Weekly Good Reads: 5-1-1

US Jobs, Recession Probabilities, Multitasking, Money Machine, Equity Risk Premium

Welcome to Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

In this Weekly, I share insightful/essential readings, charts, and one term, incorporating some of my market observations and weekly change tables. I look beyond data and share something enlightening about life, health, technology, and the world around us 🌍!

Here’s the quote of the week:

Success is going from failure to failure without losing your enthusiasm.

– Winston Churchill

Feedback is important to me, so if you like the Weekly, please “heart” it, comment, share it, or subscribe! Thank you so much for your support🙏.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

In case you have missed my recent piece:

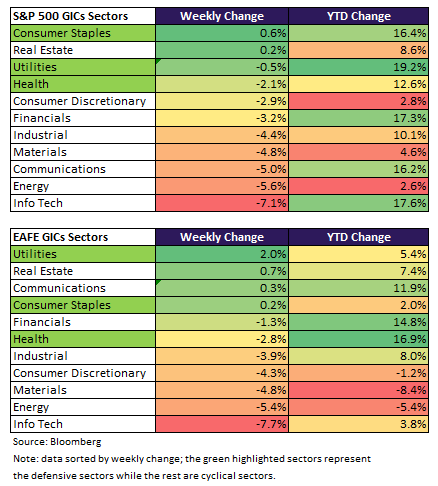

Market and Data Comments

This week’s biggest data, the mixed August US jobs data, left the market guessing whether the Fed will cut 25 or 50bp in the September FOMC meeting.

Payrolls were +142,000 in August (vs. 165k Bloomberg median forecast) though the previous two months were revised downward by 86k jobs. On a 3-month average basis, job growth was 116k compared with the 12m average of 202k. On the other hand, the unemployment rate was technically flat (4.22% vs. 4.25% prior) while the average hourly income jumped 0.4% in August (0.2% prior).

With layoffs and unemployment increasing amid a decline in job openings to 7.67 million (the lowest since 2021), and a weak Beige Book (9 out of 12 districts record flat or declining economic activity), the market has priced in a 70% chance of a 50bp cut in September and a total of 213bp cut by mid-2025. Most economists think the Fed will start with a cautious 25bp cut to not alarm the markets, but the risk is the labour market may accelerate its weakening.

A very interesting chart from JP Morgan’s strategist Nikolaos Panigirtzoglou below shows the divergence of recession probabilities implied across different asset classes with the Treasury and base metal markets pricing in a 60% chance of a recession compared to less than 25% for the rest.

The rapid drop in 2y and 5y US government yields (another 20bp+ for each this week). an 8% drop in WTI (oil) prices, the US 2Y-10Y yield curve becoming positive (un-inverting), and global equity markets selling off around 4% this past week, signal that fear of a recession has heightened.

A recent Federal Reserve research paper found that Fed policy’s impact on inflation works with an 18-month lag. By now, the economy has fully felt the impact from the Fed's 5%+ rise in interest rates.

Whether the un-inverted yield curve is good or bad for the S&P 500 depends on whether we are in a soft or hard landing (see graph below).

Elsewhere, the ECB is likely to deliver another 25bp interest rate cut (to 3.5%) in the next meeting amid weak economic recovery (Q2 GDP was revised down by 0.1% to 0.2% q/q) while the Bank of England will be watching the UK wage growth and core inflation to decide when their next cut might be.

China’s economy is flirting with deflation with manufacturing PMI in contraction, auto sales weakening, and the housing market still in a doldrum. PBOC will likely cut the bank’s Reserve Requirement Ratio by 50bp in September to counter deflationary forces and to guide mortgage rates lower.

In the coming week, we will monitor the Harris-Trump presidential debate on Tuesday, the US August CPI on Thursday, and PPI on Friday, the ECB monetary meeting on Friday, the August CPI and PPI for China on Monday, and its August exports on Tuesday.

