Weekly Good Reads: The Big Wait—Fed and the Market

FOMC, Net Portfolio Outflows, Bond ETF, Best Investors, Prediction Market, Future of Work

Welcome to a new Weekly Good Reads by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work! Please hit the 💛 button or share with others if you like it.

Sharing the quote of the week:

There are some things you learn best in calm, and some in storm.

Willa Sibert Cather

Weekly archives | Investing | Ideas | Index of charts and terms | Conversations with Investment Managers

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Try R4A for free!

Market and Data Comment

As the market expected, the Fed held interest rates steady at the 4.25% to 4.5% range in the latest FOMC meeting.

The June Dot Plot (chart above) reflects two rate cuts (median) by the end of 2025 but shows a great divergence of views between those officials who fear economic slowdown (favouring a cut) versus those who worry about inflation risks rising when the economy is holding up (favouring no rate cuts)—eight members voted for two rate cuts by the end of 2025, seven voted for no rate cut, two voted for one rate cut, and two voted for 3 rate cuts.

The Fed Chair added, “No one holds these rate paths with a lot of conviction,” and later said the FOMC is “well positioned to wait to learn more about the likely course of the economy before considering any adjustments to our policy stance.” (See Econ/Invest #1)

In their latest Summary of Economic Projections, Fed officials raised their median estimate for inflation for end-2025 to 3% from 2.7% in the March projection, and reduced their forecast for real GDP growth to 1.4% from 1.7% and the unemployment rate to 4.5% from 4.4%.

The FOMC, like a majority of economic forecasters, expects a meaningful increase in inflation from the tariff increase because “someone has to pay for the tariffs”, said Powell, but the inflation can take time to show up. Powell sees that the softer labour demand is occurring at the same rate as the reduction in labour supply.

The labour market is still in equilibrium, and the economy remains solid (defying all forecasts so far, as Powell remarked), but the Fed is watching the labour market (especially the falling job finding rate) and the effective tariff rate carefully. (See Econ/Invest #3 why the Fed is cautious and not stupid to hold rates.)

Another interesting piece of data is the April United States Net Treasury International Capital Flows, which shows a small net foreign sales of long-term securities of $7.8 billion (vs. a monthly average net foreign inflow of $64 billion in 2024). Banks’ net dollar-denominated liabilities to foreign residents decreased by $14.1 billion (see the chart below, and the breakdown of foreigners’ net transactions by asset classes).

The TIC data shows foreigners sold $32 bn of fixed income (excluding short-term debt) of about Treasuries in April, but the fear of massive capital flight out of the US was not supported.

With uncertainty regarding the economic outlook, interest rate policy, and trade tensions, investors remain cautious and lack conviction. Despite being 3% away from the recent peak, the S&P 500 has been stuck in a narrow range, often due to the many crosswinds.

In the past week, the Fed, Bank of Japan, and the Bank of England all held rates, while the central banks of Switzerland, Sweden, and Norway all cut rates, with Switzerland cutting its interest rate to zero, as the trade outlook from Trump’s tariff policy has depressed economic activities in Europe.

At the time of writing, the US has struck three nuclear sites in Iran, with Trump saying that Iran’s nuclear enrichment facilities had been “completely and totally obliterated.” Trump warned Iran of further attacks if Tehran refused to “make peace”.

The widening conflict involving the US will keep oil prices up. FT mentioned Iran can retaliate by “direct attacks on US forces or diplomatic missions in the region, cyber attacks, terrorism, or new strikes by Iranian proxies. Tehran could also disrupt energy shipments out of the Gulf.”

At the same time, the US dollar may strengthen in the short term due to the safe-haven bid. From history, the initial negative US stock markets’ reaction to war has not been long-lasting, though investors have to brace for more oil price increases and volatility.

This coming week, we will also monitor Fed Chairman Powell testimony to the Senate Banking Committee on Tuesday and the House Financial Services Committee on Wednesday on the state of the US economy, June S&P Global Composite PMI and US May new home sales on Monday, May personal spending and core PCE Price Index on Friday, Euro Area June Composite PMI on Monday, and Japan’s June Tokyo CPI on Friday.

