Weekly Good Reads: 5-1-1

Tariffs, Consumer Sentiments (Divergence), Managing Uncertainty, 60/40 Not Working, AI Agent (Free)

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work. I appreciate you for reading and taking the time!

Sharing the quote of the week:

It is never too late to be what you might have been.

~ George Elliot

You will find some useful sections below.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

👉 Interested in creating customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Please try our firm’s solution R4A. It’s free!

Market and Data Comments

Watching tariff announcements is a major sport in the market, with Trump imposing 25% tariffs on Mexico and Canada and then delaying that for a month and levying 10% on all Chinese imports (including revocation of the “de minimis” rule from goods from China).

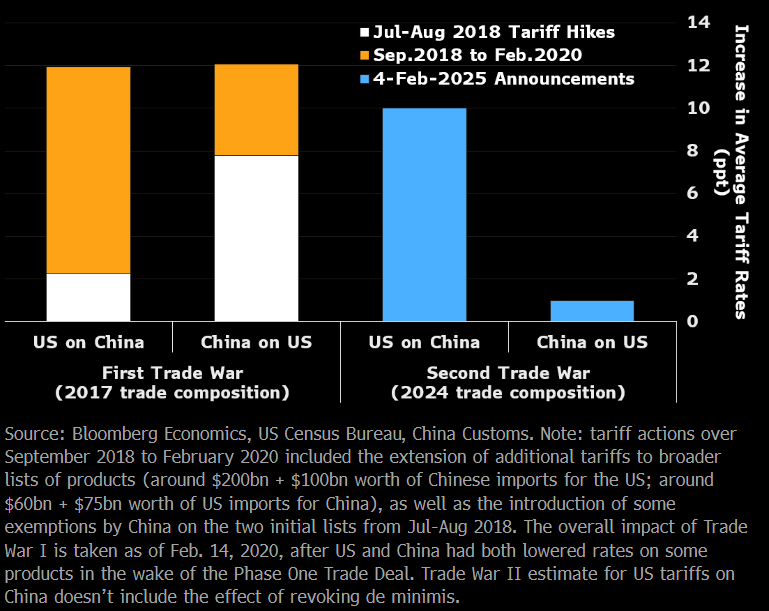

According to Bloomberg, during the first Trade War between the US and China in 2018, US average tariffs on Chinese imports and China’s average tariffs on US goods were up 12% from the pre-trade war level by mid-February 2020.

So far in 2025, while the US hit China with a 10% tariff, China retaliates on only about 9% of its US imports with a 10 to 15% tariff, thus raising the average tariff rate to US goods by 1% (see chart above), so a much milder response. But, the 10% on China is likely the beginning, and retaliation will ensue. The next will be Europe.

Turning back to the macro data, US nonfarm payrolls rose 143k in January (lower than 175k expected), the previous two months’ data were revised up by 111k, while the unemployment rate was down to 4%. 3mma non-farm payrolls (at 237k) is now the highest since early 2023 (Barclays). The labour market and the consumers are still doing well, but less fiscal tailwind, tariff uncertainty, and lower immigration may slow the economy down.

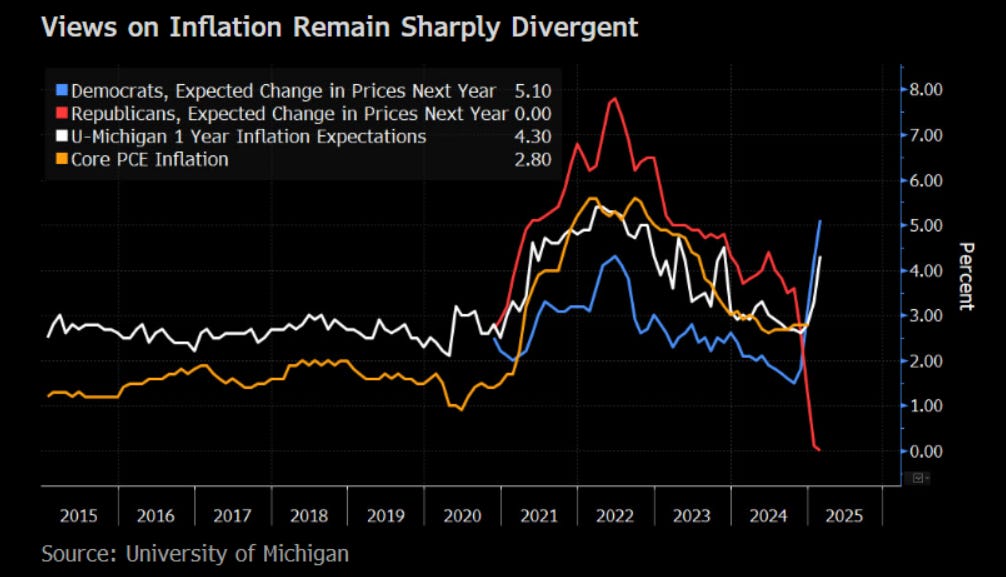

Consumer sentiment deteriorated further in early February to 67.8 (71.1 prior) while next one-year inflation expectations surged to 4.3% (vs. 3.3% prior and the 2.3-3% range pre-Pandemic). However, the views of the Republicans vs. Democrats diverge dramatically: Republicans expect inflation to slow drastically ahead, while Democrats expect looming tariffs to push up inflation.

