Weekly Good Reads

Global Bond Rout, China-US Summit, Kevin Warsh, AI Financial Advice, China Growth Drivers, Inference Shift (AI)

Welcome to Weekly Good Reads. As a 25-year investment practitioner, I aim to share insights and topical perspectives on investing, the economy, and AI/productivity. I sometimes write essays on investing, have conversations with great (female) investors, and provide leisurely thought pieces on wellness.

Thank you for supporting my work. Please hit the 💛 button or share with others if you like what you read.

A special note: as I am travelling in Asia for several weeks, the next few issues of Weekly Good Reads will focus on Global Economy and Market updates, as well as investment themes and interesting observations from the region.

Sharing the quote of the week:

None of us has the luxury of choosing our challenges; fate and history provide them for us. Our job is to meet the tests we are presented.

~ Jerome Powell (credit to Axios)

Weekly archives | Investing | Ideas | Index of charts and terms | Conversations with Investment Managers

Market and Data Comment

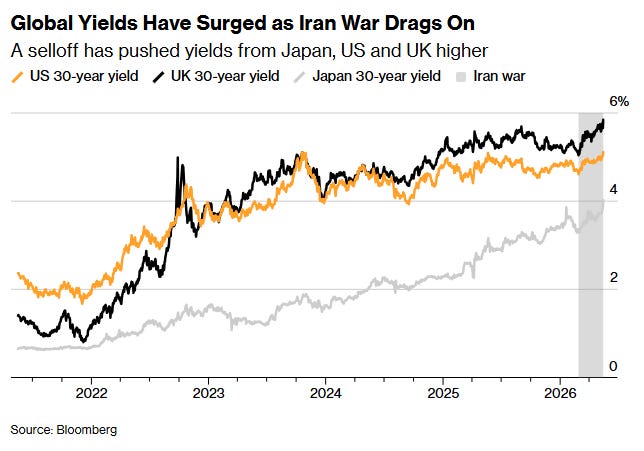

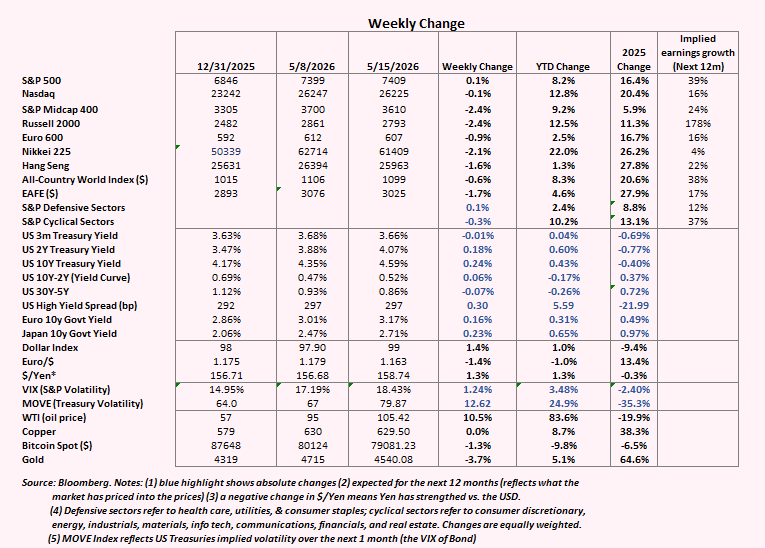

The latest synchronised sell-off in bonds that broke ranges across the US, UK, Japan, and France tells us this bond sell-off is not a local but a structural story, where “the developed world has too much debt, too little fiscal discipline and no political appetite for fixing either”, said Barclays.

US, Euro, and Japan 10-year bond yields rose 24bp, 16bp, and 23bp to 4.59%, 3.17%, and 2.71%, respectively. The MOVE Index (bond implied volatility) jumped 12.6 points to almost 80 points in the past week ending Friday.

Each of the US, UK and France has a fiscal deficit that exceeds its nominal GDP growth. For example, the 30-year bond yield touched the highest level since 2007 and is now at 5.18% at the time of writing as of US Tuesday morning. The Congressional Budget Office expects federal debt to go from 100% of GDP today to 120% by 2036, when the US fiscal deficit is already at 6.5%. No wonder Treasury bond holders are demanding more premium to hold long-duration bonds.

