Welcome to Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

Each week I share insightful/essential readings, charts, and one term, incorporating some of my market observations. You can find the weekly changes of the major indices or indicators in the Weekly Change charts. I also look beyond data and share something enlightening about life, health, technology, and the world around us 🌍!

Here’s the quote of the week:

The hardest part is starting. Once you get that out of the way, you’ll find the rest of the journey much easier.

~ Simon Sinek

I archived my Weeklies hereand the indexof charts and terms here. Check out my conversations with Female Investors and more, which I hope will inspire more females into finance and investment careers 🙌. Easily subscribe to my newsletter by clicking below.

Feedback is important to me, so if you like the Weekly, please “heart” it, comment or share it with your contacts. Thank you so much for your support🙏.

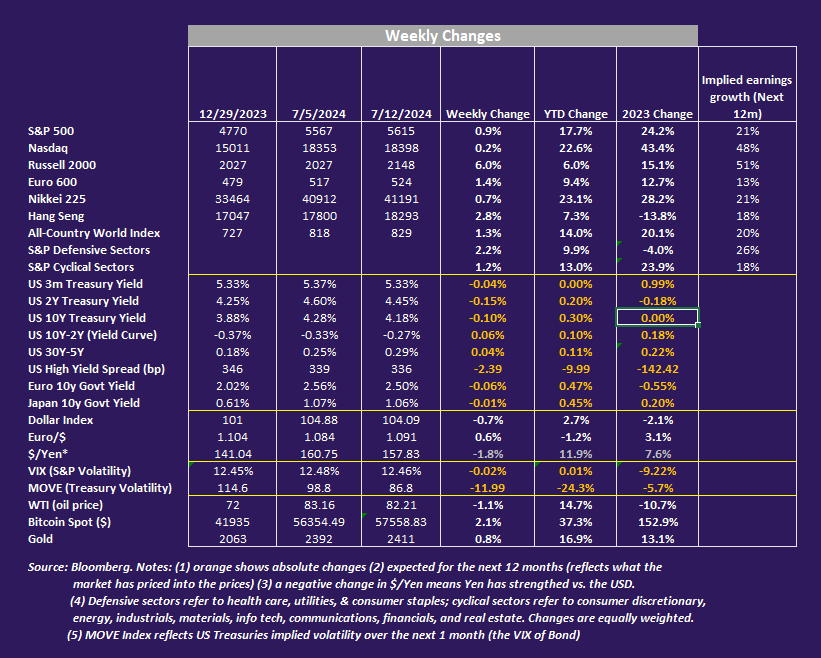

The cooling US June CPI data (-0.06% m/m, 2.97% y/y) and core CPI (+0.06%, +3.3% y/y, 2.1% 3m annualized) sparked tremendous price actions in the stock, bonds, and currency markets in the last two days of the past week as these numbers are lower than expected and are even better than the “really good” May inflation report (according to Bloomberg’s Chief Economist), driven by slower increase in car prices and housing rents.

With the soft June CPI print and Fed Chairman Powell’s “new” concern on the weakening labour market (see Econ/Invest No.2) - “Elevated inflation is not the only risk we face,” Powell said. “The labor market has cooled really significantly across so many measures,” - the market has priced in between an 80 to 90% probability of a first US interest rate cut in September. Bloomberg expects June Core PCE inflation, the Fed’s preferred inflation gauge, to reach 2.5% y/y, the lowest since March 2021.

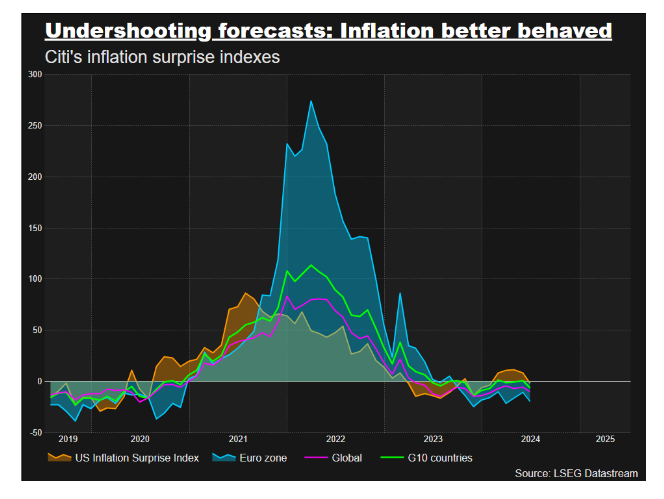

The graph below by Citibank shows inflation has been better behaved globally as indicated by the negative inflation surprise indexes this year (except in the first quarter in the US albeit inflation has slowed down in the past 2 months).

According to Barclays, the ECB is expected to cut interest rates the second time in September while the Bank of England may cut for the first time in August (despite the stronger-than-expected May real GDP number of 0.4% m/m).

