Weekly Good Reads: 5-1-1

US Downside Risks, German Elections, Berkshire's Annual Shareholder's Letter, Aha! Moments, Bessent's 3-3-3 Rule, Anthropic's Economic Index

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work. I appreciate you for reading and taking the time!

Sharing the quote of the week:

One who looks around him is intelligent, one who looks within him is wise.

~ Matshona Dhliwayo

You will find some useful sections below.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Please try our firm’s solution R4A. It’s free!

Market and Data Comments

This past week, the MSCI All-Country World Index dropped 1.1% led by the US (S&P -1.7%, Nasdaq, -2.5%, Russell 2000, -3.7%) while the Euro Stoxx 600 was slightly up and Hang Seng surged by 3.8%. Both US stock and bond volatility indices jumped while the US 10-year government bond yield declined 4bp to 4.43%.

The voices of worry are sounding louder. First, the January FOMC minutes showed the Fed plans to pause interest rate moves for a while reflecting the need to see lower inflation coupled with tariff and policy uncertainties.

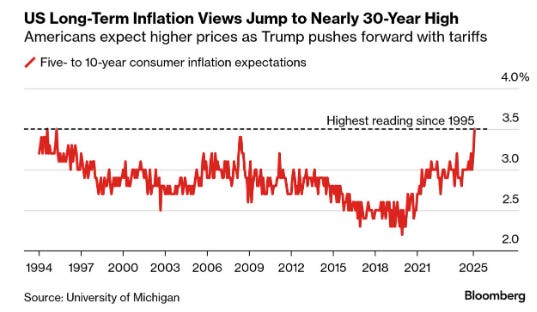

Second, long-term inflation expectations of US consumers rose to an annual rate of 3.5%, the highest reading since 1995 as fear of tariffs set in.

Third, the preliminary February S&P Global PMI dropped to 50.4, the slowest pace since September 2023 (see top chart), with the service PMI contracting for the first time in 2 years (49.7, 52.9 prior) albeit manufacturing PMI improved to 51.6 (51.2 prior).

Fourth, with mortgage rates back at 7% and housing prices continuing to rise, January existing home sales fell 4.9% on an annualized rate while housing starts dropped 9.8%.

Fifth, DOGE’s actions will lead to about 300,000 federal job cuts, but as Torsten Slok said, the multiplier effect (2 contractor jobs get cut per one federal job loss) will lead to one million job losses. (Also see Econ/Invest #3 Trump’s Executive Orders Explained—those related to the Federal Government (21 of them) outnumber those of other categories.

Rising downside risks may point to a slower 2H of the economy with real GDP below 2% compared to the Q1 estimate at 2.3% by the Atlanta Fed (as of today.) Interestingly, the US consumer staples sector has topped the performance chart YTD and was up 6.2% (see the sector change table below.)

In addition, US households, mutual funds, pension funds, and foreign investors now own 54% of their financial assets in equities, widening the gap against debt (at 18%) to the highest level since 2000 (see chart below). Any weakening in consumer sentiment and the labour market will have an outsized impact on the stock market, especially when the US bond yield is unlikely to rally much below 4.5% at this point, providing little support to the equity market.

Other news of note is the German elections on Sunday (February 23), the results (Friedrich Merz, leader of the opposition conservative Christian Democratic Union (CDU)) will likely be the next chancellor) will determine the future role of Germany in NATO and the EU and how the German economy will be revived after years of industrial decline. In the face of the US patronage withdrawing from the region as Trump’s administration looks to reset its relationship with Russia, there will likely be a faster buildup of defence spending in Europe, with Denmark already raising its defence spending to over 3% of GDP.

This coming week, we will monitor the German Federal election on Sunday, the US Q4 real GDP on Thursday, the January personal spending and core PCE price index on Friday, the Euro Area January inflation on Monday, Germany's Q4 real GDP and February IFO business climate on Tuesday, and Tokyo February CPI on Thursday. Nvidia will report on Wednesday its Q4 earnings (the company to watch these days!)

Economy and Investments (Links):

Berkshire Hathaway Annual Letter to Shareholders, 2025 (Berkshire Hathaway)

While Berkshire Hathaway did better in 2024 vs. 2023 and operating earnings rose 27% last year, 53% of its 189 operating companies reported a decline in their earnings in 2024, and with Berkshire being a net seller of shares, Buffett’s views towards the economy can be described as soft. In a few words, Buffett has also offered advice to the US government—pay taxes, save more, spend prudently, and maintain a stable currency.

In a very minor way, Berkshire shareholders have participated in the American miracle by foregoing dividends, thereby electing to reinvest rather than consume. Originally, this reinvestment was tiny, almost meaningless, but over time, it mushroomed, reflecting the mixture of a sustained culture of savings, combined with the magic of long-term compounding.