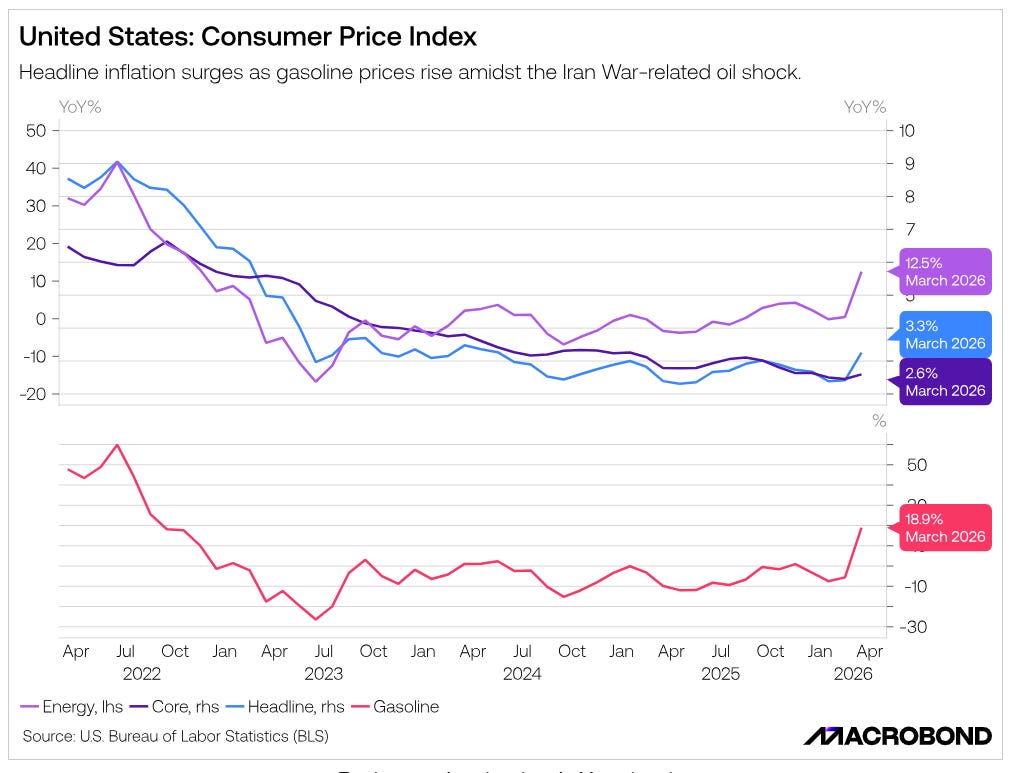

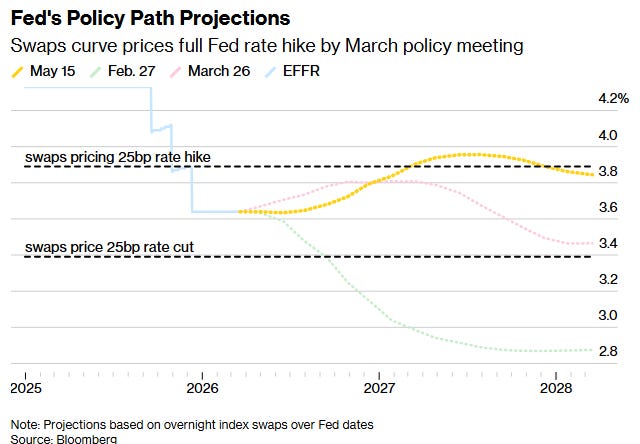

Energy price shock adds fuel to the fire, with the April US CPI rising 0.64% m/m and 3.8% y/y, and core CPI, 0.38% m/m and 2.8% y/y, necessitating the central banks to hike, not cut, which will keep interest expense high on their existing debt. The US swap market now prices in a 25bp hike from the Fed by March 2027. For Europe, markets price in 3 hikes for the ECB, 2 to 3 hikes for the Bank of England, and 2 hikes for the Bank of Japan.

PPI and core PPI in April were 6% y/y and 5.2% y/y, driven by higher energy prices. Considering CPI and PPI data together, April Core PCE is likely at 0.27% m/m (3.3% y/y).

In Japan, the current policy rate is at 0.75%, but the market has priced in a 77% probability of a June hike. 30-year JGB yield has already reached 4% compared to a near-zero rate in the past 20 years.

