Weekly Good Reads

May Momentum, Narrow Breadth, Memory Chips, US IPOs, SpaceX IPO, Nvidia at Computex

Welcome to Weekly Good Reads. As a 25-year investment practitioner, I aim to share insights and topical perspectives on investing, the economy, and AI/productivity. I sometimes write essays on investing, have conversations with great (female) investors, and provide leisurely thought pieces on wellness.

Thank you for supporting my work. Please hit the 💛 button or share with others if you like what you read.

A special note: as I am travelling in Asia for several weeks, the next few issues of Weekly Good Reads will focus on Global Economy and Market updates, as well as investment themes and interesting observations from the region.

Sharing the quote of the week:

Ben Graham taught me 45 years ago that in investing it is not necessary to do extraordinary things to get extraordinary results. In later life, I have been surprised to find that this statement holds true in business management as well. What a manager must do is handle the basics well and not get diverted.

~ Warren Buffett, Berkshire Hathaway Letters to Shareholders: 1965-2024

Weekly archives | Investing | Ideas | Index of charts and terms | Conversations with Investment Managers

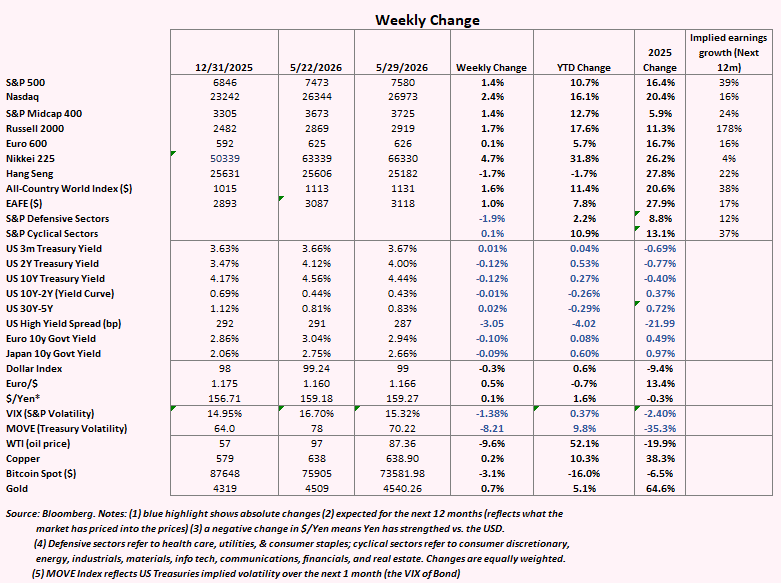

Market and Data Comment

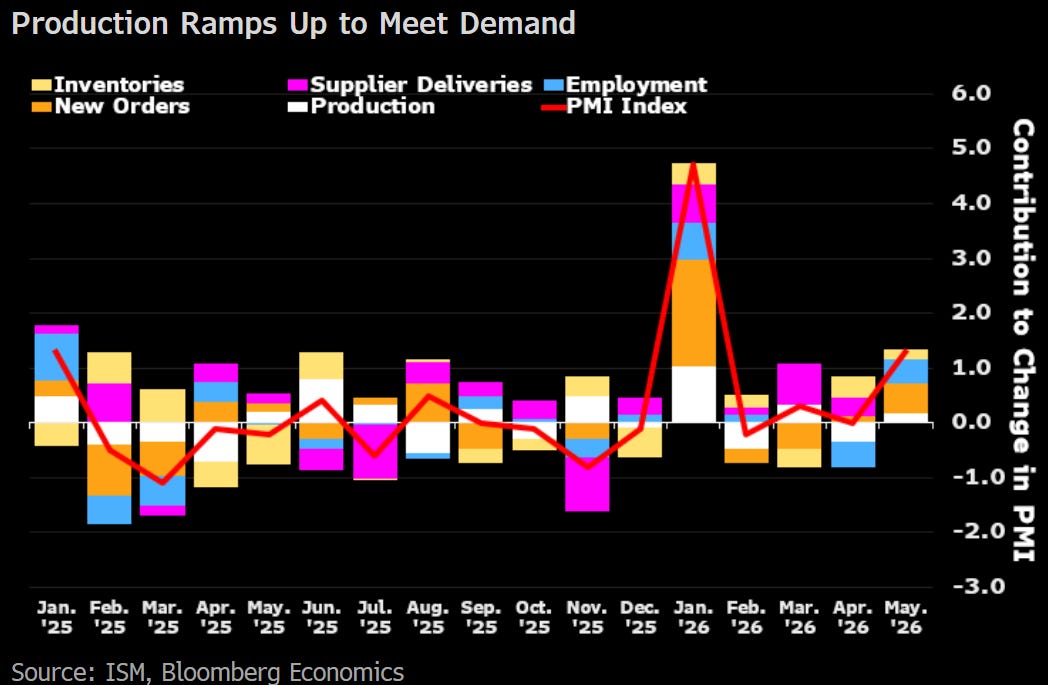

The US May ISM rose 1.3 points to 54, reflecting expansion in factory demand associated with the AI capex boom. The New Orders and Employment components were particularly strong. However, the input price (price paid index) is elevated (82.1 vs. 69.4 in May 2025), akin to the extreme global supply chain pressures during 2021 to 2022. April’s estimated job openings surged 731k to 7.6 million, with the increase mainly coming from professional and business services (likely AI-related). Private payrolls (ADP) surged 122k in May, the largest of 11 straight m/m gains, showing labour-market momentum.

Supported by the economic data, the global markets decided to keep going like an Energizer bunny despite no final agreement to extend the US-Iran ceasefire for 60 days, while negotiations to end the war continue.

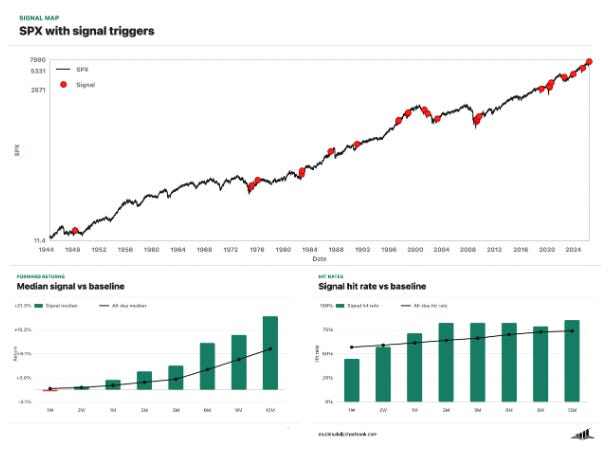

Dailychartbook’s historical studies show that when the S&P 500 gains over the past 2 months exceeds 16%, 3-month, 6-month, and 12-month average returns can reach 5.1%, 9.9%, and 15.6%.

