Weekly Good Reads: 5-1-1

Jackson Hole, US Fiscal, China Analysis, BRICS+6, LinkedIn is Cool, R-Star

Welcome to a new issue of Weekly Good Reads 5-1-1, and a warm welcome to my new subscribers! Thank you so much for supporting my work 🙏. Please let me know any feedback or questions by commenting below.

I am Marianne O, an investment professional and author of The Learner’s Mind about investing, economy, and wellness ideas. For this Weekly, I include 5 links to relevant economic and investment news, finance, and wellness/idea pursuit based on what I read. I also include 1 important chart and 1 investment term to know. All the Weeklies are here. You can easily subscribe to my newsletter by clicking below.

Market and Data Comments

In Jackson Hole this week, Fed Powell said inflation remains too high, signalling the Fed will maintain a “restrictive” monetary policy until the 2% inflation target is hit. European Central Bank (ECB) President Christine Lagarde will set borrowing costs as high as needed to tame inflation and leave them there for as long as it takes. At this stage of the monetary cycle, risk management is “critical” as Powell mentioned in his speech, indicating a cautious stance going forward.

Meanwhile, in the US, there is an ongoing debate on the level of the “neutral” real interest rate (R-star) where monetary policy is neither too tight nor too loose (see One Term to Know below for more about R-star). Some say structural issues (deglobalization, supply-side constraints, US fiscal spending) will make long-term inflation higher and the neutral rate higher than the historical 0.5% pre-pandemic.

Market participants are split on whether long-term bond yields will rise or fall. This gives Fed Powell maximum flexibility (i.e. data-dependent) to decide on his next move without upsetting the bond market. Currently, the swap traders are pricing in a two-third chance the Fed will raise 25bp in November after a likely pause in September.

Another notable news is the massive beat by Nvidia (pronounced as “N-vidia”) in its latest quarterly results - revenue of $13.5bn (up 88% q/q and 101.5% y/y) beat Wall Street expectations of $11.2bn driven by Data Center with revenue of $10.3bn, up 141.0% q/q and 171.2% y/y. EPS (non-GAAP) of $2.70 beat the Street estimate of $2.09. Its strong outlook through 2024 suggests that Nvidia does not have serious competition for the high-powered chips needed to build and run large AI models.

A much bigger economic issue in the US is the crisis-size budget deficit (see the chart above and article #1 under Economy and Investments). US fiscal spending since the Pandemic is unprecedented, with the Budget Office projecting an average 6.1% fiscal deficit for 2023-2033. As the interest rate has risen, the net interest payment on US government debt is now 14% of the tax revenue (up from a low of 6.9% in 2015) and is estimated at close to 20% by 2032.

Next week, we will monitor Europe’s August inflation and unemployment rates on Thursday and China’s August Caixin PMI and the US August jobs report and unemployment rate on Friday.

As is often the case, we are navigating by the stars under cloudy skies. In such circumstances, risk-management considerations are critical. At upcoming meetings, we will assess our progress based on the totality of the data and the evolving outlook and risks. Based on this assessment, we will proceed carefully as we decide whether to tighten further or, instead, to hold the policy rate constant and await further data. Restoring price stability is essential to achieving both sides of our dual mandate. We will need price stability to achieve a sustained period of strong labor market conditions that benefit all.

We will keep at it until the job is done.

~ Fed Chairman Jerome Powell at Jackson Hole, 2023

Market Changes for the Week:

Economy and Investments (Links):

US Budget Deficits Are Exploding Like Never Before (Bloomberg or click here)

The Staggering Economic Impact of Taylor Swift’s Eras Tour (Time)

Wither China? Part I, Part II, and Part III (AT Chartbook by

).Read Adam Tooze's excellent analyses in a 6-part mini-series on what is ailing China’s economic outlook, be it authoritarianism, fixation on growth, or overconfidence and hubris.

Finance/Wealth (Link):

Why Investors Fire Their Advisors, According To Morningstar (FA Magazine)

+ Stock Pickers Never Had a Chance Against Hard Math of the Market (Bloomberg or click here)

Wellness/Idea (Link):

Why Blue Space is Better Than Green Space (Catherine Sanderson on Medium)

+ Sorry, But LinkedIn is Cool Now (Bloomberg)