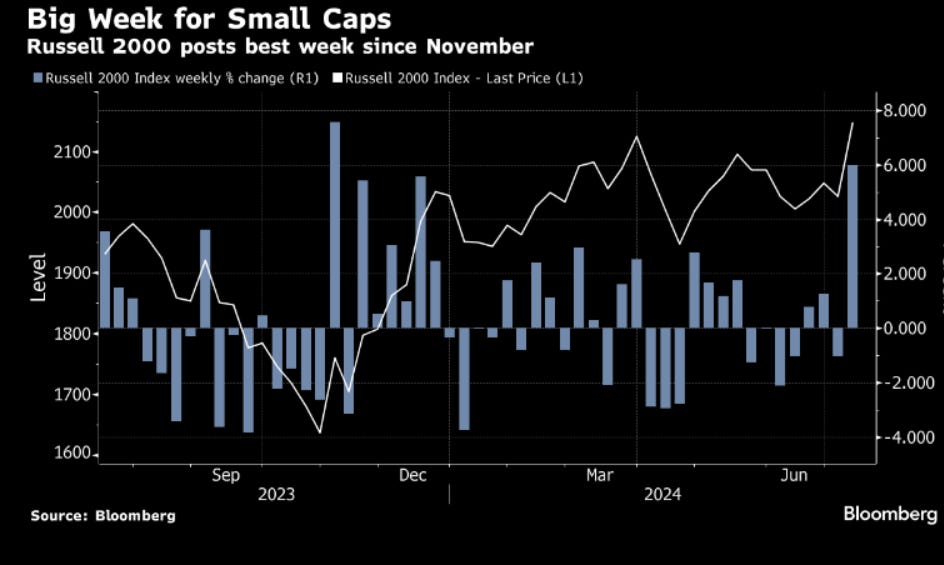

US interest rate cuts hope sent small caps stocks (Russell 2000) rising 6% this past week, the best weekly performance since November 2023. Global stocks rallied, global bond yields declined, USD declined (Yen jumped 1.8%!), VIX remained steady at 12.5%, and the Treasury Bond Volatility Index dropped 12 points to 86.8 for the week.

Based on Bloomberg’s macro strategist Cameron Crise, “Since the inception of the Russell 2000 in late 1978, there had been just eight days in which that index rallied 2% or more on a day when the SPX fell.” Also, “Thursday’s session marked a day of position liquidation, whether we are talking about long tech/short small-caps or positions in the yen.”

While investors ponder whether this is a one-time reaction, it is good to bear in mind the relative underperformances of the Russell 2000 (on average -3.5% on a 1-year trailing basis) vs. the S&P 500 since the end of 2016 where large caps have outperformed small caps by a high amplitude (see One Chart below).

Elsewhere, China’s economic picture remains weak with June CPI declining 0.1% m/m and rising +0.2% y/y. However, the recent Chinese government restriction of short-selling stocks plus the US interest rate outlook sent the Hang Seng Index up 2.8% for the week (note the top 8 companies in the Hang Seng Index are Mainland Chinese companies).

This coming week, we will monitor the US June retail sales on Tuesday and the June housing starts on Wednesday, the ECB interest rate meeting on Thursday, the UK June CPI on Wednesday, the Third Plenum in China from July 15 to 18, and China’s June retail sales, industrial production, Q2 real GDP, and fixed asset investment (YTD) on Monday.

Early market reactions to the unexpected Trump shooting this past Saturday will be seen in Asian currencies (e.g. Australian dollar and Japanese Yen) and the Mexican Peso. Expect more volatility to come.

“Inflation is no longer the only risk we face,” said EY Chief Economist Gregory Daco. “Maintaining excessively restrictive monetary policy when the labor market appears to be fully back in balance could lead to an undesired weakening of employment growth and the economy.”

Credit investors are, so far, brushing off the risks, instead piling into a deluge of debt sales to capture some of the highest yields in a decade. Risk premiums in both the high-yield and investment-grade bond markets are tight as demand continues to outpace supply. Money managers are also moving up the risk curve, according to data compiled by LSEG Lipper, pulling money from blue chip funds and adding $675.5 million to junk ones.

The amount of investors believe the global stock market will rise in the next 12 months is at record of 76% of those surveyed, with the top 3 stocks to invest to be Nvidia, Microsoft, and Apple.

In his memo, Howard [Marks] calls this a false dichotomy. He writes that value and growth “should never have been viewed as mutually exclusive to begin with.” And he argues that successful investing ultimately comes down to superior judgment.

When you’re playing a point, it is the most important thing in the world.

But when it’s behind you, it’s behind you... This mindset is really crucial, because it frees you to fully commit to the next point… and the next one after that… with intensity, clarity and focus…

The best in the world are not the best because they win every point... It’s because they know they’ll lose... again and again… and have learned how to deal with it.

You accept it. Cry it out if you need to... then force a smile.

You move on. Be relentless. Adapt and grow.

Work harder. Work smarter. Remember: work smarter. ~ Robert Federer, (he holds several ATP records and is considered to be one of the greatest tennis players of all time.)

One Chart You Should Not Miss: S&P 500 (Large Caps) vs. Russell 2000 (Small Caps) Relative Returns (1-Year Trailing)

The following chart by Datatrek Research shows the 1-year trailing relative returns between the S&P 500 (large caps) and Russell 2000 (small caps) from 2009 to the present.