Economy and Investments (Links):

America Still Has a Worker Shortage (WSJ or via Archive)

Wall Street Traders Suddenly Converge on Economic Hazards Ahead (Bloomberg or via Archive)

The Presidential Campaign Proposals Americans Like Best (WSJ or via Archive)

Voters welcome financial support from the government no matter which party candidate is proposing it—the top 3 being capping insulin prices at $35, elimination of taxes on Social Security and tops for service workers.

Finance/Wealth (Link):

How a Mind-Boggling Device Changed Economic History (FT or via Archive)

+ Related The FT Money Machine: How We Transformed An Iconic Invention for Virtual Reality (FT or via Archive)

The Phillips Machine below introduces the concept of the “circular flow of income” more vividly than any economic textbook can the movement of money around an economy as it facilitates the exchange of goods and services.

Wellness/Idea (Link):

Multitasking Doesn’t Work. So Why Do We Keep Trying? (Freakonomics)

STEPHEN DUBNER {Freakanomics]: For the average person, who thinks that they are quite adept at multitasking, are they deluded?

GLORIA MARK [Professor at UC, Irvine]: Yes, they are. And there’s three reasons. First of all, people may feel that they’re accomplishing more when they multitask. But people make more errors when they’re switching their attention rapidly. Another thing is that there’s what’s called a switch cost when we think we’re multitasking. A switch cost is the extra time it takes to reorient to this new task. The biggest cost that we found relates to the third reason why multitasking is bad, and that is because it causes stress. It’s not just correlation of shifting attention and stress, but it actually causes stress.

:

DUBNER: Why do we want to multitask?…But now that you’re talking about Bluma Zeigarnik, it makes me wonder if it’s driven by a different need, which is the need to resolve conflict, to get rid of that tension of the unfinished task.

MARK: I do think that plays a role, and I think there are a lot of reasons why people multitask. We found in our research that people interrupt themselves about half the time. So I do think that wanting to resolve conflicts in a number of ways—so you have this memory of, “Oh, that email that I didn’t answer.” … Very often, a thought will pop into my head, of some silly question, and I just can’t get it out of my mind, and I have to look it up on the internet to be able to resolve it. Why do I do it? It’s because the internet is so close at hand, and because I can get that answer within milliseconds, that’s why I do it. And I’ve developed a habit, and I know that there will be resolution after I look up that answer.

+ 41 Healthy Lunch Ideas (Love & Lemons)

(I know you need this one as do I!)

One Chart You Should Not Miss: Duration of Various Asset Classes

I discussed the concept of duration (usually applied to bonds) last week, but the concept can easily be applied to other asset classes including stocks and commodities.

As you can tell from the chart below, global stocks typically have a long duration (over 15 years with high-tech stocks’ duration longer than those of more stable and mature companies). Commodities have an even higher duration.

When managing your investment portfolios, your investment horizon is crucial as is your investment objective. Matching the right asset type to your investment horizon, coupled with your required return and investment capacity is key to a successful investment outcome.

(I have no association with Discipline Funds.)