Economy and Investments (Links)

Fed’s Powell Says Rate Path Unclear But Tariff Impact Is Coming (Bloomberg)

The Fed chief emphasized policy should be forward looking, adding that officials are beginning to see some effects from tariffs but expect more over the coming months.

While forecasters expect a “meaningful” rise in inflation, Powell said the jobs market isn’t “crying out for a rate cut.”

US Enjoys a Rare Moment of Oil Supremacy in Iran (Bloomberg)

The White House must also be careful about expecting the US oil bonanza to last forever. The country’s geological endowment is marvelous, but it’s finite. Every anecdotal sign suggests that the shale boom is largely in the rearview mirror, with further production gains limited.

- )

But the reason Powell isn’t cutting rates now is that the Fed is in a difficult position, largely thanks to, you guessed it, Trump himself, with an assist from the ghost of Arthur Burns.

+ Who Are The World’s Best Investors (The Economist or Archive)

In 2022 David McLean of Georgetown University and co-authors showed that corporate-share sales and buy-backs forecast future returns more accurately than the trades of banks, hedge funds, mutual funds and wealth managers.

Finance/Wealth (Link):

Millennial Women are Investing Earlier, and With Greater Confidence, Than Their Elders (Equities.com)

The survey finds that Millennial women are more likely to embrace a broader and more complex range of investments beyond more traditional stocks and bonds, including cryptocurrencies, options or futures, and alternative investments.

While knowledge sharing and tapping their communities to discuss finances is important to women investors across generations, it stands out as a core part of the investing experience for Millennial women, the survey finds. In fact, nearly twice as many Millennial women investors say they participated in an investment club or community when they first started investing than prior generations.

+ 5 Themes Defining Bond ETF Investing Today (PIMCO)

Multisector ETFs – which barely registered two years ago – have ballooned recently, with over $20 billion in net inflows since mid-2023. Active core and core-plus ETF strategies now have more than $88 billion in assets, according to Morningstar. This rapid growth is not merely a function of product innovation, but a response to the demands of an uncertain market.

Elevated starting yields make fixed income attractive. Plus the negative correlation of fixed income – particularly short- to intermediate-maturity bonds – versus equity returns has reasserted itself, providing an important buffer against equity market drawdowns. As a result, active fixed income ETFs now account for nearly 40% of overall fixed income ETF flows, despite representing just 17% of total fixed income ETF assets, according to Bloomberg.

Wellness and Idea (Link):

10 Tiny Habits That Make You Healthier, Calmer, and Harder to Kill (Medium)

I will practice #5 - say no to one thing per week 🚫 - and #10 - sit in silence for 60 seconds 🔕.