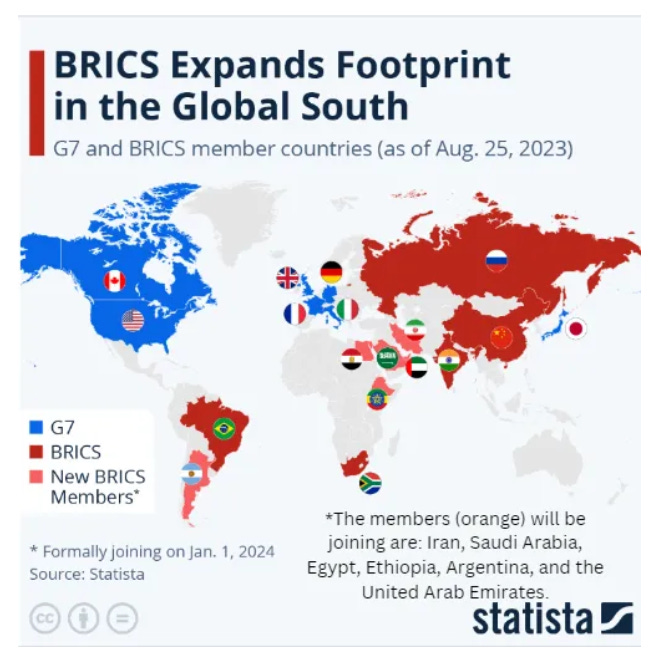

One Chart You Should Not Miss: The New BRICS - Expands in Global South

After the 15th BRICS summit in South Africa this week, 6 new members were invited to join the original BRICS (Brazil, Russia, India, China, and South Africa) on January 1, 2024, to expand the bloc’s footprint in the Global South.

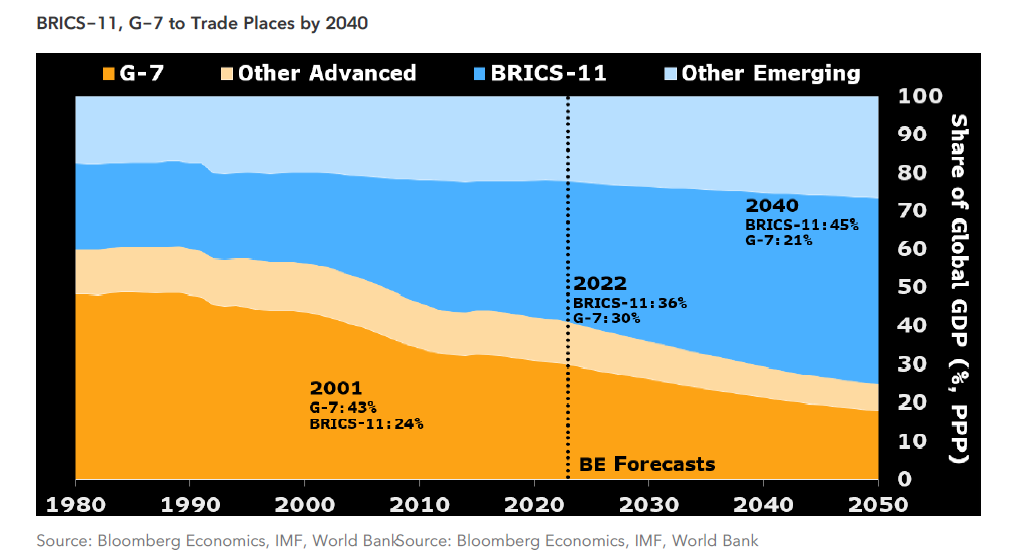

The 6 countries are Argentina, Egypt, Ethiopia, Iran, Saudi Arabia, and the U.A.E. Bloomberg Economics’ forecasts show as India takes off (while China’s growth is slower than in early decades), the BRICS-11 share of world GDP (in purchasing power terms) will be more than 45% by 2040, compared with 36% in 2022. The original BRICS accounted for about 32% of the world’s GDP in 2022 with China alone accounting for 18% of GDP.

In comparison, G7's global GDP was 30% in 2022 and will be about 21% in 2040 (a decline of 9%) (second chart).

BRICS not only expands in size, but the world’s economic force is shifting towards countries that are “partly free” or “not free”. Amongst BRICS-11, only Argentina, Brazil, and South Africa were rated “free”, while India was rated “partly free” by Freedom House last year.

One Term To Know: R-Star

The economic buzzword these days is R-Star.

R-Star, often stylized as R*, is the real interest rate where demand for savings and investment in the economy is at an equilibrium. A benchmark interest rate at neutral neither fuels nor restricts growth and inflation. Put another way, monetary policy is neither tight or loose.

~ Barron’s

If one assumes the long-run federal funds rate is 2.5%, and the Fed’s inflation target is 2%, then the estimated real neutral rate is 0.5%, which is the Fed’s median estimate since 2019.

The Fed has raised interest rates to 5.25%-5.5% but has not meaningfully slowed the economy. This implies the neutral rate could be higher than 0.5%, maybe 1.5 to 2% as research said.

While the Fed may not have to raise rates higher, it needs to keep rates higher for longer because hiking rates no longer slows the economy as much as expected.

The higher interest rates have to rise, the higher the bond yield, which will dampen the equity market.

How do we derive an estimate of the long-term government bond yield based on the neutral rate? Consider this: if say the neutral rate is 1% (higher than 0.5%), the long-term inflation rate is 2.5%, and the term premium (compensation to move from a short-dated government bond and hold a say 10-year bond) is 1%, then you get a US 10-year government bond yield of 4.5%, which is 25bp higher than the current level of 4.24%.

Please do not hesitate to get in touch if you have any questions! If you like this weekly, please share or subscribe to my newsletter.