Weekly Good Reads: Now is Time to Focus on the Macro

Stagflation Risks, Stocks Rally, How Not to Invest, International Dollars, AI Misbehaving, and in Romance, Ikigai

Welcome to a new Weekly Good Reads by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work! Please hit the 💛 button or share with others if you like it.

Sharing the quote of the week:

The person who learns the most in any classroom is the teacher.

If you really want to learn a topic, then “teach” it. Write a book. Teach a class. Build a product. Start a company.

The act of making something will force you to learn more deeply than reading ever will. ~ James Clear

Weekly archives | Investing | Ideas | Index of charts and terms | Conversations with Investment Managers

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Try R4A for free!

Market and Data Comment

In a sea of market noises and signals, there is a clear voice I listen to often, and that is Torsten Slok, Apollo’s Chief Economist.

He laid out his mid-year economic and market outlook here, saying the higher oil prices, higher tariffs, and immigration restrictions are putting downward pressure on GDP growth and upward inflation pressure; a lower GDP growth and higher inflation equate to stagflation.

The upward inflation pressure is limiting how much the Fed can cut interest rates later this year. The investment implication is that “all-in yields will stay higher for longer, which will continue to support fixed income assets, including private credit,” said Torsten.

He followed up on Friday with a piece on the growing issuance of Treasuries and the ever-growing interest payments for the US government—not only the government has to refinance $9 trillion of its debt in the next 12 months, but every one dollar the US government collects in revenue, 20 cents goes to pay down interests (see Econ/Invest #1). With government debt and, therefore, Treasury issuance growing faster than the economy, US long-term interest rates will likely rise.

This past week’s data showed the US economy less willing to spend and hints at stagflation — May core PCE deflator (price inflation) rose 0.18% m/m and 2.7% y/y, higher than expected. Real personal spending declined 0.3% (+0.1% prior) while personal income dropped 0.4% (+0.7% prior) as consumers pulled back from cars and parts spending.

This is on the heels of the revised lower real GDP in Q1, where overall spending rose at 0.5% (instead of previously reported 1.2%), with GDP declining at a 0.5% annualized rate in Q1. Continuing claims rose 37K to 1.97 million for the week of June 14, also pointing to ongoing labour market cooling.

Fed Chairman Powell maintained a cautious tone at the semiannual testimony to Congress, citing uncertainty and inflation risk from tariffs even though two Fed officials recently signalled their openness to a cut in the July 29-30 meeting.

From the chart above, the market is pricing in two 25bp rate cuts in the US by the end of 2025, with the path of interest rate in the US and the UK in lock step until the middle of 2026, when the Fed is seen to reduce rates at a faster pace. ECB is largely done in rate cuts, while the Bank of Japan is expected to raise interest rates at the end of 2025, with the rate path continuing to march upwards.

The US-China trade framework was reported “done” on Friday, with China allowing exports of rare earth minerals and magnets (important ingredients for manufacturers in auto, aerospace, semiconductors, and military), while the US will allow Chinese students to be in US universities.

