Weekly Good Reads: 5-1-1

Inflation, Tariffs (and Reciprocal Tariffs), Trendless Market, Foreign Market Stock Performances, Reddit Answers, Upside of Blues

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work. I appreciate you for reading and taking the time!

Sharing the quote of the week:

Great managers are not philosophers, entertainers, doers, or artists. They are engineers. They see their organizations as machines and work assiduously to maintain and improve them. They create process- flow diagrams to show how the machine works and to evaluate its design. They build metrics to light up how well each of the individual parts of the machine (most importantly, the people) and the machine as a whole are working. And they tinker constantly with its designs and its people to make both better.

~ Ray Dalio

You will find some useful sections below.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Please try our firm’s solution R4A. It’s free!

Market and Data Comments

Taking into account the three important data releases from the US: CPI, PPI, and retail sales together and projecting onto the core PCE inflation trend,—Fed’s preferred inflation gauge—January core PCE (yoy) is expected to fall to 2.6% when the data is released on February 28.

January CPI and core CPI rose faster than expected at 0.5% and 0.4% (mom)—the fastest monthly gain since August 2023—fuelled by volatile components such as increasing food costs (eggs +15.2% mom) and price resets in January, while key PPI components such as hospital prices (+0.5% mom, 1.1% prior) and other healthcare costs are surprised to the downside, resulting in core PCE in a disinflationary trend towards the Fed’s target of 2%, estimated by Bloomberg.

Meanwhile, more tariffs were announced including a 10% additional tariff on China, a 25% tariff on all steel and aluminium imports and the prospect of reciprocal tariffs: see One Term below for more explanations), thus raising the average US tariff rate from currently 2.5% to a prospective 10%, according to Barclays. While tariffs will be higher, actual implementation dates are far from certain, and Trump’s approach remains more transactional than ideological, leaving room for the trading partners to negotiate.

Considering CPI inflation surprises, tariffs, retail sales trends, immigrant deportations, the freezing of humanitarian refugees, and the corporate spending outlook remaining strong (including AI spend by Big Tech), the US growth picture remains solid at the moment.

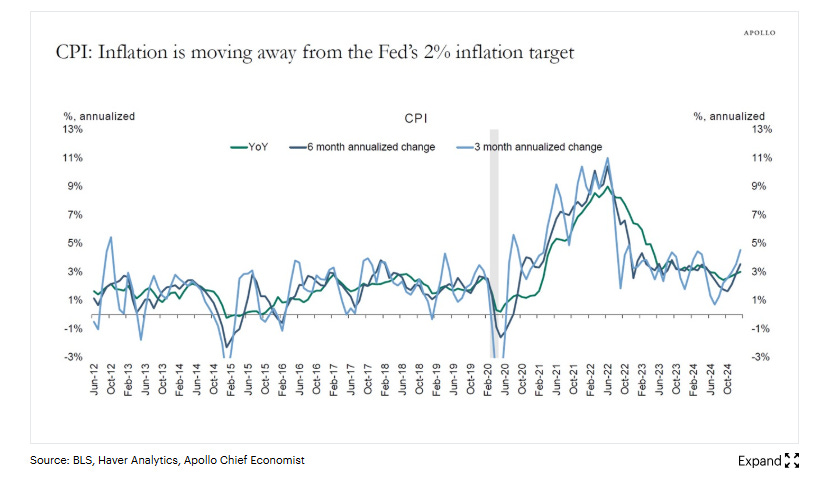

Coupled with inflation expectations and breakeven rates rising, Fed chairman Powell, when addressing the House Financial Services Committee this past Wednesday said, “Last year, inflation was 2.6%—so great progress—but we’re not quite there yet…So we want to keep policy restrictive for now,” suggesting the Fed will hold rates for longer, for fear of re-igniting inflation pressure (see Inflation: Today vs 1970s chart below).

The market now prices 40bp of interest rate cuts in 2025 compared to the 75bp cut implied from the median projections by the Fed as of December 2024.