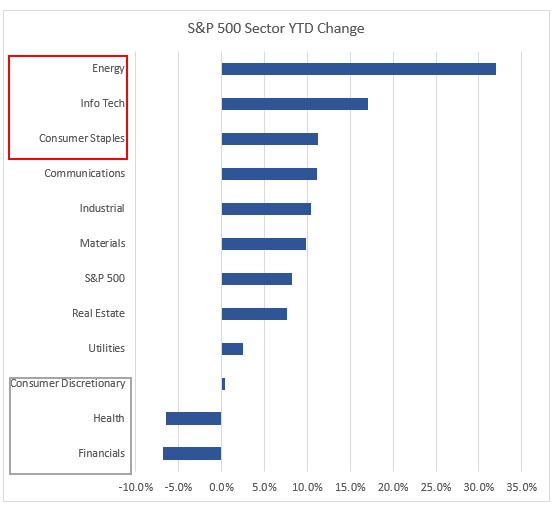

While the S&P 500 and Nasdaq managed to end flat for the week, US small-caps and the EAFE Index all fell, while the Dollar Index was up 1.4% and the crude oil price was up 10.5%.

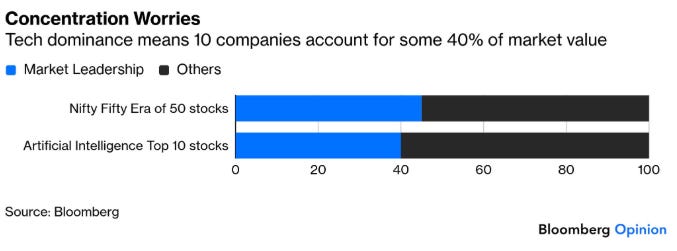

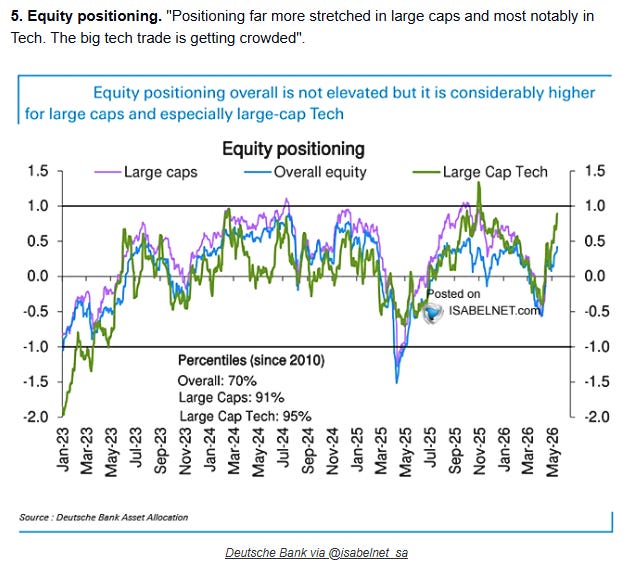

From the graphs below, equity positioning is heavily concentrated in large-cap tech (95%) vs. overall equity (less than 50%). The top 10 tech stocks in the AI era make up 40% of the market value of US stocks, with the percentage of stocks outperforming the S&P 500 Index at a low 22% over the past 30 days, the third-lowest reading since 1996.

While the expectations for last week’s Trump-Xi meeting were low and both parties managed to establish a sense of stability, there was very little tangible progress: no confirmed new contracts for US companies, no common approach to reopening the Strait of Hormuz (although Xi, while meeting Putin, also called for a ceasefire in the Middle East and the end of the war).

And as SCMP reported, the US remains set on its containment policy on China and utilizes non-tariff strategies against China: institutionalised legal restrictions, full-chain logistics control, and targeted technological blockades. China will not blindly compromise but stand firm to maintain stability. The November deadline on tariff extension and whether the extra 24% tariff will be implemented should be watched. So far, Trump-Xi have achieved a tariff truce but not a trade truce.