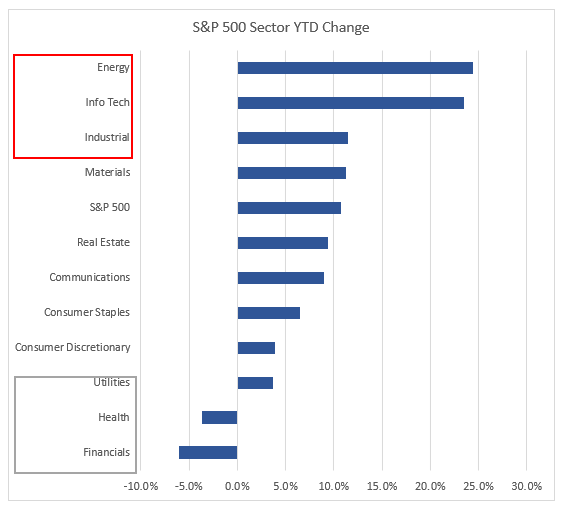

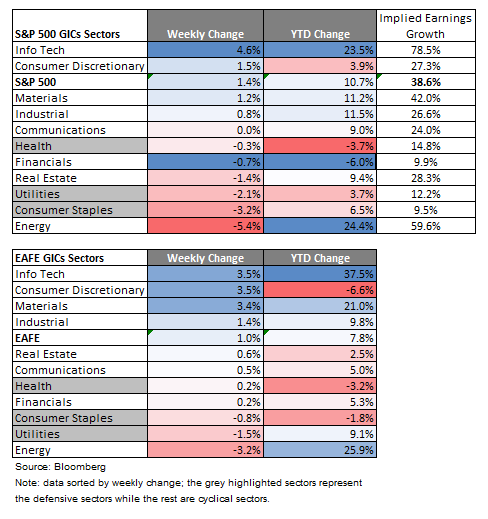

As many have noticed, while the S&P 500 has risen ~10% YTD, the forward PE has fallen from 22.3x at the start of the year to about ~21 today (in the bottom quintile of its 1-year range), mainly driven by large upward revisions across Big Tech stocks, i.e., the stock market rally has been driven by EPS upward revision and not multiple expansion (usually associated with speculative bubbles).

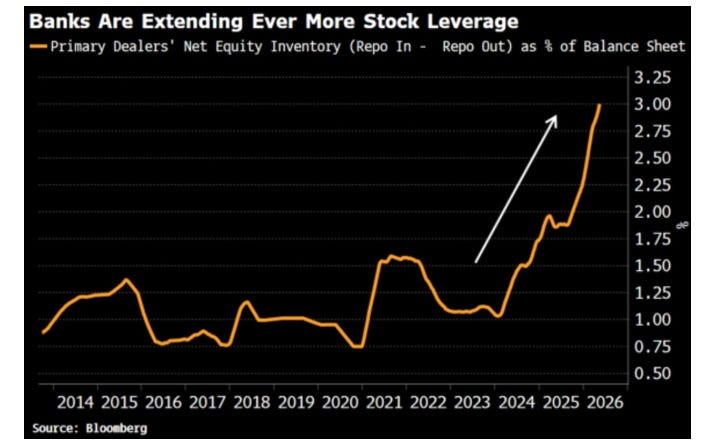

However, Bloomberg’s strategist pointed out that the stock rally has been financed by rising retail leveraging financed by banks, with bullish trades in options (buying calls or selling puts) in mega-cap Tech stocks near a record high — these could accelerate a stock price reversal pretty quickly.