Berkshire’s activities now impact all corners of our country. And we are not finished. Companies die for many reasons but, unlike the fate of humans, old age itself is not lethal. Berkshire today is far more youthful than it was in 1965.

However, as Charlie and I have always acknowledged, Berkshire would not have achieved its results in any locale except America whereas America would have been every bit the success it has been if Berkshire had never existed….

So thank you, Uncle Sam. Someday your nieces and nephews at Berkshire hope to send you even larger payments than we did in 2024. Spend it wisely. Take care of the many who, for no fault of their own, get the short straws in life. They deserve better. And never forget that we need you to maintain a stable currency and that result requires both wisdom and vigilance on your part.

Taking Advantage of Superbooms (The Big Picture - Interview with Jeff Hirsch, Why Big Federal Spending Plus Inflation - “Superbooms”)

Jeff Hirsch: Think about AI and all the related tech about where we were in like ‘92 to 95 with Windows 95. Early internet days. My view is that we’re kind of at that period of time in this technological boom.

I remember the other part of the superboom equation that I added to it on top of war and inflation and peace was the culturally enabling paradigm shifting technology. Which AI and all of its related ancillary items, that we spoke about are part of. And I think we’re at that, you know, early, mid-nineties timeframe.

Barry Ritholtz: So to wrap up, if you’re a long term investor and you are constructive about both the economy and the market. You should be looking at sectors like defense and energy and technology. And you should not be surprised that the current bull market might have a whole lot further to run.

Trump’s Executive Orders Explained (Bloomberg or via Archive)

Finance/Wealth (Link):

In Search of the Best S&P 500 ETF (Barron’s)

+ Three Simple Rules From The Man Who Inspired Warren Buffett (Finimize)

“The intelligent investor is a realist who sells to optimists and buys from pessimists.”

“The investor’s chief problem – and even his worst enemy – is likely to be himself. In the end, how your investments behave is much less important than how you behave.”

“No matter how careful you are, the one risk no investor can ever eliminate is the risk of being wrong.”

~ Benjamin Graham

Wellness/Idea (Link):

The Brain Science of Elusive ‘Aha! Moments (Scientific American or via Archive)

…when you are stuck, take a break and expose yourself to a variety of environments and people to increase the chance you will encounter a triggering stimulus. Perhaps the most important scientific lesson about insight, though, is that it is as fragile as it is beneficial. The aha! moment brings new ideas and perspectives, lifts mood, increases tolerance for risk, and enhances the ability to discern truth from fiction. But anxiety and sleep deprivation can squash these precious gifts.

Modern society’s unrelenting demand for productivity and speed often denies insight the time and opportunity to work wonders at its own pace. Even so, we need to remember the value and power of insights and the conditions that spark them. As Morgan’s galactic epiphany shows, when it comes to aha! moments, the sky is the limit.

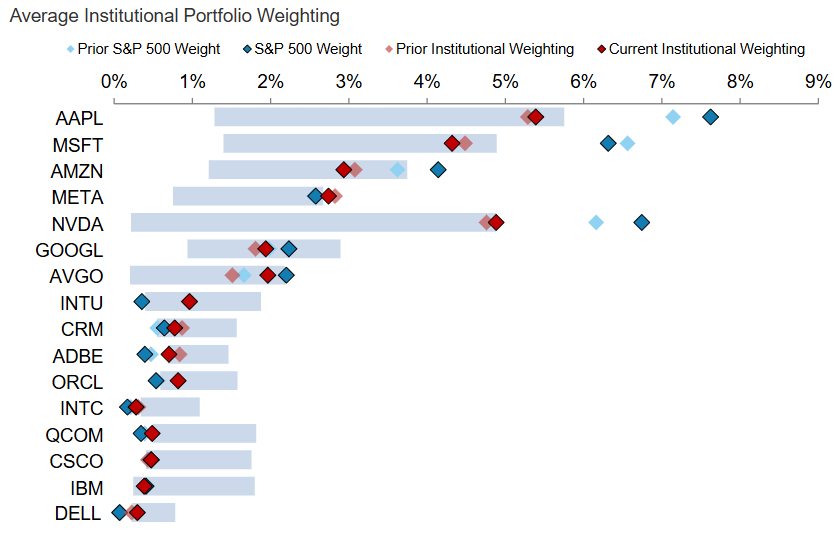

One Chart You Should Not Miss: Institutional Ownership of Mega-Tech Stocks - Most Underowned in 16 Years

