Weekly Good Reads: 5-1-1

Higher for Longer, China Stimulus, Options, Naval Ravikant's Ideas

Welcome to a new issue of Weekly Good Reads 5-1-1, and a warm welcome to my new subscribers! Thank you so much for supporting my work 🙏. Please let me know any feedback or questions by commenting below.

I am Marianne O, an investment professional and author of The Learner’s Mind about investing, economy, and wellness ideas. For this Weekly, I include 5 links to relevant economic and investment news, finance, and wellness/idea pursuit based on what I read. I also include 1 important chart and 1 investment term to know. All the Weeklies are here. You can easily subscribe to my newsletter by clicking below.

Market and Data Comments

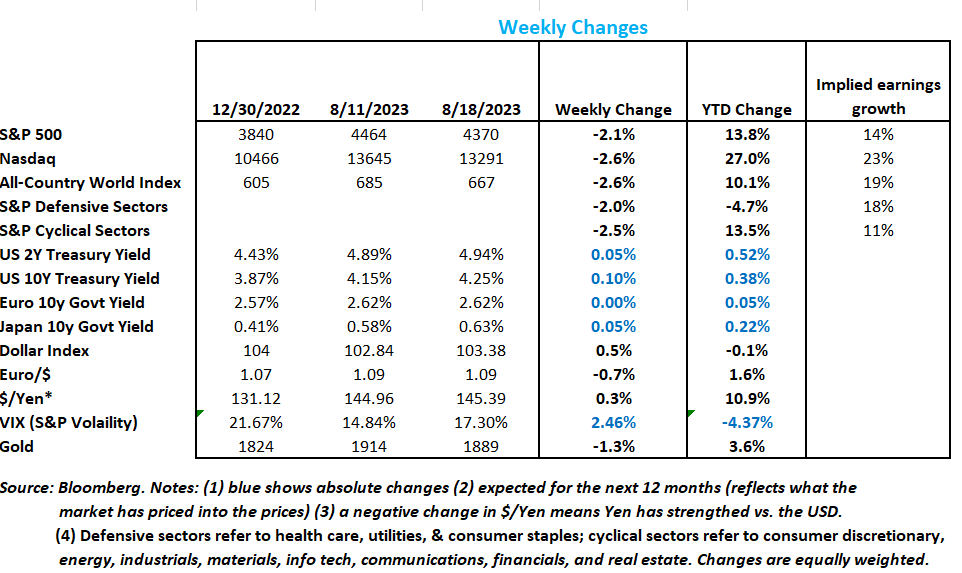

This market could not stop talking about rising bond yield and China risks this week. With the US 10y government bond yield near 4.3%, the highest since 2008, bonds have become great contenders compared to stocks (see article #1 below). The yield on 10-year US Treasury Inflation-Protected Securities (TIPs) hit 2% on Friday, its highest level since 2009. Major stock indices declined between 2.1% to 2.6% this week.

Higher than expected US Treasury issuance, Fitch downgrade of US credit rating, and change in Japanese Yield Curve Control policy, as well as stronger US data (e.g. retail sales, housing starts, and industrial production), led bond yield to rise higher.

The market will focus on Fed Chairman Powell Jackson Hole economic outlook speech next Friday and expect higher-for-longer rates in developed markets.

China, on the other hand, is under the weight of a debt crunch (from property woes), and deflation and is deleveraging. The news includes Evergrande (property developer) filing for bankruptcy in the US, continued housing price decline, and real estate investment falling 8.5% yoy (Jan to July). Downside surprises in retail sales, fixed asset investment, and industrial production confirm the slowing economy, property crisis, and subdued consumption. JP Morgan estimated about 13% of China’s total trust assets may see rising default risks, given their exposure to property and local government debt.

To counter waning consumer confidence and credit demand, the central bank of China not only lowered interest rates but also intervened in the FX market and asked state-owned banks to carry out about $2bn of intervention to support the Yuan and asked fund managers to stop net selling stocks.

See

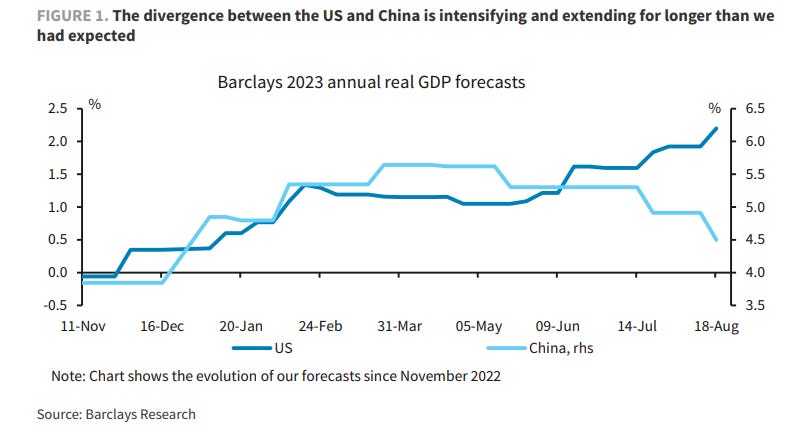

’s interesting take on China. Can China’s government, enterprises, and citizens keep their spirits and confidence up and avoid Japanification?From the chart above, economists like Barclays have been ratcheting up the GDP growth expectation for the US but down for China.