Instead of reacting to the tariffs and inflation news, market performance has remained anchored on earnings growth (Q4 2024 so far is +16.9% yoy led by financials, communication services, and consumer discretionary), expectations of lower tax rates, higher corporate spending, more deregulations, and perhaps some removal of bloat in the government via DOGE if those pass the court.

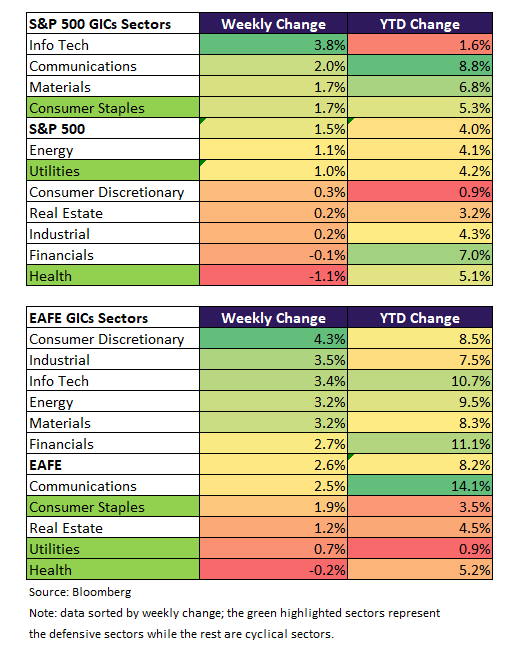

In the past week, the S&P 500 and Nasdaq rose 1.5% and 2.6% while EAFE also jumped 2.6% in USD terms as the Euro strengthened. The 10-year US Treasury yield dropped 2bp to 4.48%, the US high yield spread tightened 5bp, while the VIX declined 1.8 percentage points to 14.8% and the MOVE index fell 8.5 points to 84.7. Investors continued to move money into stocks and short-term bills/money market to enjoy relatively high interest rates.

Still, as Bloomberg charts show below, no particular market trends are sticking this year, making any macro calls confusing and difficult (see Econ/Invest #3 interview with

on his macro talks.)One trend that is not shown here, is the rally of the Hang Seng and the Hang Seng Chinese Enterprise Indices, which are up 13.2% and 15% YTD respectively, fuelled by optimism of AI company, Deepseek, which China also has a leading company in the AI ecosystem.

This coming week we will monitor US January housing starts and FOMC minutes on Wednesday, UK’s January CPI on Wednesday and the Composite PMI on Friday, Japan's January CPI on Thursday, and the Euro Area February preliminary composite PMI on Friday.

Economy and Investments (Links):

TLT: CPI Report Weighs on Bond ETFs, Tariff Impact Looms (etf.com)

The key takeaway from this data is that investors are betting more on higher-for-longer rates than they are on rate cuts, as ultra-short-term bonds pay higher yields with very little interest rate risk; whereas long-term bond ETFs like TLT are much more rate sensitive, meaning prices will fall much more when yields are rising on inflation concerns

How Torsten Slok Solved the ‘Sherlock Holmes Mystery’ of the Economy (Bloomberg)

Don’t miss his super-efficient and informative “Daily Spark” delivered to your inbox most days of the week.

There’s no internal committee to persuade and no proprietary economic model to spit out precise estimates. By Wall Street standards, his team is minuscule: just Slok and two India-based associates who build charts for him overnight. “You would be surprised at how incredibly efficient this process is,” he says. He tries to keep his notes as short as possible. “Everyone everywhere is just running out of time,” he says. “The challenge is communicating and translating [the economic situation] without using Greek letters and using fancy econometrics.” Zelter says Slok “can take a very complicated topic and boil it down to three things on a page.” For investors, that brevity is like a superpower.

Talking Trump 2.0 Uncertainties with Maggie Lake on Wealthion (

at )With Trump 2.0, that type of disruptive, high-vol strategy at a country level to break us out of that innovators’ dilemma [fiscal spending gets so bloated]…help us break out of the [existing] low-vol death spiral

I can listen to these macro talks all day, and his show notes are terrific. Michael discusses how to think about the important macro variables under Trump 2.0 right now.