Overall this week, global stock markets were slightly weaker, except for Hong Kong (+4.5%), while the dollar retreated 0.3% but copper surged 7.2% and gold rose 2.2%.

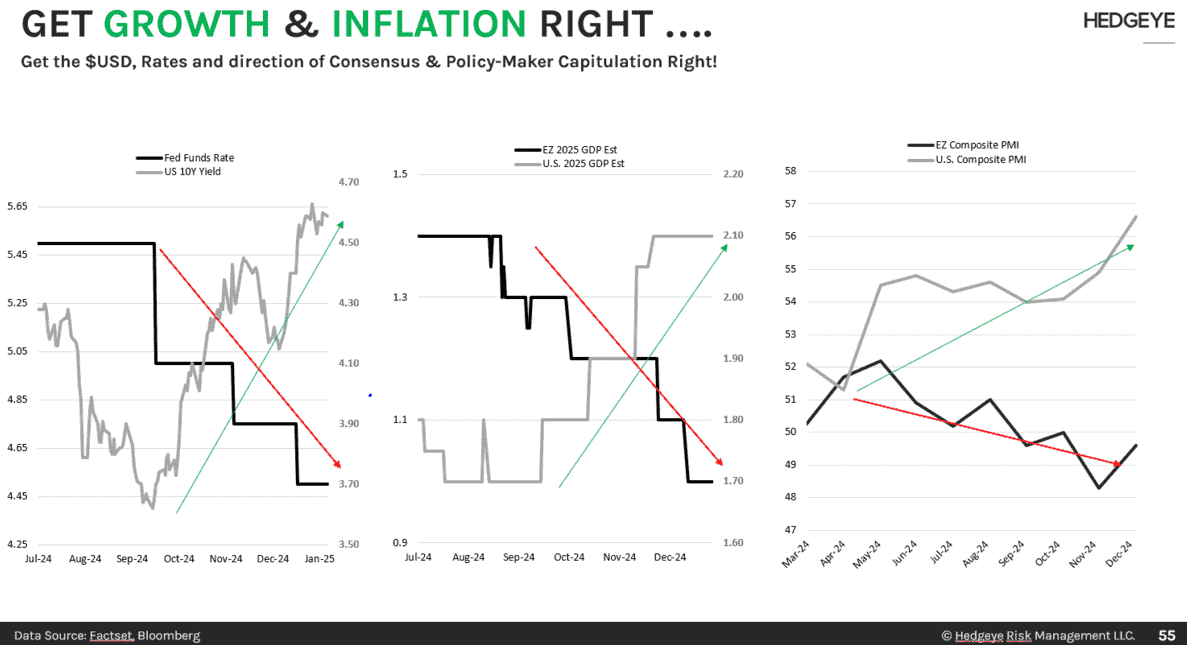

Hedgeye highlighted below the 3 key macro megatrends to watch currently—the Fed Funds rate vs. the US 10-year yield, the US and European relative real GDP growth rate in 2025, and the composite PMIs of the US vs. Europe.

These relative movements have major implications on the direction of the US dollar, how consensus thinks about rate direction, how much the Fed action lags behind the market expectations, and how fast the Fed may catch up.

I agree with one of Hedgeye’s recommendations that when long-term rates are uncertain, exposure to rate-sensitive sectors is not advisable (e.g. fixed income or highly leveraged companies). Stay focused on growth-oriented equities including US Tech, financials, and energy/commodities, but be broadly diversified especially if inflation rises but growth slows.

Elsewhere, the Bank of England cut rates by 25bp to 4.5% this past week, with the market expecting 4 more 25bp cuts for 2025 (Barclays).

This coming week we will monitor US January CPI on Wednesday, PPI on Thursday, retail sales, and industrial production on Friday, the Euro Area Q4 real GDP on Friday, and China’s January CPI and PPI on Sunday.

Economy and Investments (Links):

Trump Is Testing Our Constitutional System. It’s Doing Fine (Bloomberg)

When these stressors are introduced into the system, the courts swing into action and block Trump’s executive overreach. Congress protests — or is supposed to — that the president can’t override federal laws that direct spending or establish agencies. If those things happen, the system equilibrates. Instead of degrading, the stress test shows the system works and what might need some fixing.

Bessent Says Trump is Focused on the 10-year Treasury Yield and Won’t Push the Fed to Cut Rates (CNBC)

“He wants lower rates. He is not calling for the Fed to lower rates,” Bessent said. Trump believes that “if we deregulate the economy, if we get this tax bill done, if we get energy down, then rates will take care of themselves and the dollar will take care of itself.”

