Weekly Good Reads: 5-1-1

Economic Policy Uncertainty, China's NPC, Investor's Many Choices, Private Credit, US Trade Deficit, Perplexity AI

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work. I appreciate you for reading and taking the time!

Sharing the quote of the week:

Every exit is an entry somewhere else.

~ Tom Stoppard

You will find some useful sections below.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Please try our firm’s solution R4A. It’s free!

Market and Data Comments

While the year is still young, economies (globally) face peak economic policy uncertainty with trade policy at unprecedented uncertainty (see top right chart). The most immediate threats by the Trump administration are the 25% tariffs on Mexico and Canada, additional 10% tariffs on Chinese imports on March 4, and likely 25% on the EU.

Additional US tariffs could reduce global GDP by 0.7% annually if implemented, per Barclays models, with emerging markets (such as Mexico and China) most exposed. As Torsten Stok said, “an increasingly segmented global economy is putting structural upward pressure on inflation in goods markets and labor markets, which will keep interest rates structurally higher for longer [as inflation is pushed higher due to tariffs].”

Federal job cuts (300,000 initially estimated and its multiplier effect) may lead to slower US consumption.

Trump’s trade policy, uncertain Ukraine-Russian deal, limitations on immigration have likely led to individual investors’ sentiment (the spread between bullish and bearish expectations, see Econ/Invest #1) turning the lowest since 2002 and similar to the level in 2009—a key indicator for traders to watch.

Funds have increasingly flowed to fixed income (see red bars below) and diversified assets such as commodities as equity inflows retreated from the high levels in November 2024.

One good news is that the January PCE Price index (2.5% year-on-year) and core PCE Price index (2.6% year-on-year, the Fed’s preferred inflation gauge) both fell vs. December levels. Personal income also surged 0.9% in January (0.4% prior), largely because of a cost-of-living adjustment to Social Security benefits. Personal consumption expenditures, however, fell 0.2% in January (+0.8% prior). It is the second recent indicator (after January retail sales falling 0.9%) that suggested a pullback in consumer spending.

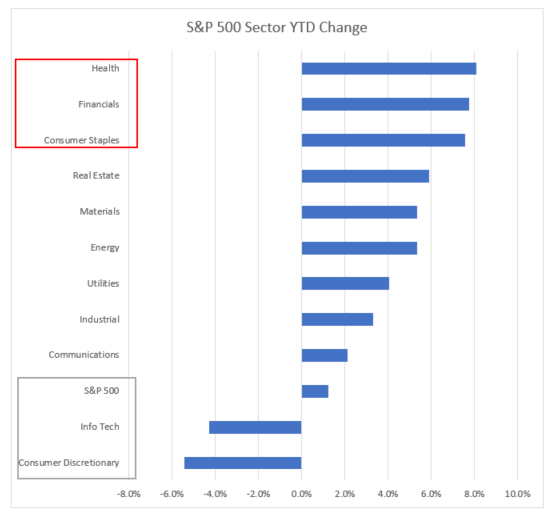

Taken together, US stocks have performed a lot worse than their overseas counterparts with S&P 500 rising 1.2% YTD versus Europe, 9.8%, and Hang Seng, 14.4%. US defensive sectors on average were up 6.6% compared to the chips sector (proxied by the ETF SMH), which has shed 17% from its all-time high in July.

Gold, defensive sectors, and China technology stocks fuelled by Deepseek AI optimism have attracted investors’ interests. For next week’s China’s National People’s Congress meetings, the market will look for fiscal deficit announcement (including special local bonds issuance), property rescue measures, consumption boosting, private sector support, and AI and data-related fiscal support to see if China can raise domestic demand and support world global growth.

This coming week, we will monitor US February ISM manufacturing PMI on Monday and ISM services PMI on Wednesday, February non-farm payrolls, average hourly earnings, and unemployment rate on Friday, the Euro Area February preliminary inflation on Monday, Euro Area February composite PMI on Wednesday, and ECB interest rate meeting and Press Conference on Thursday, and China’s NPC starting on Wednesday.

