Weekly Good Reads: 5-1-1

On Google AI, Credit Tightening, Bank's Asset-Liability Mismatch, and Japanese Eating Etiquette

Welcome to another issue of 5-1-1. Each week, I will include 3 links to relevant economic and investment news, 1 link to finance, and 1 to wellness pursuit based on what I read (5 links). I will also include 1 important chart and 1 investment term to know.

The week began with the Quarterly U.S. Fed Senior Loan Opinion Survey, showing tighter bank credit standards and weaker demand from businesses and households. Credit tightening applies to all business sizes for commercial and industrial loans, an important bellwether for economic growth, and household debt products such as mortgages and home equity lines.

One good news is U.S. April Consumer Price Inflation finally dipped below 5% yoy (at 4.9%) for the first time in 2 years while the Fed’s focused indicator CPI Core Services ex-housing dropped to 5.1% yoy, the weakest since July.

With the U.S. government running out of money in a few weeks if the debt ceiling (currently at $31.4 trillion) is not raised, the IMF and JPMorgan CEO warned of potentially catastrophic outcomes like a deep recession and a blow to national security. Hedge fund investor Stanley Druckenmiller predicted a U.S. hard landing based on current economic trends. Fund managers use put options to hedge for large stock price declines as equity volatility is still low.

The week was a big AI week with Google announcing many AI features being integrated into Gmail (e.g., Help Me Write), Google Searches (conversational answers and follow-up requests using fresh data), Google Maps (Immersive View for Routes), all Google Workspace products (such as doc and sheet plus a collaborative tool called “Duet AI.”) The most anticipated news was Google’s AI chatbot Bard will be publicly available and powered by its newest large language model: PaLM 2 (fluency in over 100 languages and codes plus text-to-image, math, logic, and reasoning). Google is not on defense vs. Microsoft/Open AI anymore.

Watch out for the G-7 summit announcement next week in Japan’s Hiroshima. Can Japan play peace-brokering?

Economy and Investments:

1. Banks Tighten Credit Terms, See Loan Demand Drop, Fed Survey Shows (Reuters)

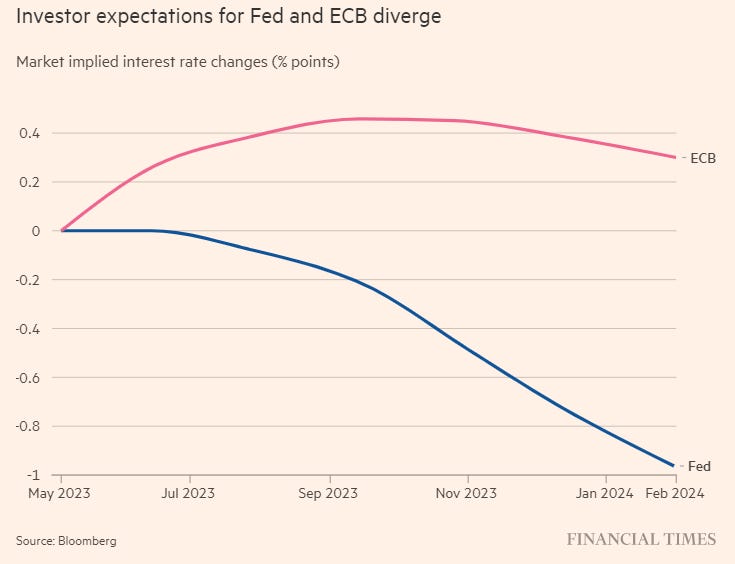

2. Investors Bet on ‘Great Divergence’ between Federal Reserve and ECB (Financial Times)

3. AI Frenzy Accounts for All of S&P500 Gain in 2023, SocGen Says (Yahoo Finance)

Finance/Wealth:

Keynote speech for the 37th USC Marshall Center for Investment Studies Annual Meeting (Stan Druckenmiller) - Druckenmiller urged the graduates to address the U.S. fiscal gap issue, which will derail future investment and growth.

Wellness:

Japanese Dining Etiquette 101 (Just One Cookbook)

Bonus: 6 Quick Things You Can Do to Improve Your Health - Tips Picked up from Life in Japan (kakikata.space)

One Chart You Should Not Miss: Interest Rates Expectation Divergence

“We are in for a great divergence in monetary policy on both sides of the Atlantic which is something quite new,” said Christian Kopf, head of fixed income at Union Investment, as reported in FT. This happens as the Fed signals a pause in rate hikes while the European Central Bank may raise interest rates 1 to 2 more times due to “significant upside risks to inflation remaining.”

One Term to Know: Banks’ Asset-Liability Mismatch

With the collapse of the Silicon Valley Bank in early March, the fragility of a bank business model has been in focus. Banks take short-term (on-demand) deposits (liabilities) to fund longer-term loans they lend out or longer-dated bonds they invest (assets). When interest rate rises, customers either demand higher interest rates or flee to money market funds or Treasury bonds while the banks’ loan/bond value declines—the mismatch between assets and liabilities is getting larger, especially when banks cannot keep their bank deposit rates low anymore.

Please do not hesitate to get in touch if any questions!