Weekly Good Reads: 5-1-1

China's Bold Stimulus, Gold, Trading Rules, Ad Revenue, Bazooka, Emergency Preparedness

Welcome to Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

In this Weekly, I share insightful/essential readings, charts, and one term, incorporating some of my market observations and weekly change tables. I look beyond data and share something enlightening about life, health, technology, and the world around us 🌍!

Here’s the quote of the week:

Try to disprove your best loved ideas. ~ James Clear

Feedback is important to me, so if you like the Weekly, please “heart” it, comment, share it, or subscribe! Thank you so much for your support🙏.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

Market and Data Comments

The Fed easing has now clearly opened the door for China to ease. This past week, China has delivered a “Dragon Blitz” (quoting Barclays) though not an economic “Bazooka” (see One Term to Know below) as many economists and strategists commented. Announcements can be found in the table above (Morgan Stanley) and Econ/Invest. #1).

These actions, albeit with few details on the fiscal side, reflect a new decisive direction by the Chinese authorities (to stimulate demand to defend the 5% economic growth target), who had unfortunately regarded stimulus as “drinking poison to quench thirst”, to quote

’s post. The actions taken together and announced by the central bank, the securities commission, and the financial regulator plus the unscheduled Politburo meeting to call for more fiscal support were unprecedented.For asset prices, the Chinese CSI 300 Index (A-shares, up 16% this past week), Hang Seng Index (up 13%), and emerging market equities (up 6.1% proxied by the MSCI EM Equity Index) beat the rest of the major developed market indices, with glitches and delays in trading/order processing in the Shanghai stock exchange, representing a sea-change in investor sentiment toward Chinese stocks. Billionaire investor David Tepper is ‘“buying more of “everything” China-related after Beijing rolled out sweeping stimulus”’ per Bloomberg. Compared to the S&P 500 (+91%), China A-shares (+1% since the end of 2019) had much to catch up on (or perhaps much for investors to be excited about!)

Before changing their allocation to China, investors will monitor upcoming fiscal policy actions by China - for example, the execution of the expected CNY1tn each to stimulate consumption and help local governments tackle debt with the help of a CNY2tn issuance of sovereign bonds. This may raise GDP growth by 0.4% in 2025 per Barclays, but if China can execute a “Bazooka” of CNY10tn including more housing stabilization funds, fund transfer to local governments, and liquidity support to consumers and state banks, GDP growth in 2025 may be lifted by 1%.

In the US, mixed economic data this past week—job market confidence declined, softer-than-expected August core PCE (0.13% vs. 0.16% prior, and 2.1% 3-month annualized), and unexpected upward revisions to GDP data (+294 billion higher than expected in the 5 years ending 2023 with a higher-than-expected savings rate at 5.2% in Q2 2024) boosted market bets for another 50bp rate cut in November.

In Europe, with recent economic data (e.g. contractionary PMI) pointing to an outright contraction in Q3 2024 but a supportive inflation outlook (decline in energy prices YTD), the ECB will likely cut in October.

One market chart to note is that cross-asset momentum tracked by Societe Generale has jumped to the highest in more than one year. The 11 components, which include copper vs. gold, cyclical stocks vs. defensive, cryptocurrencies, high-yield bonds, etc., are flashing hot, with this bullish level seen at only about 5% of the time based on data since 2011 (read more in Econ/Invest. #3).

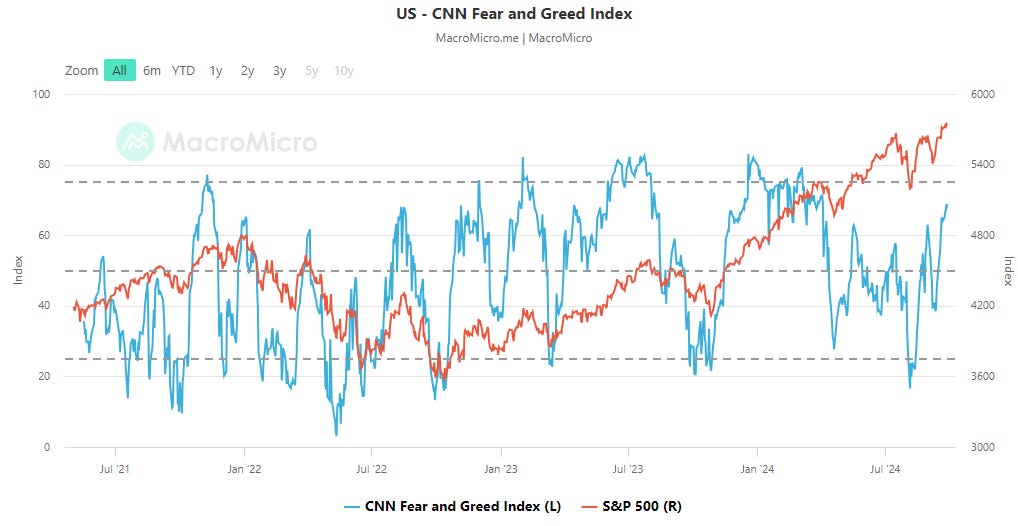

Global central banks’ easing, led by the 2 largest economies in the world, has re-fueled market optimism of a goldilocks economic scenario in the US and little risk of a global recession. The CNN Greed and Fear Index (latest at 68) rebounded to “Greed” from extreme pessimism in early August.

Nevertheless, for many fund managers, “cautious optimism” is needed, as when all asset classes move simultaneously, macro risks may be overlooked and leverage may jump, leading to complacency. With increasing market liquidity and optimism on China, cheaper assets such as emerging market equities and debt may attract a second look.