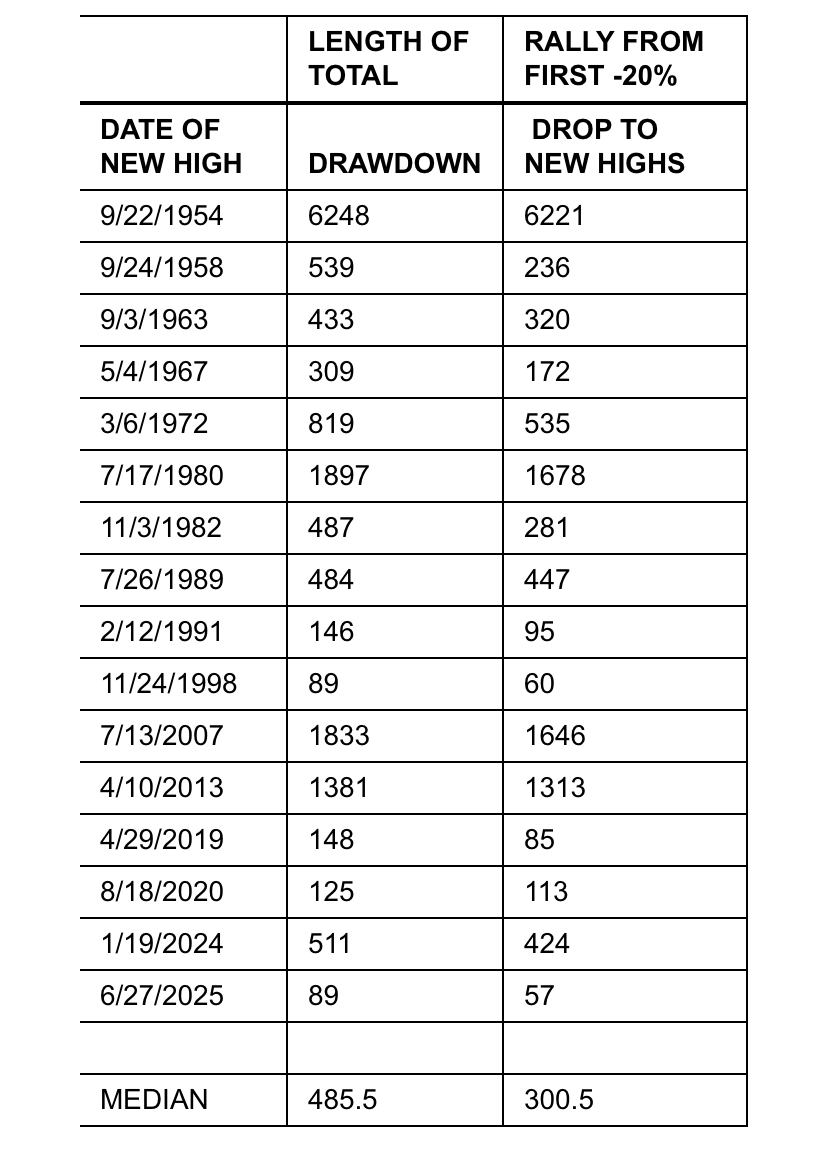

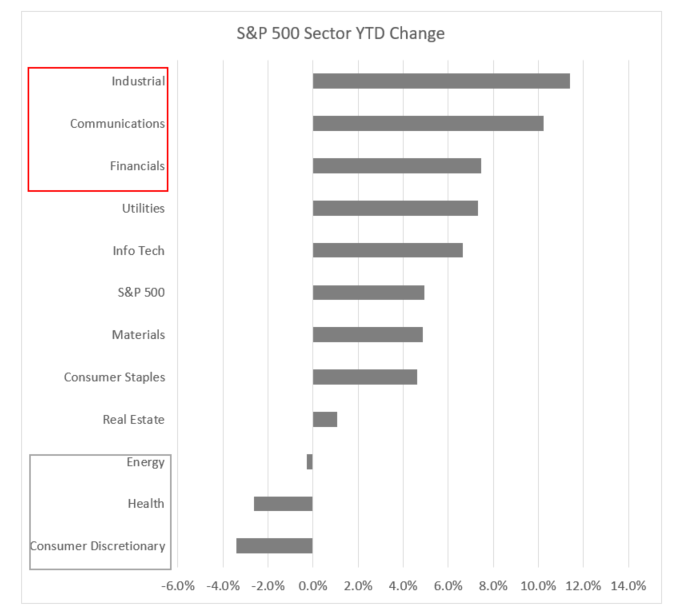

Both the S&P 500 and Nasdaq exceeded their previous highs this year as trade and geopolitical uncertainty have somewhat retreated, AI optimism and spending has continued, and US earnings estimates has slightly risen for Q2, with a full year expectation of 9.1% for 2025 (the highest EPS growth being in info tech, communication services, and healthcare).

As seen below, the latest S&P trough to peak has been the shortest in history, very similar to that in November 1998, which you might recall was the depth of the Asian debt crisis, Russian debt default and the LTCM crisis, which prompted the Fed to lower interest rates three times to buffer the still-strong US economy. Will the Fed change its tune soon? It all depends on the path of inflation and the labour market!

However, institutional investors are citing a litany of concerns about the US stock markets, including five key risks: the July 9 tariff deadline, uncertain earnings growth, geopolitical risks, US debt and Federal Reserve leadership, and high valuations (see Econ/Invest #2).

This coming week, we will monitor the US June ISM manufacturing PMI on Tuesday, the June nonfarm payrolls, unemployment rate, average hourly earnings, and S&P Global PMI on Thursday (July 4, Friday, is the US Independence Day), June Euro Area inflation and manufacturing PMI on Tuesday, May unemployment rate on Wednesday, June Composite PMI on Thursday, and China’s June NBS manufacutring PMI and Caixin manufacturing PMI on Monday.

Economy and Investments (Links)

Treasury Issuance Growing (Torsten Slok, The Daily Spark)

…debt-servicing costs are rising rapidly, and the US government currently pays a record-high $3.3 billion in interest payments every day, and for every dollar the US government collects in tax revenue, about 20 cents go to paying interest on debt.

With debt levels growing much faster than GDP, the bottom line is that Treasury issuance will continue to grow faster than the economy, and the most likely outcome is that investors will demand compensation in the form of higher long-term interest rates.

Five Risks for Stocks That Cloud the Outlook for the Second Half (Bloomberg)

US equity valuations, particularly in market-capitalization-weighted strategies such as the S&P 500 Index, may have further to adjust if US economic conditions deteriorate,” said David Chao, a global market strategist at Invesco Asset Management. “Markets outside of the US mostly trade at lower multiples, and we think the gap with the US will continue to narrow.

