Weekly Good Reads: 5-1-1

Strong Dollar, China and Apple, Commodities vs. equity valuation, Decision intelligence, Bond Risk Premium

Welcome to Weekly Good Reads 5-1-1, and a warm welcome to my new subscribers! Thank you so much for supporting my work 🙏.

I am Marianne O, an investment professional and author of The Learner’s Mind about investing, economy, and wellness ideas. For this Weekly, I include 5 links to relevant economic and investment news, finance, and wellness/idea pursuit based on what I read. I also include 1 important chart and 1 investment term to know. All the Weeklies are here. You can also find the index of charts and terms. You can easily subscribe to my newsletter by clicking below.

Market and Data Comments

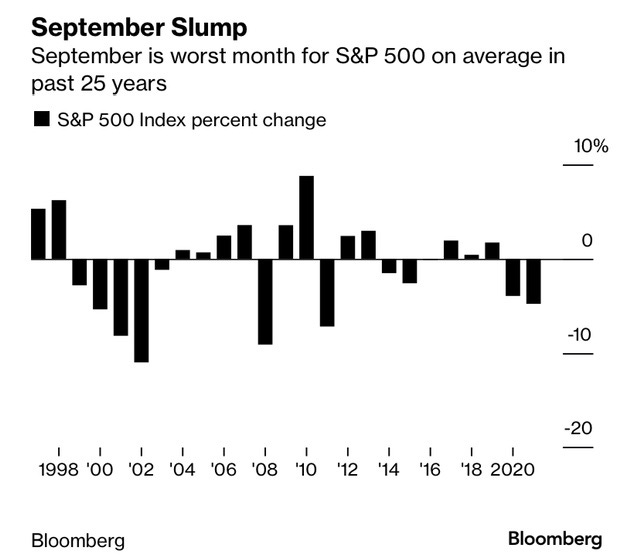

September on average has the worst monthly return using the last 25 years’ data of the S&P 500 (-0.7%, see above chart, Bloomberg). The best month is December at +1.64% (CFRA, since 1944).

Global stocks declined 1.2% in September. It is the month corporates and investors reevaluate their budgets or positioning. Further interest rate hikes, Russia, and the US midterm elections can all add to volatility.

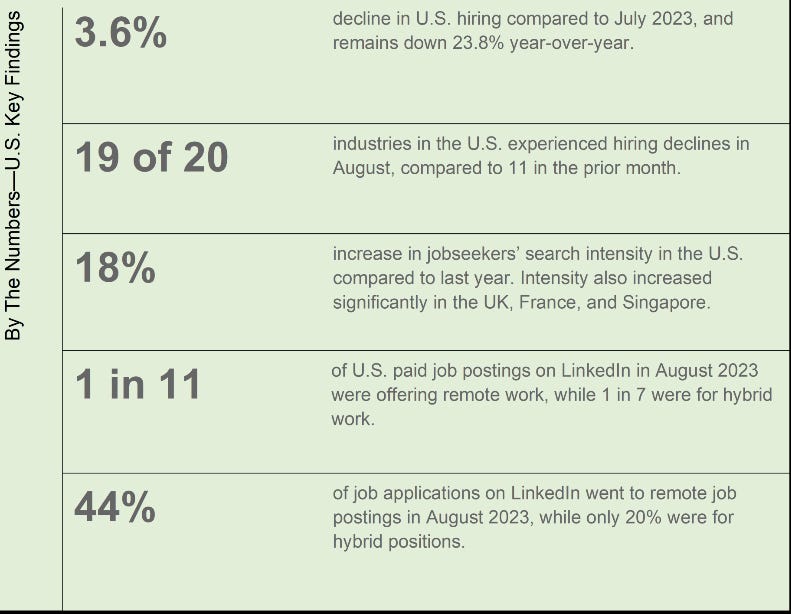

This week, many Fed governors sounded more cautious about NOT over-hiking rates and squashing the economy (see article #1) as data for core inflation and the labour market (see LinkedIn table below) have eased.

Yet wobbles came from Apple - the stock dropped 6% this week upon the news China has widened ban on state employees from using iPhones at work for fear of security leaks. Apple’s woes spread to Nasdaq, which dropped 1.9% this week. This may cheer the investors who already sounded cautious about tech valuation and the narrow breadth of the stock rally this year (84% of S&P 500 gain this year came from 7 big-cap stocks (out of 500) as of June 7).