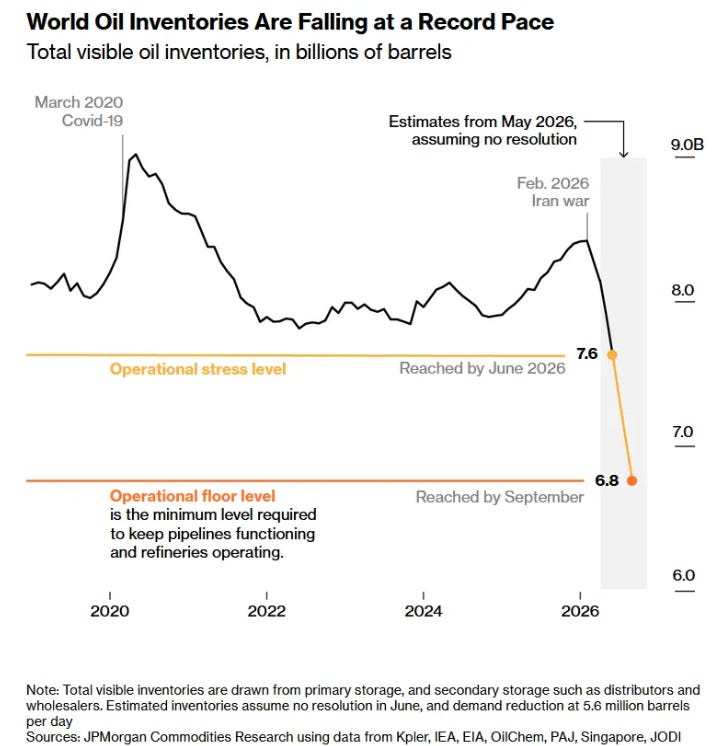

Meanwhile, with no real progress on US-Iran negotiations, world oil inventories could fall below 8 billion barrels per day by June 2026, and according to JP Morgan, when that happens, things start to fail, which exerts tremendous stress on the markets. Prices have to rise to destroy demand to match this significant drop in supply.

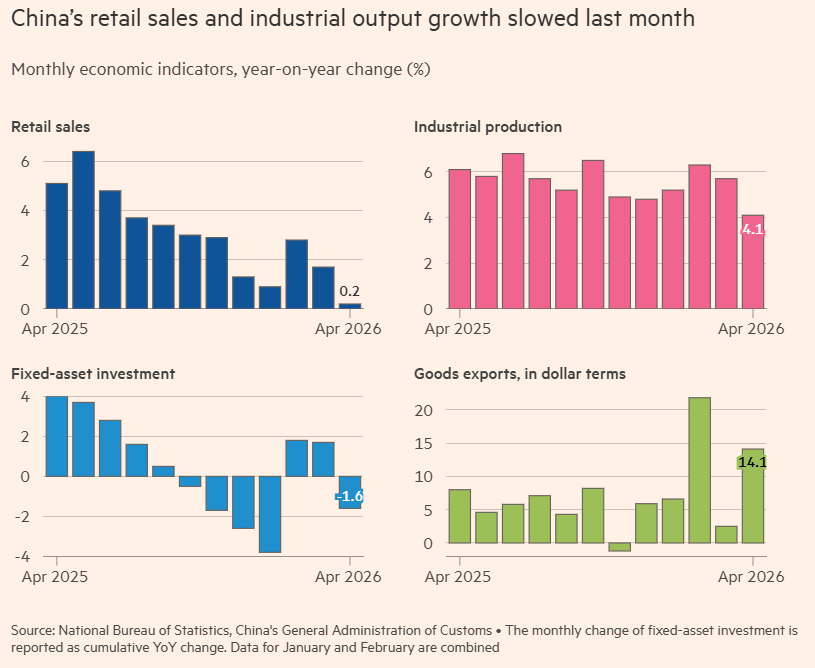

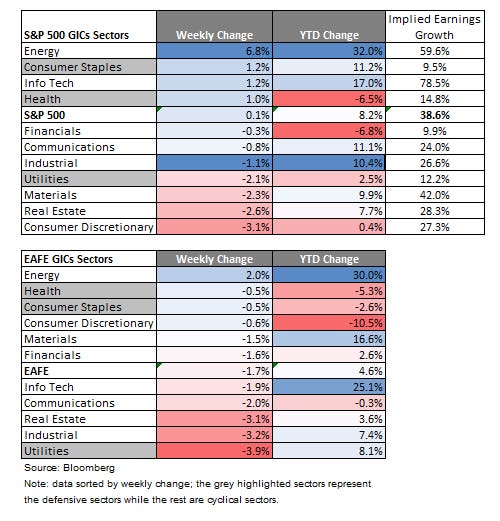

As the world is grappling with the energy supply shock, the latest growth figures from China just show how its economy is now hit—April retail sales and industrial production were weaker than expected, while the Jan to April fixed asset investment turned negative at -1.6%. Domestic demand has been mainly driven by SOEs’ investments and manufacturing, as well as increased crude oil production, while exports continue to be strong due to tailwinds from AI and energy transition and China’s supply chain resilience (see more on Investment Note below).