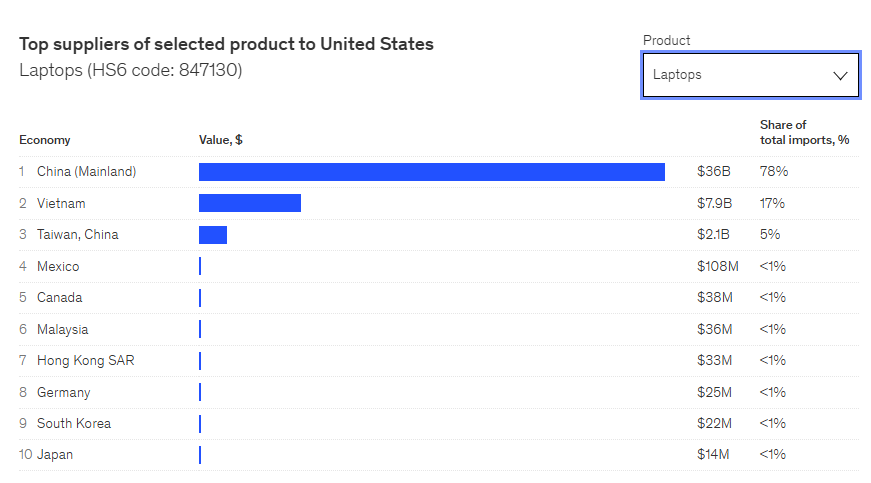

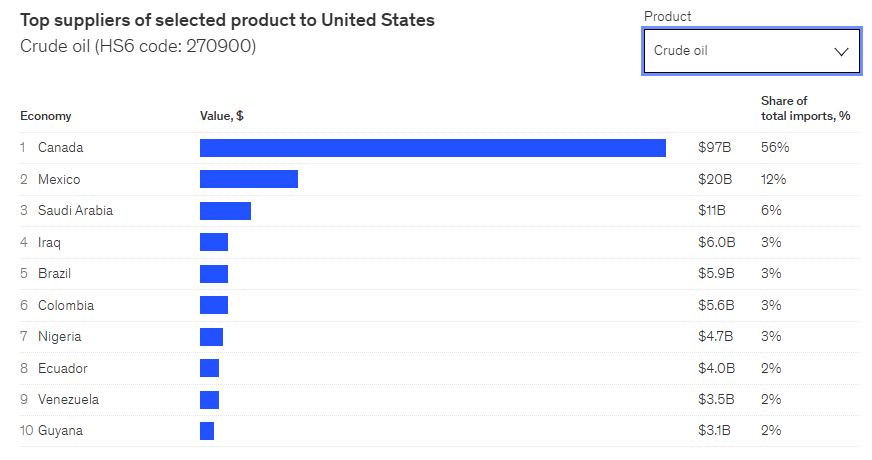

One Chart You Should Not Miss: Which Products are Supplied by a Small Number of Economies? (McKinsey)

Amongst the US imports, there are a few products that are heavily concentrated in one country e.g. 84% of spark ignition trucks come from Mexico, 78% of laptops and 70% of li-ion batteries come from China, 67% of computer units; storage, input and output come from Mexico, and 56% of crude oil comes from Canada.

One Term to Know: Prediction Market in Finance

Prediction markets, also known as information markets or event futures, leverage financial incentives to forecast future events, allowing participants to trade contracts tied to specific economic outcomes, such as future inflation rates or interest rates and commodity price movements.

Prediction markets can provide useful signals to investors as their dynamic pricing reflects the collective, real-time probability for an event by market participants based on “efficient market hypothesis” and the wisdom of the crowds, and effectively aggregates real-time dispersed information, often outperforming traditional forecasting methods because the participants have “skin in the game”.

By election day, the markets [the Iowa Electronic Market trading on presidential election contracts] with an average absolute error of around 1.5 percentage points, were considerably more accurate than the Gallup poll projections, which erred by 2.1 percent. ~ NBER Working Paper, Can Markets Predict the Future?

Internal corporate prediction markets have also been successfully deployed by firms like HP, Ford, and Intel to forecast printer and car sales and product demand (better than their internal processes would predict), leading to more responsive production planning and optimized inventory management.

The downside of using prediction markets includes the potential for "perverse incentives", where participants might be motivated to manipulate or cause the predicted outcome, eroding trust in market integrity, or the deliberate spread of misinformation to influence prices for profit, which can distort market signals. When integrity and public trust in the outcome are compromised and misinformation abounds, prediction markets are not as telling.

Furthermore, market-specific challenges like liquidity constraints and susceptibility to behavioural biases can reduce their reliability and accuracy.

🌻Things I learned About AI/Productivity

The Future of Work is Agentic (McKinsey)

Your AI agents could now be the evolution and the creation of a digital replica of the entire workforce of an organization. ~ McKinsey Senior Partner, Jorge Amar

Study: ChatGPT's Creativity Gap (Axios)

AI makers say their tools are "great for brainstorming," but experts find that chatbots produce a more limited range of ideas than a group of humans.

Thanks for reading!

Please do not hesitate to contact me if you have any questions, and check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please 👍and share it with your friends, or subscribe to my newsletter🤝.