This coming week, we will monitor Fed Chairman Powell’s speech to a business economic conference on Monday, the US September manufacturing ISM on Tuesday, non-farm payrolls, unemployment rate and average hourly earnings on Friday, the Euro area September manufacturing PMI and inflation on Tuesday, August unemployment rate on Wednesday, the Bank of Japan rate decision on Tuesday, China’s September NBS and Caixin manufacturing indices on Monday.

Economy and Investments (Links):

At Last, China Pulls the Trigger On a Bold Stimulus Package (The Economist or via Archive)

These easing measures, even if confirmed, still fall short of the 2008 bazooka. That crisis-era package, often labelled the “4trn yuan” stimulus, ultimately amounted to 9.5trn yuan (or 27% of 2009 GDP) spread over 27 months, according to Christine Wong of the University of Melbourne. And some of the central government’s extra borrowing this year will merely offset fiscal tightening by cash-strapped local governments.

But even with these caveats, China’s stimulus this week comfortably exceeded expectations. It also sent a powerful signal. In a video conference on September 26th, the central bank’s leaders told branch officers to “go all out” in implementing the Politburo’s vision. Other officials may be getting a similar message. “As saving the economy and rescuing markets…become politically correct, we believe officials are likely to jump on the bandwagon to display their loyalty,” wrote Ting Lu of Nomura, a bank.

Why Gold Continues to Hit Record Highs (Investopedia)

+ Related: Unearthed: How Rate Cuts and Policy Decisions Will Impact Gold Markets (Gold Hub/ World Gold Council)

+ Related: The Next Nvidia (

)Wall Street's Risk Binge Expands to Even Unloved Assets After Global Policy Easing (Bloomberg or via Archive)

Finance/Wealth (Link):

Marty Zweig Trading Rules (The Big Picture)

Marty was famous for his call before the 1987 stock market crash in the show Wall Street Week (6:30m on YouTube). The trading rules I most resonant with are (but all of them are gems):

The trend is your friend; don’t fight the tape hard return

If you buy for a reason and that reason is discounted or is no longer valid then sell

The market is not efficient but is still tough to beat

If you can’t sleep at night reduce your positions or get out.

Wellness/Idea (Link):

As September is “Emergency Preparedness Month” (in California), here’s a reminder of a “Go Bag” to provide essential items during an emergency evacuation.

+ The Versatile Leader: How Learning to Adapt Makes CEOs Better (McKinsey)

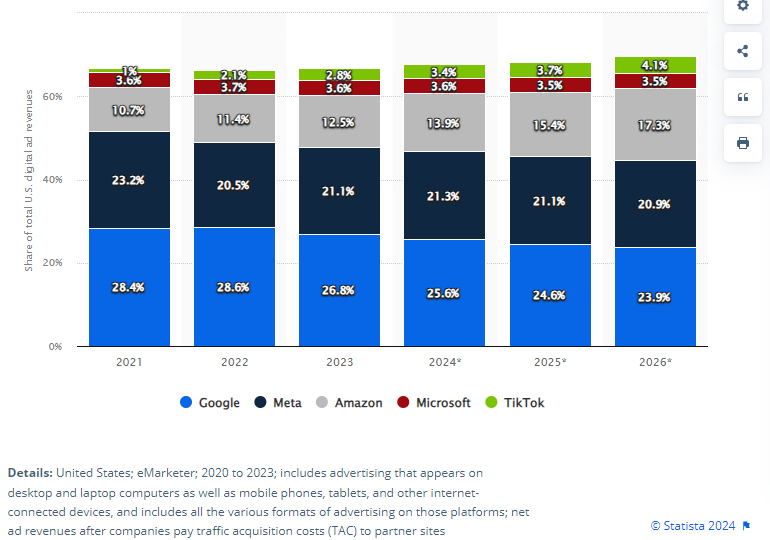

One Chart You Should Not Miss: Digital Ad Revenue

Google’s dominance in digital ad revenue (25.6% of total US digital advertising revenue as of 2024) dwarfed those of Microsoft and dominant search engine companies in China and Russia/EMEA (Statista), making Google susceptible to another loss from the second antitrust lawsuit from the US Department of Justice.

One Term to Know: Economic “Bazooka”

The term bazooka originally refers to a shoulder-type rocket launcher adopted by the U.S. Army in WWII, the first infantry weapon that could reliably attack tanks and fortified positions at a short range.

This is now adopted to mean “You blast everything you have at a problem with as big a weapon as you have.”

This was seen in the US (banks and mortgage markets support and the unprecedented quantitative easing) and China (economic stimulus) during the 2008-2009 global recession and ECB Draghi’s famous speech that the ECB would do “whatever it takes” to save the Euro in 2012 and his unprecedented monetary policy easing in 2016.

The recent macroeconomic policy moves by China are not “qualified as a bazooka” but rather a big jolt to the demand-lack economy and a bold step in the right direction. The problem of China is structural and deep-rooted and not cyclical, so consistency and execution by the authorities are key to a sustainable economic rebound.

[🌻] Things I Learn About AI/Productivity:

It was never credible that OpenAI was protected from the financial interests of the investors pouring billions of dollars into it. Restructuring the company to make those interests explicit may sharpen their profit motives, but it will at least bring some semblance of oversight and structure to what is arguably the world’s most important startup, sitting on its most powerful technology.

Shruti Mishra below made a great point. Canva is my most used productivity and graphics tool but I am scratching the surface with its capability. I especially like the video recording (based on OBS) and how easy it is to turn a presentation into a video.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

I always look forward to these but I think this was my favourite!