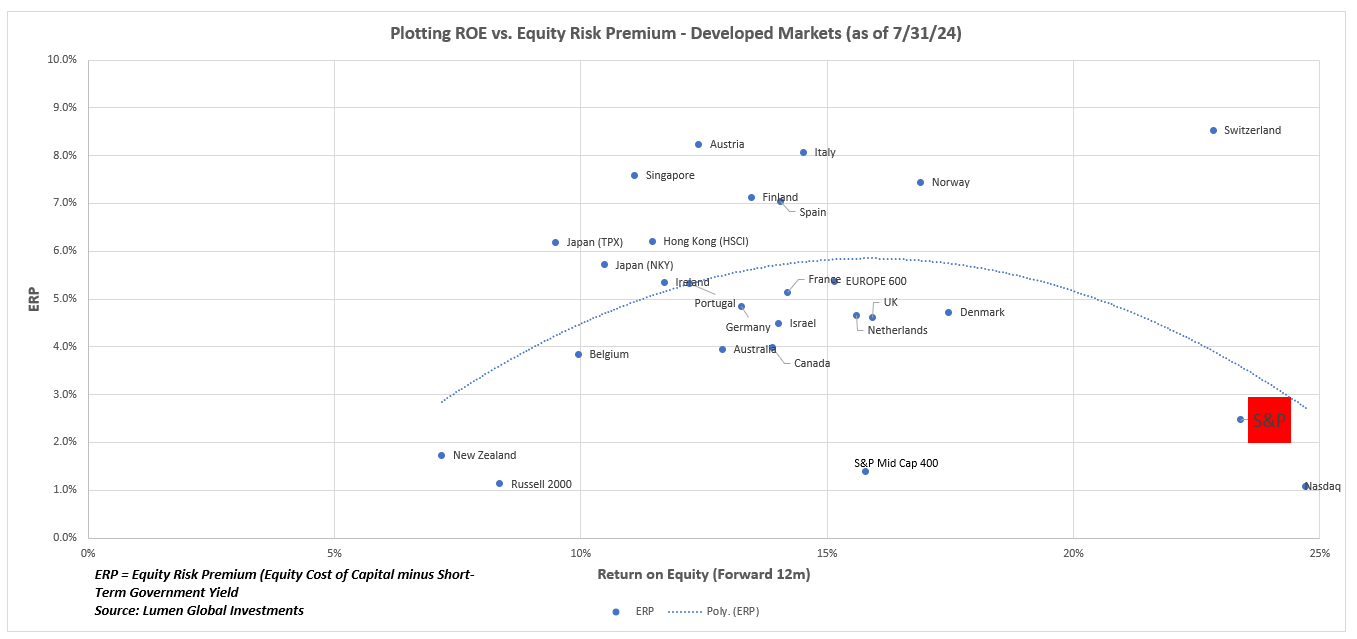

One Term to Know: Equity Risk Premium

I discussed Equity Risk Premium (ERP) here before—it is the expected stock returns over a risk-free rate (either short-term government bill or long-term government bond) within the same country.

ERP is driven by the relative value between the equity return and bond return and is a reasonable estimate of equity valuation to understand if it is cheap or expensive.

A popular way of looking at equity valuation is comparing the reverse of a market’s P/E ratio (earnings yield) with say the 10-year government bond yield. However, this runs into the problem that an earnings yield does not measure the same thing as a bond yield which is an internal rate of return - so comparing apples with oranges!

According to the valuation guru Professor Awath Damodaran in his annual Equity Risk Premium Paper, there are three ways of estimating equity risk premium:

There are three broad approaches used to estimate equity risk premiums. One is to survey subsets of investors and managers to get a sense of their expectations about equity returns in the future. The second is to assess the returns earned in the past on equities relative to riskless investments and use this historical premium as the expectation. The third is to attempt to estimate a forward-looking premium based on the market rates or prices on traded assets today; we will categorize these as implied premiums.

At my firm, we use the implied premiums as we favour measuring relative valuation looking forward not backwards. The graph below depicts the equity risk premium (equity expected returns minus the short-term government bill rate) for developed countries as of July 31, 2024.

The scatterplot shows the forward return on equity (profitability) versus the current equity risk premium of the developed markets.

A polynomial trendline is plotted (showing data breaking away from a linear line).

The higher the ERP, the higher the expected stock value above the bond value, meaning equity is relatively cheaper than a bond in the same country.

While we should not interpret any economic relationship between the ERP and ROE, the graph shows the anomaly in the US markets presented by the S&P 500, Nasdaq, and Mid-Cap. While the ERP appears low, the profitability of those stock markets beat the others which may have caused investors to bid up those markets.

[🌻] Things I Learn About AI/Productivity:

A couple of good reads on AI 😎:

The 100 Most Influential People in AI 2024 (Time) (First edition here)

A New Way to Search Google Photos (Google Blog)—Gemini-powered search function for easy search of photos.

What Do People Really Ask Chatbots? It’s a lot of Sex and Homework (Washington Post or via Archive)

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

My second favourite Churchill quote! First is ‘if you’re going through hell, keep going’.