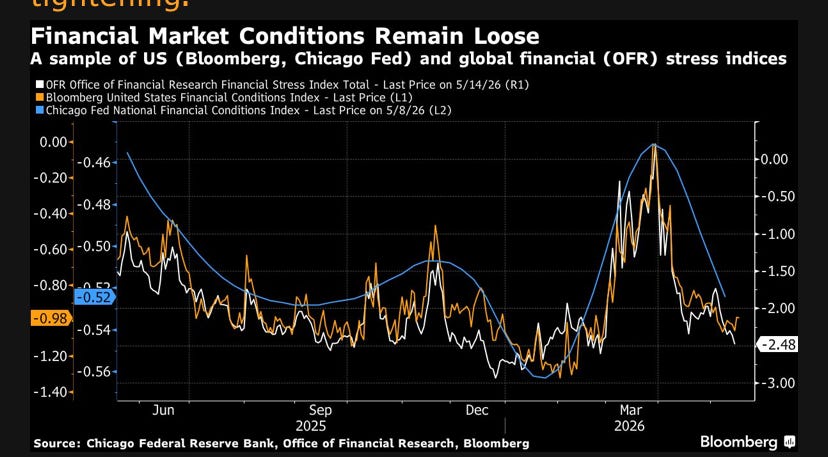

There are positives—so far, financial conditions remain loose, VIX (S&P implied volatility) has not spiked, high yield spread has stayed tight, while bond volatility has not spread to other areas of credit.

This week, we are monitoring the FOMC April minutes on May 20, the US April housing starts and the May S&P Composite PMI on May 21, the Euro Area and UK April inflation on May 20 and the Euro Area and the UK May preliminary Composite PMI on May 21, and Japan’s April nationwide CPI on April 22.

We will also closely watch Nvidia’s Q1 earnings with a focus on its Blackwell sales and forward guidance. SpaceX's S-1 IPO registration statement should also be imminent, given that SpaceX has reportedly selected Goldman Sachs for the IPO.

Economy and Investments (Links)

How the World Has Avoided an Oil Catastrophe So Far (The Economist or Archive)

The tide of non-Gulf barrels narrowed the supply gap to roughly 8m b/d. Enter the second force: in the same four weeks big oil-buying regions imported 11m b/d less petroleum than a year before. China’s purchases alone dropped by 6.6m b/d (see chart 3). The country’s refiners have even resold some cargoes they had pledged to buy from west Africa and beyond to other Asian buyers.

Global Bond Selloff Worsens as Rising Oil Prices Spook Investors (Bloomberg or Archive)

The selloff came as crude oil prices climbed and the US-Chinese summit failed deliver any breakthroughs toward ending the war in Iran. That’s compounding worries sparked by back-to-back US reports that revealed a sharp rise in consumer and wholesale prices, fueling speculation that the Federal Reserve and other central banks will need to shift to tightening monetary policy.

Goodbye Powell, Enter Warsh (Axios and WSJ) and a great read by Stay-At-Home Macro (SAHM) on Powell’s words that matter.

Target Date Funds: More Flawed Than Advertised (Jesse Cramer—Best Interest)

Key Takeaways: • Target date funds are designed as all-in-one retirement portfolios that automatically adjust risk over time. Their core mechanism is the "glide path," shifting from stocks to bonds as retirement approaches. • Most target date funds are structured as "funds of funds," investing in underlying mutual funds or ETFs. • The average target date fund underperforms a comparable index-based benchmark by ~1% annually. • The "curse of average" means no single glide path can suit every investor's needs. • Effective portfolios rely on four ingredients: risk level, diversification, low cost, and behavioral fit. • Some target date funds (e.g., Vanguard, BlackRock, Fidelity Index) are significantly better than others.

Half Of Americans Get Financial Advice From AI, But Is It Any Good?

They found, in essence, that the answers you get from an AI are about as good as the questions you ask. Their findings appear in a working paper titled “AI Financial Advice: Supply, Demand, and Life Cycle Implications.”