Yet, the bond yield has not stopped climbing, and we may see a long-bond yield of over 5% as domestic private investment is growing strong while personal consumption remains robust despite the rate hikes. Stocks now are more “fearful” of good economic data for the Fed will have to keep hiking rates.

The rising long-bond yield has also helped strengthen the US Dollar by 12.9% and 6.5% against the Yen and the Chinese Yuan YTD. A strong dollar hurts S&P 500 companies’ foreign earnings (about 30% of earnings are derived internationally), which means lower stock prices.

Next week, we will monitor the August CPI and PPI in China this Saturday, the US August CPI next Wednesday, and the ECB rate policy next Thursday.

The Group of 20 top world economies welcomed the African Union as a member at their annual summit Saturday, but their wording on the contentious issue of Russia’s war in Ukraine was limited to a call to avoid forcefully seizing territory or using nuclear weapons.~AP News on the G20 Summit (September 9, 2023)

Economy and Investments (Links):

The Fed Is Getting More Hopeful It Can Avoid a US Recession (Bloomberg)

China is no longer sure to become the largest economy (Financial Times by Mohamed El-Erian)

Apple Becomes the Biggest U.S.-China Pawn Yet (Wall Street Journal) and more extent of the ban from FT here.

+ The Great Gloom? U.S. Worker Happiness is Eroding at a Record Pace. And Health Care Pros Most Dire of All (Deseret News)

Finance/Wealth (Link):

The $100trn Battle for the World’s Wealthiest People (The Economist)

This is the most coveted part of finance right now - the wealth management industry. The industry is expected to grow from $130 trillion of assets under management to $230 trillion by 2030 with revenue almost doubling. Global wealth is equivalent to 6 times the global economic output currently.

Wellness/Idea (Link):

Decision Intelligence (LinkedIn course by Google ex-Chief Decision Scientist Cassie Kozyrkov)

It is a worthwhile 90-minute learning on decision-making.

We are going to cover the most important concept in decision analysis —the difference between a decision and an outcome and why outcome bias is such an important thing to watch over, and why a decision maker needs to avoid outcome bias, and why outcome bias, unfortunately, is one of society’s favourite form of mass irrationality. ~ Module 1, course 1.

One Chart You Should Not Miss: Commodities vs Equity Valuations (1970-2023)

The graph below plots the commodities index (proxied by the Goldman Sachs Commodity Index) vs. the S&P 500 index. When that ratio rises, commodities do better than stocks.

When commodities do well, stocks usually do worse, and vice versa. The ratio goes through huge cycles. Commodities prices have reached a 50-year low vs. equity prices currently. The last time the ratio troughed (the 2000 tech bubble), commodities began a supercycle, which means commodities perform much better than their long-term historical average. This was the result of industrialization and demand for raw materials in the BRIC nations.

Commodities staged a comeback in 2022 while global stocks tanked, but this year, the S&P 500 outperformed by about 18% YTD.

This ratio can tell you a bit about the macroeconomy. During a period of uncertainty with inflation rising, commodities can act as a good hedge vs. the stock markets as they act more like a safe haven. Commodity sectors such as energy and gold mining can perform better than stocks.

In a period of strong economic growth, commodities can lead the stock performances and do well due to rising demand for commodities.

Commodities can be a diversifier in a portfolio though commodities are more volatile than stocks historically, so investors need to be careful with the allocation between commodities and stocks to suit their risks and goals.

One Term To Know: Bond Risk Premium (Term-Premium)

According to the New York Fed, “yields on Treasury securities are composed of two components: expectations of the future path of short-term Treasury yields and the Treasury term premium. The term premium is defined as the compensation that investors require for bearing the risk that interest rates may change over the life of the bond.”

Put simply, the term premium reflects the higher compensation required for long-term borrowers. The longer you lend money, the more chance things will go wrong. As Ben Bernanke found, the term premium reflects two key risks.

One is the changes in demand/supply of bonds, which can affect bond prices. The other is future inflation, which would reduce the real value of future bond payments. If the risk is higher in either of these cases, then investors will need higher interest rates to compensate for the risks.

The New York Fed model (below) estimates the term premium as follows (red line). It has dipped below 0 since 2017 (now at -52bp).

The term premium, albeit negative, has stopped falling, likely due to stronger inflationary pressure and the Fed shrinking the size of its Treasury bond portfolios (both will push up longer-term yields).

Please do not hesitate to get in touch if you have any questions! If you like this weekly, please share or subscribe to my newsletter.