Weekly Good Reads: 5-1-1

US exceptionalism, Central Bank Decisions, AI and Power Consumption, Fakes, GDP vs. GDI, and Selling Volatility

Welcome to Weekly Good Reads 5-1-1 by Marianne O, a 25-year investment practitioner and the author of

on investing, economy, and wellness in an intuitive voice. All the Weeklies are here, and here is the index of charts and terms. You can easily subscribe to my newsletter by clicking below.Please also check out my conversations with Female Fund Managers and Investors - new this year!

Thank you so much for your support🙏.

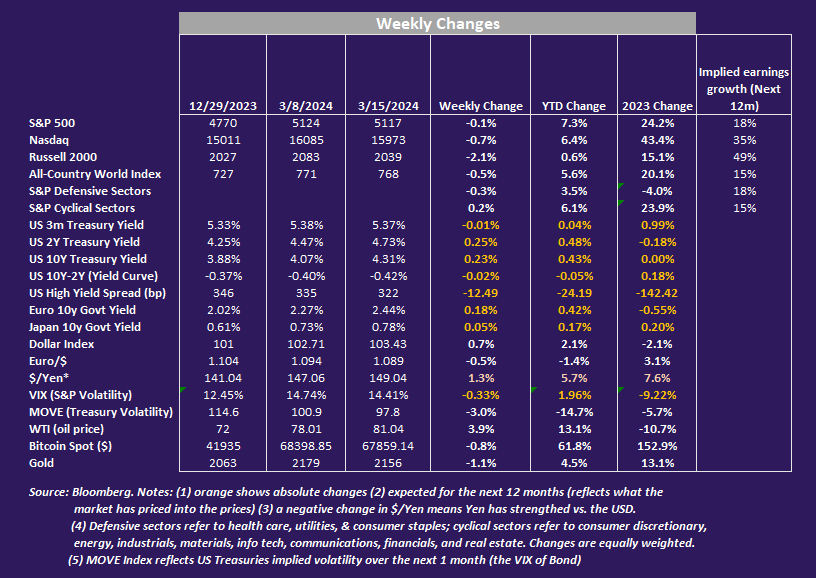

Market and Data Comments

With the US February headline CPI and core CPI (yoy) coming in at 3.2% and 3.8% and PPI at 1.6% and 2% respectively (chart above), disinflation in the US is largely intact albeit both CPI and PPI month-on-month increases were hotter than expected (see chart above). Based on these February data, economists have reasonably estimated that the core PCE on a 12-month basis will decline to 2.5% yoy by June from 2.8% (February, estimated), very close to the Fed’s “projection”.

Disinflation is happening across the West, not just in the US, and as Barclays pointed out, this has happened without net job losses so far. The US macro resilience (and growing above potential) has been the top macro story in the past year, leading global GDP to be around 3.1% in 2024 (flatline from the expected 3.1% in 2023) according to the IMF.

On the other hand, US February retail sales growth was lower than expected (0.6% vs 0.8% expected and revising lower for January and December).

The full employment as % of the working-age population is rolling over, and sharp decelerations were coincident with recessions (chart below, worth monitoring). As the US GDP is 70% consumption, wage growth needs to sustain full employment/jobs, which sustains spending.

US households now face unprecedented non-mortgage interest payments (the same level as mortgage payments measured in annual rate).

Retail sales, full employment status, and wage growth trends could point to slower periods of consumption growth ahead. The latest GDPNow data from the Atlanta Fed was 2.3% as of March 14, 2024, slowing down from over 4% (end of January estimate).

The week ended with the world stock markets softening a touch (worse in US small caps) but interest rates moving up about 20bp across the curve in the West, fortunately with lower bond volatility. Energy stocks had a good run fuelled by a 3.9% jump in WTI price. Also increasingly, energy companies cited AI (especially data centres) as pumping up energy demand (see Econ/Invest. #2 below).

We await interest rate decisions from the US, Japan, and the UK central banks next week. The biggest news is possibly from Japan, which received intense pressure to end its negative interest rates and yield curve control policies in next week’s meeting. The market expects no change in the Fed’s rate decision although some expect the Fed may update its dot plot to reflect two cuts (median projection) rather than 3 cuts and the UK will push the interest rate cut to later in the year.

This coming week, we will monitor US FOMC rate decision, the Fed’s press conference, and new Fed dot plot projections on Wednesday and February existing home sales on Thursday, the Euro Area Composite PMI for March (preliminary) on Thursday, Bank of England rate decision on Thursday, Bank of Japan’s rate decision on Tuesday, and China’s Jan-Feb fixed investment, retail sales, and industrial production on Monday.