For the most part, AI chatbots counseled their human correspondents to make sound financial moves: Save money for emergencies. Invest in the stock market, favoring low-cost index funds. Limit your exposure to risky investments, especially as you get older.

But AI struggled, the researchers found, with some of the subtleties of investing.

Investment Notes from Asia: What’s Driving the Chinese Economy in 2026-2027

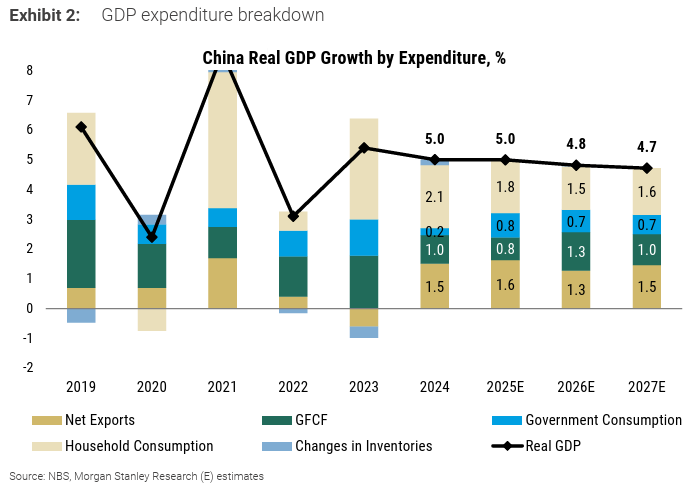

Morgan Stanley has recently slightly upgraded China’s real GDP growth forecasts by 0.1% to 4.8% for 2026E and 4.7% for 2027E. However, this masks a highly polarized “two-speed economy.”

Cyclical momentum is entirely supply- and export-driven, being powered by global AI capital expenditure and a clean energy infrastructure super-cycle. At the same time, domestic demand, consumption, and corporate pricing power remain deeply depressed by structural labour market slack and multi-year property adjustments. With aggregate growth safely within Beijing’s target zone, additional fiscal top-ups or central bank rate cuts appear off the table.

Key Growth Drivers (2026–2027):

The Global AI Capex Super-Cycle: With the global semiconductor market projected to cross $1 trillion in 2026, China’s deep hardware supply chain is gaining significant market share. Accelerated domestic AI chip localization and data centre buildouts are contributing 0.2 to 0.3% annually to real GDP.

Energy Transition Super-Cycle: Geopolitical friction in the Middle East has accelerated global demand for grid infrastructure and renewables. China controls >80% of critical solar manufacturing stages; combined exports of solar, batteries, and EVs hit a record $21.9 billion in March (up 70% y/y).

Strategic Shock Insulation: Unlike previous cycles where oil spikes penalized Chinese manufacturing, an insulated, diversified energy mix and expanded strategic oil reserves mean Chinese factories are running uninterrupted, allowing them to capture incremental global market share. Nominal goods export growth is projected at 10% y/y for 2026 by Morgan Stanley.

The Domestic Drag: The “Low-Employment” Export Sector:

A severe transmission bottleneck prevents export wealth from feeding back into the domestic economy, causing household consumption to decelerate to a muted 3.7% in 2026 (below headline GDP).

Capital-Intensive Export Mix: China’s export engine has shifted from labour-intensive assembly to automated sectors (EVs, advanced shipbuilding, chips, power grids). Consequently, each incremental export dollar generates fewer jobs than in past cycles.

The AI Paradox: Amid weak corporate earnings, firms are leveraging generative and agentic AI tools primarily for white-collar corporate cost-cutting, creating severe structural friction for the 12 to 13 million graduates entering the labour market annually. Urban surveyed unemployment hit a 13-month high of 5.4% in March.

Property Drag: Housing construction continues to subtract ~2% from nominal GDP. New construction starts (-22% y/y) and land sales (-24% y/y) confirm that property remains a persistent, multi-year drag.

Questions Investors Should Consider:

As China is operating with a high-tech macro engine and a weakened micro reality, in thinking about Chinese investment, it is good to consider:

(1) Is China a thematic tech/energy story rather than a macro reflation play, given industrial outperformance, as driven by government policy, concentrates within AI hardware, automation, and green capital goods?