Finance/Wealth (Link):

Buffett’s Way vs. Index Funds (Best Interest)

Earlier, I wrote about “poor schmucks like me and you” not having enough info to know whether the market was right or wrong. Buffett says, “I’m different than that. I do have enough info, at times, to know whether the market is right or wrong about a particular stock.”

When Buffett identifies one of those opportunities – and the opportunity has a sufficient margin of error around it (in case his math ends up being too optimistic) – he pounces. This is the method by which Buffett has built his investing legend.

Wellness/Idea (Link):

Valentine’s Day Got You Blue? There’s an Upside (Scientific American)

People want to be happy. But research is finding that a satisfying and productive life includes a mix of positive and negative emotions. Negative emotions [sadness, anxiety, boredom, anger, etc.], even though they feel bad to experience, can motivate and prepare people for failure, challenges, threats and exploration.

Pleasant or not, your emotions can help guide you toward better outcomes. Maybe understanding how they prepare you to handle various situations will help you feel better about feeling bad.

+ 33 Ways To Improve Your Life, Japanese Style (Mr. Porter)

#21 Revel in being cheap. Cheap is not a dirty word in Japan – and it’s not a byword for bad quality either. “There’s a word in Japanese called puchipura, which means cheap cosmetics that are still high quality,” Miyake says. “It’s about adjusting your lifestyle to your budget, but still enjoying luxuries when you can.”

One Chart You Should Not Miss: US is Not the Only Game in Town

European (developed and emerging) stocks have outperformed the US YTD (these are YTD performances as of 2/13/25) (credit to Bespoke).

Why? Mag 7 stocks are no longer leading the pack, underperforming the S&P 500 YTD, while Europe, Latin America, and China all rose above 10%.

One Term to Know: Reciprocal Tariffs

What are reciprocal tariffs?

Reciprocal tariffs are import taxes customized for each US trading partner, designed to match or offset the tariffs and other trade barriers imposed on US goods by other countries, e.g., if the UK imposes a 5% tax on U.S. cars, the US would impose a 5% tax on UK cars. Historically, reciprocal tariffs have meant lowering trade barriers.

Trump signed executive orders on February 13, 2025, directing the Office of the US Trade Representative to propose reciprocal tariffs by April 1, recommending new levies on a country-by-country basis. Trump wants to raise revenue for the Federal budget and reduce the US. trade deficit, ultimately promoting more US business activities and growth domestically.

Pros and Cons?

Proponents argue that reciprocal tariffs could level the playing field for US manufacturers, potentially reducing trade deficits, generating more income for the Federal Budget, and adding some certainty to the trade landscape by creating a more standardized approach to tariffs.

Critics, however, warn that reciprocal tariffs could lead to higher prices for American consumers, erode household spending power, and potentially disrupt global supply chains. Economists all seem to agree broad tariffs will cost average Americans money and could endanger certain jobs although market participants may differ (see Econ/Invest #3 above).

On the broader economic impact: reciprocal tariffs implementation not only can lead to higher inflation in the US and slower economic activity globally but also cause the Fed to maintain higher interest rates for a longer period. Emerging market nations with higher tariffs on US goods, such as India, Argentina, and parts of Africa and Southeast Asia, could be most impacted.

[🌻] Things I Learn About AI/Productivity:

Reddit Answers (Reddit)

These days when we use Google search, we can see a list of Reddit answers pop up. So it is better to ask Reddit directly — here come Reddit Answers, which uses a new, AI-powered conversational interface. “Once a question is asked, curated summaries of relevant conversations and details across Reddit will appear, including links to related communities and posts. Redditors can easily read relevant snippets and answers inline from real Redditors, jump into the full conversations, and go deeper in their search with their own or suggested follow-up questions.”

For example: I asked: “Which one is better - Deepseek or ChatGPT?” The answer is well-rounded and based on real conversations.

The Artificial Intelligence Driven Future: Who Wins and Who Loses? (Elizabeth Yin, Hustle Fund (a micro VC)

According to her co-founders, when Elizabeth writes, you drop everything to read it!

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.