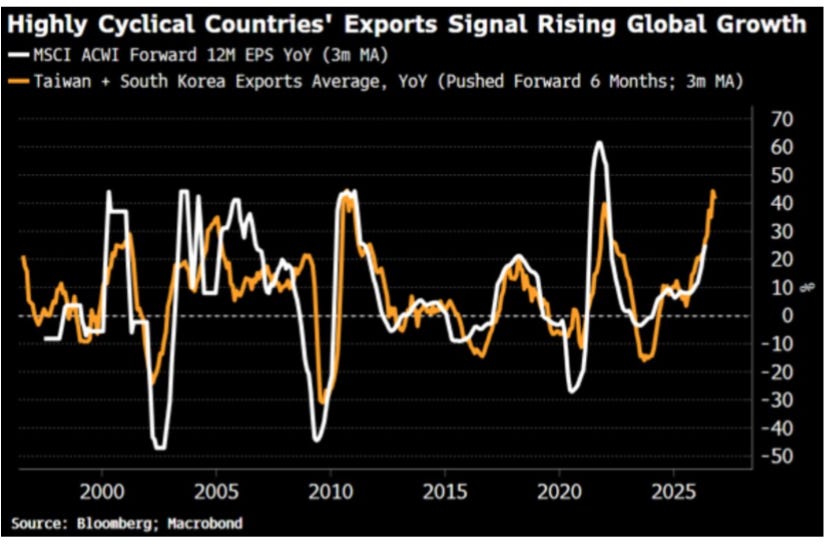

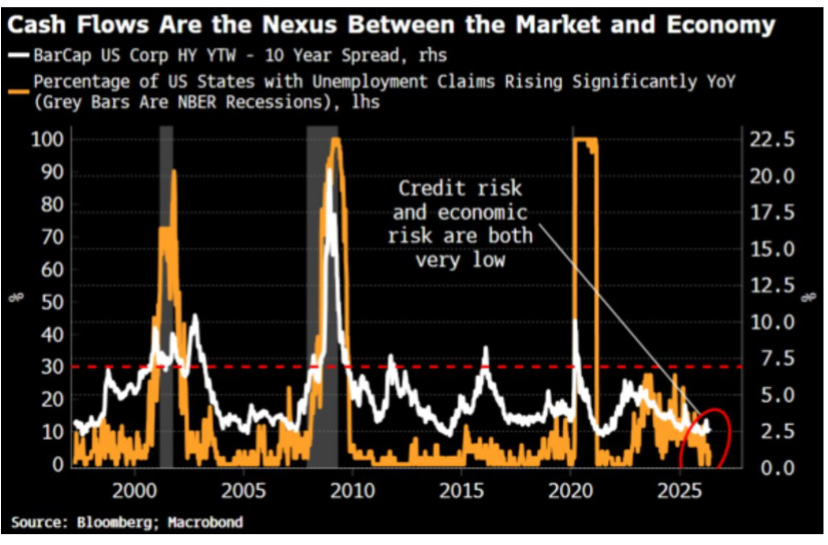

The good news is that there is a positive economic growth impact when earnings and cash flow are rising, providing more stability to the other part of the capital structure, like debt. This is illustrated in rising exports in chip manufacturing countries like Taiwan and South Korea (its May exports rose 60.7% y/y, led by semiconductors, reflecting strong AI and data centres investments). (Read more in Investment Note from Asia below).

The other indicators of stability are low credit spread and relatively low unemployment rate and claims, which can support the retail leveraging mentioned earlier. Any signs of recession, prompted by continued energy supply shock and inflationary pressures, rate hikes, rising borrowing costs, profit slowdown, etc., could accentuate a market correction. US April core headline PCE inflation and core PCE inflation were at 3.8% y/y — propped up by energy inflation (headline) and AI-related inflation (core). In the Euro Area, countries’ inflation ranged from 2.8% y/y (Germany) to 3.6% y/y (Spain). April Harmonised Index of Consumer Prices (HICP) for the Euro Area rose to 3.2% y/y (from 3% in April).

For the remainder of the week, we will watch out for the May US nonfarm payrolls, unemployment rate, and average hourly earnings on June 5 and Nominal/Real Wages per worker for April in Japan on June 5.

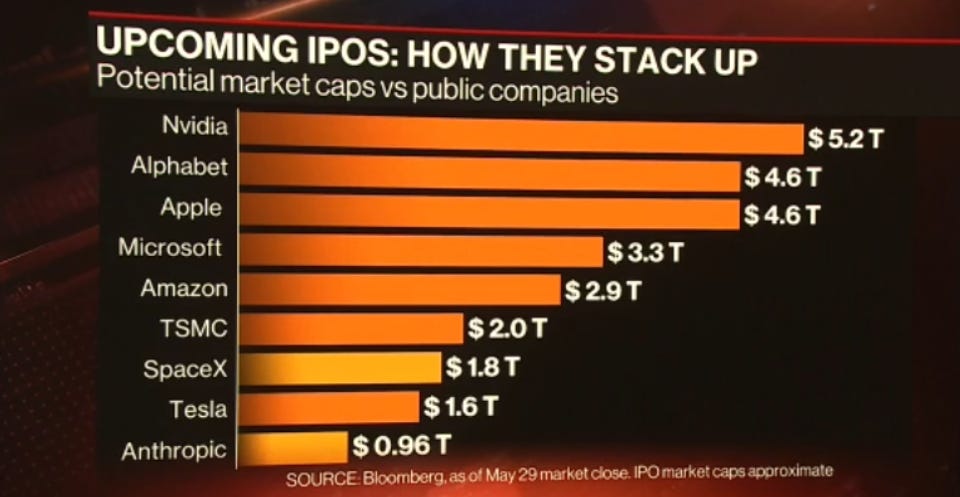

On the US IPO fronts, watch out for the three upcoming mega IPOs: SpaceX (planned for June 12), Anthropic, and OpenAI are collectively targeting ~$200bn-odd. However, this is still small compared to the $79 Trillion of market cap of the Russell 3000 (see Econ/Invest #5).