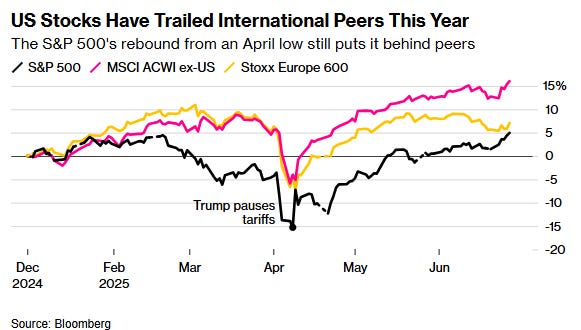

The Unlikely Stocks That Drove the Market to a Record High (WSJ or Archive)

To start with, the best-performing stock since the February high is the discount store Dollar General DG increase; green up pointing triangle, up around 50%. It isn’t an outlier. Its rival Dollar Tree is the 13th-best performer in the S&P 500, up around 30%. They aren’t quite the opposite of AI, but they are the opposite of the growth story that investors are warming up to once again.

Finance/Wealth (Link):

How Not to Invest: Avoiding Common Mistakes and Dangerous Financial Advice with Barry Ritholtz (Peter Lazaroff)

Barry emphasizes that focusing on avoiding mistakes rather than trying to identify the next big winner is a far more practical and effective investment strategy. His straightforward advice encapsulates the essence of inversion: “Forget trying to pick the next Nvidia, just make less mistakes. You’re way ahead of 90% of your peers.”

Wellness and Idea (Link):

Reasons for Being (Information is Beautiful)

I love to stare at beautiful visuals, and I am in love with this one. The Japanese word “ikigai” combines “iki” (life) and “gai” (worth or value) and encourages individuals to identify what truly matters to them and to live a life filled with meaning and joy.

The author revised a previously drawn Venn diagram and came up with a new one with a complete set of unique intersections.

Ikigai = what you are good at + what you love + what the world needs + what earns you money.

Struggling = the above first three without “what earns you money” 🌀!

One Chart You Should Not Miss: World Defense Spending as % of Real GDP

In the recent NATO summit, 32 North American and European countries agreed to a defense budget of 5% of real GDP by 2035, compared to 2% currently.

Spending diverged across countries, with the US being the only country that reduced the spending as a % of GDP over the past decade; still, the US represented 66% of the total defense spending in 2024!

From the chart below, countries like Italy, Belgium, Canada, and Spain have not met the 2% spending commitment. Bringing up the European defense budget to 5% of GDP would add $1.9 trillion of defense expenditure, which means the Europeans will need to have to shift their priorities in their national budgets.

They can reallocate existing national budgets, utilize the EU mechanisms for joint defense projects, and potentially take on more debt. Also, the EU is providing flexibility within its budget rules, allowing countries to temporarily exceed deficit limits to fund the increased defense investments.

One Term to Know: International Dollar

Many have heard of GDP per capita, which divides the nominal GDP by the population of a country. It is a common way to compare the standard of living or average income among countries.

But incomes, measured in local currency, may be meaningful to the local people, but GDP per capita itself does not tell us anything about the relative standard of living. If you convert the local GDP into GDP in US dollars using the market exchange rate, GDP per capita will be a lot smaller for the poorer countries because the prices in these countries can be a lot lower than in richer countries, making them look poorer than they actually are.

What we want is a measure that tells us what money can truly buy in different countries.

International dollars are a hypothetical currency that helps us answer such questions by equating different currencies with what they can buy. They adjust for the fact that the cost of living is much higher in some countries than in others, allowing us to compare data denominated in different currencies in terms of their local “purchasing power”.

International dollars adjust for differences in prices across countries and inflation over time. One international dollar is intended to buy the same quantity and quality of goods and services, no matter where or when it is “spent.” ~ Our World in Data

The chart below compares GDP per capita for the United States and four selected countries in 2023 using (1) international dollars (adjusted for differences in local prices using PPP rates) and (2) market dollars (local currencies converted to US dollars using market exchange rates). Both series are adjusted for inflation, with 2021 as the base year.

Since the US is the benchmark country for calculating PPP rates, its GDP per capita is the same in both measures. Using India as an example, GDP per capita as measured in market dollars shows India is 29 times poorer than the US but only 8 times poorer in int-$, demonstrating the power of using international dollars to compare countries’ living standards.

🌻Things I learned About AI/Productivity

The Struggle to Get Inside How AI Models Really Work (FT or Archive)

While company researchers said this process [chain-of-thought process] has provided valuable insights that have allowed them to develop better AI models, they are also finding examples of “misbehaviour” — where generative AI chatbots provide a final response at odds with how it worked out the answer.

These inconsistencies suggest the world’s top AI labs are not wholly aware of how generative AI models reach their conclusions. The findings have fed into broader concerns about retaining control over powerful AI systems, which are becoming more capable and autonomous.

Can You Really Have a Romantic Relationship With AI? (WSJ or Archive)

The harms we can anticipate or have already seen include sycophantic engagement—in other words the AI companion telling people what they want to hear, which can distort their sense of reality by isolating them from perspectives other than their own. Then there’s reinforcement and amplification of existing pathologies in thinking (such as suicidal ideation, self-deception or conspiracy theories), as well as decreased capacity for independent self-management. If people start to rely on an AI tool too much, that could affect their ability to do things like managing boredom with creative activity, or spending time alone reflecting on and evaluating their own thoughts, feelings and plans.

Thanks for reading!

Please do not hesitate to contact me if you have any questions, and check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please 👍and share it with your friends, or subscribe to my newsletter🤝.