Managing Uncertainty in the Trump Age (FT)

Over time businesses will need to re-evaluate their broader sourcing, production and distribution operations. Supply chain diversification, particularly away from China, has progressed since the pandemic. But now even those de-risking and “friendshoring” efforts are at risk. The administration has cottoned on to “China Plus One” strategies of shifting some production to third countries, such as Mexico and Vietnam, to export into America. Still, assessing new sourcing routes and logistics hubs and finding new markets can provide operational flexibility. This can be costly, but it hedges against rising geopolitical tensions. By forcing businesses to look at alternative fast-growing markets it can also be fruitful.

Finance/Wealth (Link):

Be Water, My Friend (Anthony Isola)

Martial arts and personal finance do have a lot in common.

The best techniques are the simple ones executed right ~ Bruce Lee. This quote illustrates the most significant reason index funds outperform stock picking over the long term: Simple almost always beats complex in personal finance.

Wellness/Idea (Link):

Profile | Chinese Ballet Dancer and Social Media Star Sun Jia Shows What Goes On Behind The Curtain (South China Morning Post)

When people think about ballet dancers, they only see what they see on stage – pretty and elegant,” she says. “But we are human beings, and I thought it’d be interesting to show what we do every day and show people another side to our profession.

One Chart You Should Not Miss: View of Americans, Democrats, and Republicans of the Economy

In late October [of 2024}, 73% of Republicans said the economy was getting worse and 6% said it was getting better; now, 42% of Republicans say the economy is getting worse and 12% say it's getting better.

Democrats' views also have changed, though less dramatically: The share saying the economy is getting worse has risen from 16% in October to 30% now, while the share saying it's getting better has fallen from 42% to 32%.

Americans change their views of the economy as the President’s party is changing.

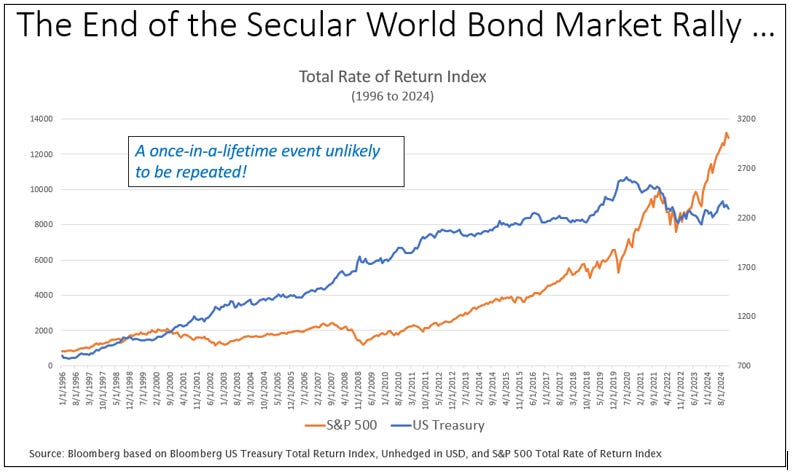

One Term to Know: 60/40 Portfolio (and Why It Is No Longer Good Enough)

The idea of a 60/40 Portfolio is to allocate 60% of a portfolio to stocks and 40% to bonds. The strategy works if bonds act as a hedge to stocks, i.e. when stocks are racing higher as the economy and market are doing well, the bond price may fall, but fall a lot less. But when the economy and market turn down, bonds are supposed to cushion the blow—a good way to balance risk and safety.

Since the early 1990s and thanks to a secular world bond market rally (see chart below), the correlation between stocks and bond prices has been neutral or negative. Note bond yield had been coming down from the range of 8 to 16% in the 1980s.

But since September 2022, this relationship no longer holds, and correlations have stayed more positive; that means when stocks prices fall, bond prices also fall and bond yield rises (the prime example was when both stocks and bonds fell the same amount in 2022 as interest rate environment shifted (Fed raising rates).

That means bonds no longer offer a sure-win diversification benefit to stocks, especially in light of the uncertain tariff policies and rising debt burden in the US which promote inflation.

Alex Shahidi published a paper in 2012 that outlined the shortcomings of the 60/40 mix and said this mix is almost exactly as risky as a portfolio composed entirely of equities, using historical returns since 1926. His alternative portfolio of 30% Treasury bonds, 30% Treasury inflation-protected securities (TIPS), 20% equities, and 20% commodities was shown to yield almost the same returns over time but with far less volatility, in other words, a higher Sharpe Ratio.

{kind=link}

[🌻] Things I Learn About AI/Productivity:

Replace OpenAI $200 Deep Research with this Agent (Paul Couvert)

This will be my first test of an AI Agent, built with Replit, the online coding environment. The first step is to get Paul’s template (free), replicate it on Replit, and follow his instructions step by step. I look forward to having my own AI Agent to do deep research on the web using iteration and refining and to get a complete report—all for free.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

Was wondering what you thought about the tariffs (as a Canuck I’m obviously paying attention). Very helpful and eloquent as always!