When the blue line is above/below 0 (the X-axis), the S&P 500 has out/underperformed the Russell 2000 by the percentage shown on the Y-axis.

Source: Datatrek

According to Datatrek, while the Russell on average beat the S&P 500 by 0.9% from 2009 to 2016, since then the S&P 500 outperformed the Russell by an average of 3.5%, with the past year's outperformance close to 20%.

While the Russell had a banner year compared to the S&P 500, since 2017, for almost 3/4 of the time, the S&P 500 outperformed the Russell 2000.

The data shows that small caps, despite the US's generally good economic growth, no longer consistently outperform the large caps after 2016. Small caps tend to outperform when the economy is coming out of a recession and high-yield bond spreads are declining (like in 2021), which is not the current economic case. One reason is the investor’s focus on the mega large caps tech companies, fuelled by the AI theme.

The recent outperformance of the Russell 2000 may represent a relative value trade and a catch-up to the large caps as the Fed is viewed as more certain to cut interest rates in September.

However, note that the S&P 500 has 30% in the information technology sector, while the Russell has only 15%, with the weight more equally spread between the industrials, financials, health care, and info tech sectors. If market performance is broadening to sectors other than infotech, that is another reason why Russell may continue to outperform the S&P 500 in this coming year.

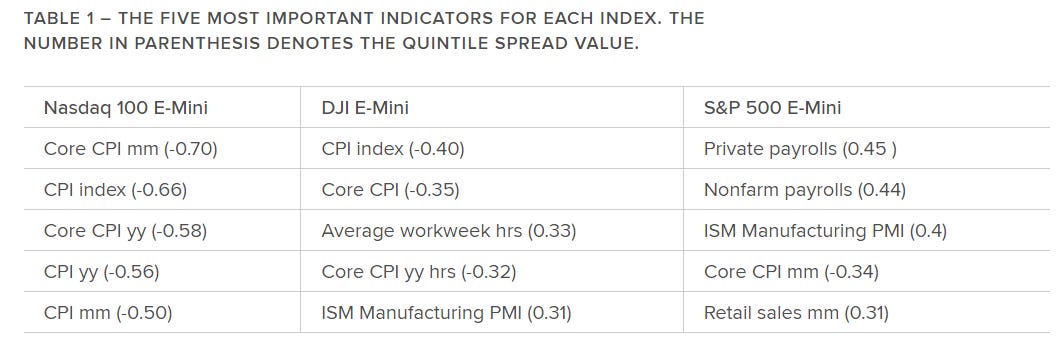

One Term to Know: Economic Surprises

Economic surprises are economic data releases that differ significantly from the consensus forecast and can move different types of market indices differently —equity, bond, currency, etc.

LSEG studied various economic surprises and their impact on three liquid equity indices - Nasdaq 100, Dow Jones Industrial Average, and S&P 500 based on the index futures contract prices from 2009 to 2022.

They tracked the changes in contract prices in a 5-minute window after the economic data release and put them into 5 quintiles. The quintile spread of the different indicators is the difference of the index futures contract price change between quintile 5 (most positive surprises) minus quintile 1 (largest negative surprises).

A negative quintile spread means the economic indicator surprise affects the equity index in the opposite direction.

The 5 most important indicators for each index are plotted below, showing how economic data surprises affect equity indices differently.

For example, non-farm payrolls affect the S&P 500 but less so on Nasdaq and Dow Jones while Core CPI affect all three indices importantly.

Using an AI Assistant as a business coach can help you with your business strategy and advice 24/7 without the need to incur the cost of a business consultant. This is done by writing a mega-prompt, which is a longer-than-usual prompt specifying role, context, explicit instructions, and examples of desired outputs.

For example, one can write a mega-prompt like this and then fine-tune the results by modifying the mega-prompt using roles and directives. Iterate until the results become helpful and relevant to your business needs, goals, or projects.

You are a seasoned business coach that provides startups, entrepreneurs, and corporate leaders with advice and feedback based on their real business needs. You combine real-world business experience with coaching skills like active listening. You ask questions that enable your clients to reflect and apply critical thinking. I will ask you questions, and you will provide actionable answers and direction with succinctness while formatting your responses with clear headings and bullet points. You will first ask me to write a paragraph about my business so that you understand my business context before giving advice. ~ 100daysAI

…instead of hiring teams of specialists across every function, small business owners can purchase AI capabilities that will become the “right-hand person” abstracting away the headaches of business operations and enabling the business to do what it does best—build and nurture meaningful customer relations and experiences through their products and services. ~

Tech giants and beyond are set to spend over $1tn on AI capex in coming years, with so far little to show for it. So, will this large spend ever pay off? MIT’s Daron Acemoglu and GS’ Jim Covello are skeptical, with Acemoglu seeing only limited US economic upside from AI over the next decade and Covello arguing that the technology isn’t designed to solve the complex problems that would justify the costs, which may not decline as many expect.

Thank you so much Marianne for the mention. 🙏🏼🙏🏼🙏🏼