Economy and Investments (Links)

Vanguard Is the Costco of Finance, According to the Hosts of ‘Acquired’ (WSJ)

Bogle [Vanguard’s founder] ran the numbers: in seven of the prior 11 years, if you had owned the whole S&P 500 with no fees, you would have beaten half the active managers. And over the full decade, from 1964 to 1974, you would have outperformed 78% of them.

Bogle’s big insight was not that a passive index of the entire market provided magically better returns. After all, its returns are by definition average! It was that running this passive strategy would be inexpensive, and thus wouldn’t require charging large fees to the investor clients. And it was precisely these low fees, compounded over large periods of time, that created the outperformance compared with active managers

May Momentum (Axios)

“The everything-semiconductors rally has allowed the Philadelphia Semiconductor Index to reach some of the most short- and medium-term overbought conditions since the 2000 period,” technical stock analysts for JPMorgan wrote Thursday, noting that the “comparison raises immediate concerns about a ‘bubble.’”

- They stressed, however, that while the recent surge in chip stocks has been extreme, the rally would have to persist for several more months “to match the extremes achieved in the late-1990s and 2000 period.”

Gold Is Set to Be a Drag on Portfolios in 2026: Macro View (Bloomberg Terminal)

Trader positioning suggests that the charm of gold may be starting to wear off. Open positions among investors who don’t have a commercial need to hedge against gold prices totalled under 155,000 contracts as of May 26, after peaking at 315,000 contracts in 2024 and a median of 195,000 over the past five years. While gold has bounced off its recent lows, it has a long way to go before it can reclaim its peaks. History suggests that won’t happen in a hurry.

Global Roadshow Insights (Citadel Securities)

Bottom line: The current equity rally remains characterized by a powerful but increasingly unusual combination: historically narrow breadth alongside exceptionally strong earnings growth. Rather than a speculative bubble driven purely by multiple expansion, mega-cap technology earnings and revisions have continued to outpace price appreciation, allowing valuations to compress even as equities move higher.

At the same time, intense performance-chasing, systematic positioning, and flow-driven momentum have created a market where many investors still feel underinvested (despite equities sitting at highs) and in a state of nervous bullishness, actively searching for the catalyst capable of disrupting the current momentum regime. This has fueled increasingly rare dynamics such as the “spot up, vol up” behavior seen throughout May.

Ultimately, the pain trade likely remains higher for now. But the market is also becoming progressively more dependent on the same leadership cohort, the same systematic flows, and the same momentum dynamics continuing to work simultaneously beneath the surface.

Can the Stock Market Swallow SpaceX, Anthropic and OpenAI? (The Economist or Archive)

Together, the three giga-IPOs may add as much as $4trn to the market value of listed American companies in a matter of months.

How on Earth will the stockmarket handle this? Headlines predict a “trading frenzy”. Steve Sosnik, chief strategist at Interactive Brokers, one of the world’s biggest online trading platforms, has warned of the “existential risk” the listings pose. A particular worry is that compilers of stockmarket indices will grant the gigantic trio fast-track entry to their benchmarks. That would prompt tracker funds with trillions of dollars in assets to buy the newly minted shares days after they are issued. After exhausting a big pool of buyers straight away, who will be left?

The answer is: lots of investors in an extraordinarily deep and liquid market. Unprecedented as the serving of supersized IPOs is, America’s extraordinary stockmarket will gulp it down. In the years to follow, though, expect some indigestion.