(2) Consider the AI J-Curve: if Beijing permits aggressive white-collar AI labour displacement to win the high-tech race with global peers, can the political economy sustain a soft labour market without stepping up on demand-side stimulus and consumer wealth transfers? And would a stronger RMB (given rising trade surplus) offset the supply-chain competitiveness that is keeping China’s headline growth afloat?

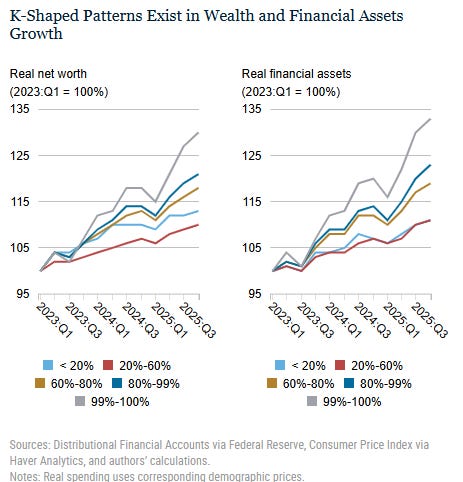

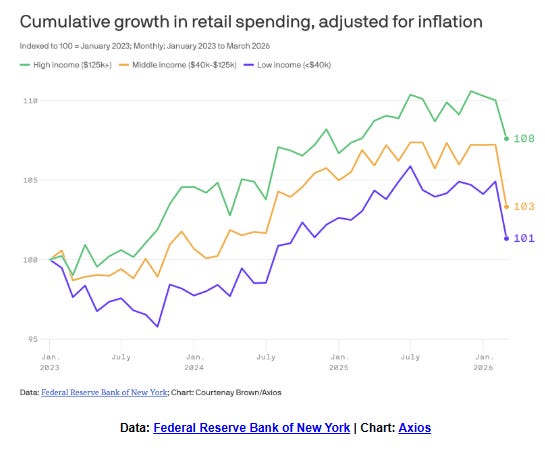

One Chart You Should Not Miss: K-Shaped Economy

…real net worth has displayed a K-shaped pattern since 2023, with higher income groups experiencing higher cumulative wealth growth, relative to the first quarter of 2023, than lower income groups in nearly every quarter. The bottom quintile was an exception as its net worth grew slightly faster than that of the middle 40 percent. Thus, real net worth of the top percentile grew by more than 25 percent, while that of the middle 40 percent grew by less than 10 percent. This growth in net worth has been driven by large increases in financial assets for higher-income groups and especially the top percentile (right panel below). Given these wealth patterns, it is not surprising that higher income groups also increased their retail spending by more than lower income groups.

~ New York Fed

On AI/Productivity

The Inference Shift (Stratechery)

I have previously made the case, including in Agents Over Bubbles, that we have gone through three inflection points in the LLM era:

ChatGPT demonstrated the utility of token prediction.

o1 introduced the idea of reasoning, where more tokens meant better answers.

Opus 4.5 and Claude Code introduced the first usable agents, which could actually accomplish tasks, using a combination of reasoning models and a harness that utilized tools, verified work, etc.

All of this falls under the banner of “inference”, but I think it will be increasingly clear that there is a difference between providing an answer — what I will call “answer inference” — and doing a task — what I will call “agentic inference.” Cerebras’ target market is “answer inference”; in the long run, I think the architecture for “agentic inference” will look a lot different, not just from Cerebras’ approach, but from the GPU approach as well.

OpenAI launches ChatGPT for personal finance, will let you connect bank accounts (TechCrunch)

OpenAI has partnered with the financial connection service Plaid to manage the account connections. Users can connect to over 12,000 financial institutions, including Schwab, Fidelity, Chase, Robinhood, American Express, and Capital One. Once users connect these accounts, they will see a dashboard of their portfolio performance, spending, subscriptions, and upcoming payments…

Generalized chatbots are designed to answer anything, leading people to ask questions about data-sensitive topics such as health, finance, and personal life. AI companies are realizing this and making specialized products for these sectors. Both OpenAI and Anthropic have launched health-related tools. Earlier this month, Perplexity launched its own financial research product based on its Computer agent.

Thanks for reading!

Please do not hesitate to contact me if you have any questions, and check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please give a👍, share it with your friends, or subscribe to my newsletter🤝.

Interested in building a globally diversified, customized, and optimized investment portfolio that aligns with your objective and risk profile?

Creating yours at Lumen R4A - click “Guest” - it’s free!