One Term to Know: Scott Bessent’s 3-3-3 Plan

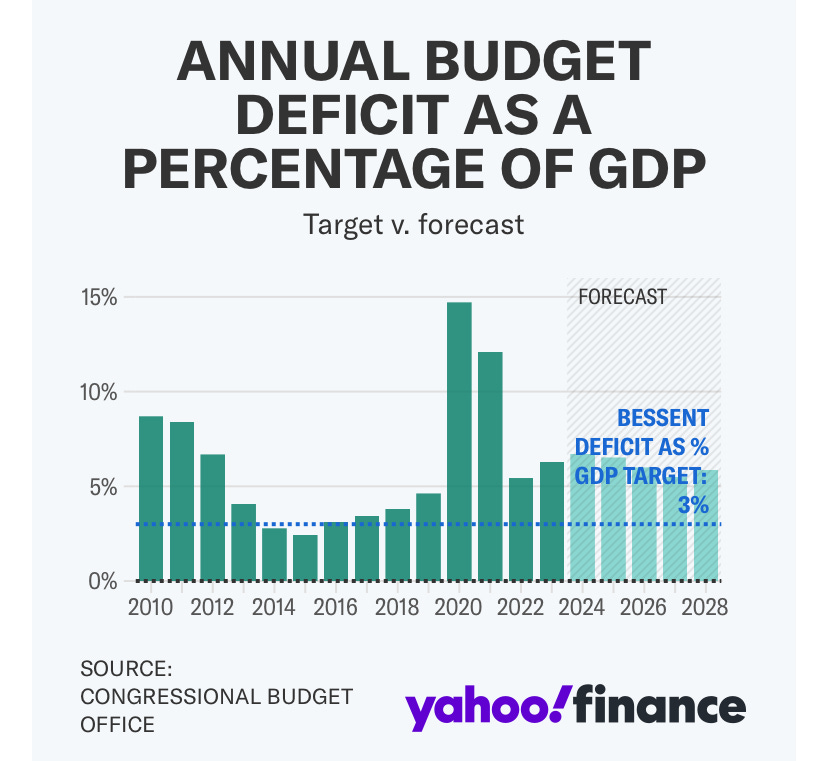

US Treasury Secretary Scott Bessent has famously set his ambitious 3-3-3 plan: real GDP would average 3% p.a., annual budget deficits would drop to 3% of GDP, and domestic oil production would rise by 3 million barrels per day (versus currently 13.5 million b/day) by 2028.

Reality check: the US Congressional Budget Office projects real GDP at 1.9% of GDP for the next decade. The fiscal deficit was at $1.8 trillion in 2024, to reduce that to 3%, federal spending has to be cut by $1 trillion.

Bessent has already said he will extend the 2017 tax cuts, adding $4 trillion to the national debt. If DOGE aims to cut $1 trillion from government spending but without touching defence, social security, and Medicare, CAP estimates this would require a massive import tax of 20% across the board and 60% on China (an equivalent of a $2,200 tax increase for a typical family), big axes to anti-poverty programs such as Medicaid, cuts to veterans’ benefits and pensions, and reduction in debt service, while lowering taxes for the wealthy.

Oil producers currently are more focused on returning capital to shareholders than boosting production. The idea behind higher oil production is to bring down oil prices, consumer inflation, and long-term interest rates, thus encouraging more economic growth and a lower budget deficit as a percentage of GDP.

[🌻] Things I Learn About AI/Productivity:

Reuters at Davos 2025 - Watch now the AI Outlook 2025 (Reuters)

The Founder of Workhuman highlighted there are three phrases of AI use by companies: (1) experimentation (2) getting real work done but heavily supervised by humans and later unsupervised (3) having an AI-first draft mindset, i.e., the first draft of every worker’s output is generated by AI. For example, if you are a marketer, make your first draft AI-generated. Then the human element kicks in to make it production-ready. He has seen that 20% of the first draft of codes in software engineering has been done by AI. Imagine when 30% of the first drafts are done by AI in multiple sectors and industries, human productivity can be vastly increased.

The Anthropic Economic Index studies how AI is used in the workplace by examining millions of real conversations in the Claude AI platform.

The findings: AI is primarily used for augmentation (57% of tasks, assisting human work) rather than full automation (43% of tasks) and is used the most in tech fields such as software engineering and technical writing (37.2%) followed by arts and media (10.3%).

AI mainly affects mid-to-high-wage occupations and is currently enhancing existing jobs more than replacing them outright. Only 4% of the jobs use AI for at least 75% of its tasks.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

Conversational AI usage might be very different from API usage - so Anthropic's index might be biases towards more writing oriented tasks.

On job market, I have been surprised by the reported strength vs felt softness. I am wondering with the 1m job loss related to DOGE and the natural time lag before resettlement into workforces, inflation will come down faster and rate cut will be put back on the table (assuming no DOGE's disruption at Fed)