Related: The SpaceXIPO…It’s Worse Than You Think

[No matter how much you like the investment thesis, be sure you know what you are getting into - a great video by Casual Finance for review]

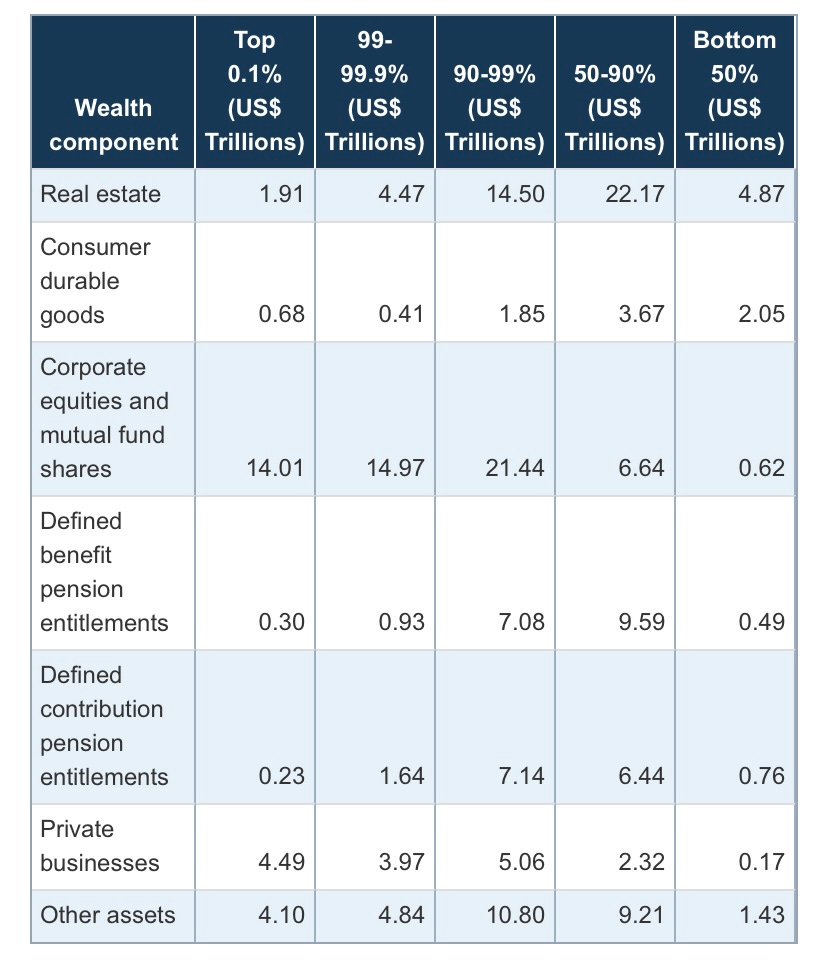

One Chart You Should Not Miss: US Assets Distribution by Wealth Group (Q42025)

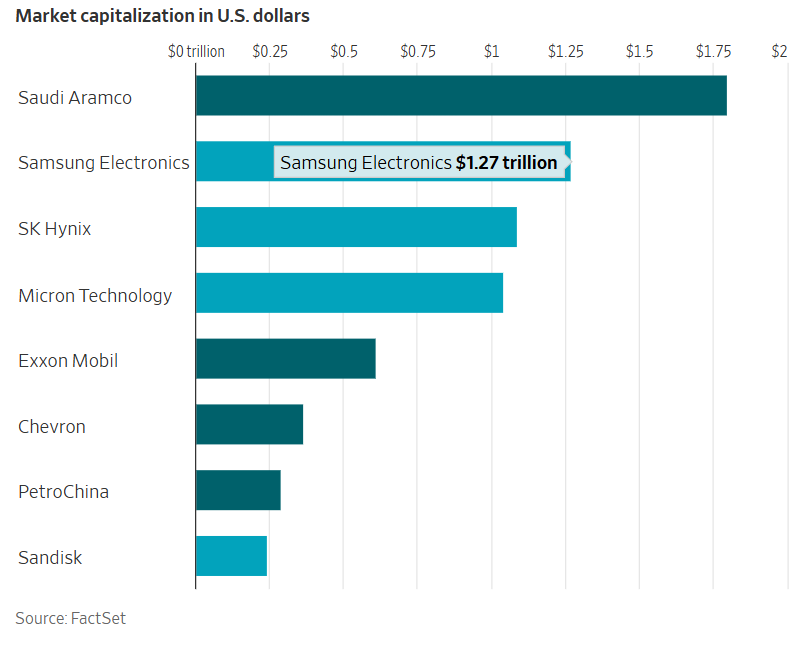

Investment Notes from Asia: Memory Chips and Highlights from Computex (Jensen Huang’s Keynote)