Economy and Investments (Links):

Corporate Bond Rush Is Breaking Down a Maturity Wall That Everyone Feared (Bloomberg or via Archive)

How AI Is Sparking a Change in Power (Barron’s or via Archive)

America’s Extraordinary Economy Keeps Defying the Pessimists (The Economist or via Archive)

To understand this, consider the reasons for the economy’s extraordinary performance. A key plank was generous pandemic stimulus, which at 26% of GDP was more than double the rich-world average. This largesse fuelled inflation but also ensured fast growth: consumers have yet to spend all the cash they received in “stimmy” cheques...Strong demand has been met by growing supply. America has 4% more workers than it did at the end of 2019, thanks in part to rising workforce participation, but mainly owing to higher immigration…Other long-standing strengths have made America enviably placed to cope with geopolitical tumult. Its vast internal market encourages innovation and means it depends less on foreign trade than smaller rich economies do…

The trouble is that each of the ingredients for growth can no longer be relied upon. It may be tempting for politicians to extrapolate from America’s recent success and juice the economy with further stimulus. But that is becoming unsustainable. Official forecasts show that America will this year spend more on debt interest than national defence. More borrowing risks building up financial perils in the future.~The Economist

Finance/Wealth (Link):

How to Research an ETF? (Investing Channel.com)

+ What The Birth of the Spreadsheet Teaches Us about Generative AI (Tim Harford)

Wellness/Idea (Link)

It’s Harder Than Ever to Identify a Manipulated Photo. Here’s Where to Start (National Geographic)

If you see a photograph that’s giving you pause, Farid suggests searching to see if any research or articles have been published about it, or if other outlets like Snopes or FactCheck.org have investigated it. If you’re only seeing the image on community forums like Reddit, 4chan, and Twitter “you should probably just ignore it.”

“Many so-called ‘fakes’ aren’t necessarily fabrications, they’re just old images misleadingly passed off as new,” Looft says. “Reverse image search is an easy way to tell whether an image already exists. There are many options but TinEye has a great reverse search, and some other tools for those looking to go a little deeper. ~ National Grographic

+ 🎧 How to Run a Profitable One-person Internet Business Using AI (Every)

One Chart You Should Not Miss: (Gross Domestic Product) GDP versus Gross Domestic Income (GDI) - Widening spread

GDP tallies all spending (final expenditures) by businesses, consumers, overseas companies and the government by conducting a broad survey of retailers, car dealers, manufacturers and others.

GDI estimates all incomes represented by wages and salaries, corporate profits, interest and dividends, and rents.

In theory, GDI and GDP should match, but they can differ because not only are they measured by different surveys with differences in sampling errors, but final expenditures data (that go into GDP) are considered more timely while in measuring GDI, the early income estimates of quarterly corporate profits, bonuses, stock options, and other incomes may reflect income earned during the year, but recorded later only in the quarter when it is paid.

Morgan Stanley explained why the US economy keeps pumping and how GDI is dropping below GDP (GDI/GDP ratio now at 0.98).

We think the better than expected economic activity can be explained by the ongoing fiscal support. The budget deficit remains around 6-7 percent of GDP which is unusual in an economy that is operating close to full employment. Funding for the IRA and Chips Act programs, in particular, are driving not only spending dollars but also hiring by private construction and manufacturing companies via the subsidies offered to incent such activities. While these programs are helping to keep the economy humming, they are also crowding out the private sector as they impact the cost of labor, materials and capital. One way to illustrate the increasingly ambiguous backdrop is the spread between Gross Domestic Income and Gross Domestic Product. Rarely do we see such a wide spread between two series that should be aligned conceptually, and historically such divergences do get reconciled. In short, the private economy will likely need to step up from a growth rate standpoint to match high expectations going forward. ~ Morgan Stanley

One Term To Know: Selling Volatility

You may know that a stock option gives you the right, but not the obligation, to buy or sell a stock at an agreed-upon price.

Option prices are influenced by numerous factors including the current stock price vs. the strike price, time to expiry, and the expected (implied) volatility of the stock.

Like buying house insurance, owners are compelled to buy insurance to protect themselves in case of disasters, and the probability of the actual losses is usually lower than the amount of hard assets owned on which the insurances are purchased.

In financial markets, as concerns about a stock or crisis loom, the volatility of a stock goes up, raising the option premium prices. In a period of calm, options traders can also benefit from “selling volatility” of highly volatile stocks whose options become relatively higher than average in the hope these options will lose value faster than comparable options with lower costs.

If no disaster happens, the seller of the options collects/pockets the premiums although if volatility spikes suddenly and sustainably, option sellers could experience deep losses.

Please do not hesitate to get in touch if you have any questions!

Check out also my Conversations with Female Investors and other changemakers.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

Thanks MO! I had no idea about the gap in GDI and GDP