Economy and Investments (Links):

Stocks Face a ‘Fog of Uncertainty’ as Global Risks Keep Mounting (Bloomberg or via Archive)

The Election Day level is key to traders because if the S&P sinks below that [5,783 points on the S&P 500 on November 5], investors who are “currently long risk would very much expect and need some verbal support for markets from policymakers,” strategists at Bank of America led by Michael Hartnett wrote in a note to clients on Friday.

A Trader’s Guide for China’s Closely Watched Policy Meeting (Bloomberg or via Archive)

“Higher government spending driven by fiscal deficit expansion and rebounding credit impulse would help alleviate deflationary concerns and add to the ongoing China equity market re-rating,” said George Efstathopoulos, a portfolio manager at Fidelity International. China holds the keys to “rebalance its economy and create more sustainable growth domestically.”

A Modest Stagflation Shock But Not a Recession (Torsten Stok)

DOGE and tariffs combined are a mild temporary shock to the economy that will put modest upward pressure on inflation and modest downward pressure on GDP…The bottom line for markets is that this is a modest stagflation shock to the economy but not a recession.

Finance/Wealth (Link):

Investors Have More Choice — But Are The New Offers Any Good? (FT or via Archive) - a very good read!!

The industry is offering many new options to tempt investors away from the low-cost index funds that are starting to dominate the market. Some may appeal to investors looking for diversification in their portfolios. But one rule should never be far from such investors’ minds; higher returns are not certain, but higher fees are.

+ 10 of the Most Ridiculous Fees (and How to Avoid Paying Them (Lifehacker)

I particularly sympathise with the concert service, airline seat selection, and overdraft fees!

Wellness/Idea (Link):

9 Really Tired Sleep Myths (Robert Roy Britt on Medium)

One Chart You Should Not Miss: Trade Deficits in the US by Types of Goods

The US ran a record trade deficit of $1.2 trillion (in goods) in 2024, prompting the Trump administration to evaluate reciprocal tariffs on countries that have import taxes on the US. January 2025 monthly trade deficit has ballooned to an estimated $153 billion.

By types of goods, the largest items of deficits are machinery, electrical equipment, and vehicles, while the US exported more mineral fuels and oils and aircraft than it imported.

One Term to Know: What is Private Credit?

What is Private Credit?

Private credit refers to loans made directly by investment funds (not banks) to companies, typically held until maturity. They include strategies like direct lending (to financially stable companies), distressed debt (troubled borrowers), mezzanine financing (subordinated debt), and niche areas like litigation finance. From the chart above, private credit has reached $1.5 trillion in 2024 compared to less than $0.5 trillion in 2008.

In the past decade of low government bond interest rates, private credit has emerged as an alternative high-yielding asset, attracting institutional investors and now private wealth clients.

Risks Over Opportunities

While private credit commands a higher yield, as these are loans to private companies who may not receive funding from banks and can receive more flexible payment terms, there are several risks:

Loans are not traded publicly, so funds either self-report or use a third-party to value these loans, with the stability of the marks not reflecting the underlying risks.

Private credit lenders have less oversight than banks, which increasingly finance these private credit funds, causing EC and SEC to question whether these private credit assets are valued accurately.

The funds that invest in private credit tend to be issued by the same private equity firms issuing the debt, which is a potential conflict of interest.

In the event of a recession or sustained rise in interest rates, private credit, like any other high-yield debt, is likely to experience defaults.

A 2024 National Bureau of Economic Research study argued that private credit hardly offers any advantage to investors above public markets assets, once the fund’s higher fees and additional risks are considered.

[🌻] Things I Learn About AI/Productivity:

Introducing ChatGPT 4.5 (Open AI)

GPT‑4.5 is an example of scaling unsupervised learning by scaling up compute and data, along with architecture and optimization innovations. GPT‑4.5 was trained on Microsoft Azure AI supercomputers. The result is a model that has broader knowledge and a deeper understanding of the world, leading to reduced hallucinations and more reliability across a wide range of topics.

Perplexity AI and DeepSeek R1: The Ultimate Research and Reasoning Combination (Julian Goldie on LinkedIn)

The ultimate advantage lies in its flexibility for users to choose models from Claude (Anthropic), ChatGPT (OpenAI), and Deepseek (with data remaining in the US).

Perplexity Pro Models Choices

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.