Next week, we will watch for the BRICS summit on Tuesday, European PMI data on Thursday, and key speeches by Fed Powell on US economic outlook and ECB President Lagarde on “Structural Shifts in the Global Economy” at Jackson Hole on Friday.

On Wednesday, he [Argentina Presidential Candidate Javier Milei, the leading candidate in the primary election] flashed his zeal for unleashing the powers of free markets on the ailing country in a two-hour interview in Buenos Aires. He vowed to slash government spending, shutter the central bank, replace the beleaguered peso with the US dollar, and restore credibility to the famously unstable economy.

~ Bloomberg

Economy and Investments (Links):

1. Investors Are Leaving Stocks for the Allure of Risk-Free Payouts in Bond (Bloomberg, or click here).

2. The 4 Most Important Things to Know About the China Slowdown (Macrohive research)

3. Will China's Economy Follow Japan's Path? (Ginger River Review)

So far no, but will China problems become a bigger threat to the global economy, especially if opaqueness leads to more social confusion and economic uncertainty. Good space to watch.

Finance/Wealth (Link):

What an Amusement Park Can Teach Us About Central Banks (Tim Harford)

Wellness/Idea (Link):

Naval Ravikant on How to Build Wealth (Smart Friends Podcast by Eric Jorgenson)

This is one of my favourite quotes from Naval. It is a basic concept of mathematics that has geometric consequences on many aspects of our lives:

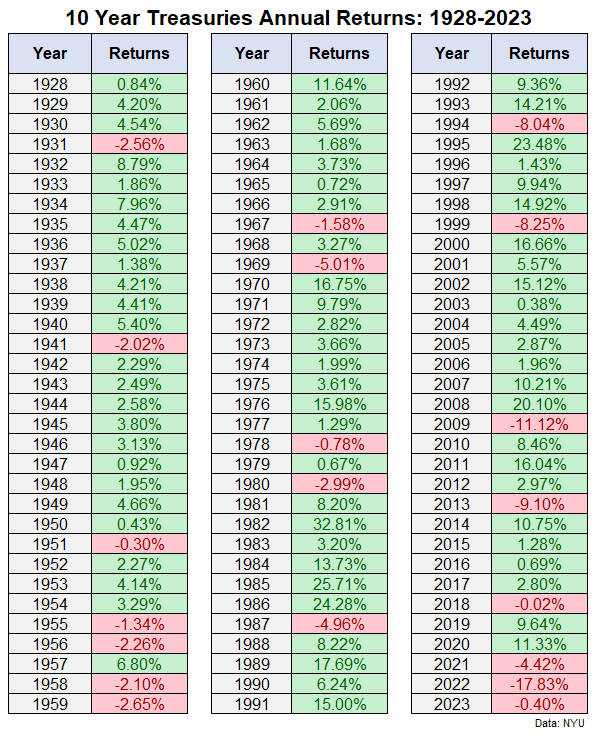

One Chart You Should Not Miss: Bond Returns (Since 1928)

Since the 1950’s the US Treasuries have not declined three years in a row. The 2022 bond decline was exceptional, due to inflationary pressures, impact of war, the Fed playing interest rate catch-up, etc. The year is not over; in the 2H of 2023, the economy can surprise on the weaker side and bonds rally.

One Term to Know: Out-of-the-Money Options

An option is a financial derivative and a contract that gives the buyer the right to buy or sell a financial product at an agreed-upon price (called strike price) for a specific period of time. The buyer has the right, but not the obligation, to exercise the option. Options are based on the value of underlying securities such as stocks, indexes, and exchange-traded funds (ETFs). Options are used for hedging, income, or speculation. The price you pay for an option is called a premium. Before the option expires, you can trade the option.

Out of the money (OTM) describes an option contract that has no intrinsic value but has extrinsic value (cost/premium of the option itself).

A call option is OTM if the underlying market price is trading below the strike price of a call option. So if the underlying stock appreciates in price before the call option expires, the premium or value of the call option increases.

A put option is OTM if the underlying market is above the put’s strike price. If the underlying stock price declines before the put option expires, the premium or value of the put option increases.

OTM options cost less than in-the-money or at-the-money options because they have no intrinsic value. Read more using the link in the section title.

Please do not hesitate to get in touch if any questions! If you like this weekly, please share or subscribe to my newsletter.