A recent WSJ article highlighted that memory chips — the components that store and process data — have quietly become more valuable than oil in today’s economy. The world’s largest memory makers, including Samsung, SK Hynix, and Micron, are now collectively worth more than the biggest oil companies, fuelled by the explosive demand from AI (see chart above).

Data and computing power are now as essential to modern economies as energy once was. And the industry is changing its business model.

Memory is well-known for its volatile, “commodity-like” market, where prices swing sharply based on supply and demand.

But AI demand is so strong that supply cannot keep up, giving chipmakers more bargaining power. They are increasingly signing long-term contracts with major customers like Microsoft, Amazon, and Google. These agreements lock in future demand and pricing, making revenues more predictable and reducing the industry’s historical boom-bust pattern.

Despite the massive run-up in valuations, these companies may not be as expensive as they seem. Strong and more stable earnings are making their stocks look relatively cheap compared to the broader tech sector.

For example, some memory firms are trading at much lower P/E ratios than the average semiconductor company. That means investors are paying less for each dollar of future profit, even as those profits are expected to grow rapidly. If the shift toward long-term contracts continues, memory chips may not only rival oil in importance but also become a more stable and attractive investment.

Nvidia at Computex

At Computex, one of the world’s largest technology B2B trade shows held in Taipei, Jensen Huang (Nvidia’s CEO) announced a new chip launch — the RTX Spark Superchip, a combination of microprocessor and graphics chip, built with MediaTek’s help and running Microsoft Windows on Arm — that will debut in laptops and desktops (targeting the premium segment) this fall. The combination of the RTX Superchip, which includes a CPU with up to 20 computing cores, and the Blackwell-generation GPUs with 6,144 cores will enable them to handle large AI models and high-end games.

Jensen also highlighted the superior performance of the Vera Rubin CPUs, Nvidia’s microprocessors for AI data centres, which is ~1.8x faster at essential AI-related workloads than Intel’s technology, prompting investors to rethink competitors such as AMD and Intel.

Jensen alluded to software companies which embrace AI Agents, which can support the software sector relief rally. Nvidia is also working with major robotics companies to power the next generation of physical AI. “Every industrial company will become a robotics company,” according to Jensen.

The key takeaway for investors: the announcement serves as another reminder that the AI trade is increasingly expanding beyond data centres and into consumer hardware.

On AI/Productivity

Starbucks Scraps AI Inventory Tool Across North America (Reuters)

Starbucks (SBUX.O), opens new tab terminated an AI program workers used for automating certain inventory counts this week, nine months after deploying it across its North American stores, according to an internal newsletter reviewed by Reuters and two people with direct knowledge of the situation.

The tool was part of CEO Brian Niccol’s efforts to fix the coffee chain’s persistent product shortages that he has blamed for hurting sales. The app - designed to improve Starbucks’ visibility into shortages at stores - frequently miscounted and mislabeled items, such as confusing similar milk types or missing them altogether, Reuters reported in February.

Nvidia Expands AI Push with Cosmos 3 World Model (Axios)

Bottom line: Nvidia's bet is that the next wave of AI won't just answer questions or generate images — it will need to predict, simulate and act in the physical world, and Nvidia wants its open models and infrastructure to be the place developers start.

🙌 Disclaimer: The suggested readings are for reference only and are not investment advice.

Thanks for reading!

Please do not hesitate to contact me if you have any questions, and check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please give a👍, share it with your friends, or subscribe to my newsletter🤝.

Interested in building a globally diversified, customized, and optimized investment portfolio that aligns with your objective and risk profile?

Creating yours at Lumen R4A - click “Guest” - it’s free!