Weekly Good Reads: 5-1-1

All my favourite Substack reads

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

In the spirit of Thanksgiving, this Weekly will look different. It will have all my latest favourite reads under each topic ALL from Substack writers. I am grateful for their generous insights, which are deliciously good, and you will probably click on each link.

To my readers, thanks again for following my work🤞!

Sharing the quote of the week:

The real voyage of discovery consists not in seeking new landscapes, but in having new eyes. ~ Marcel Proust (Courtesy of )

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

Here’s my latest investing post in case you have missed it:

👉 One more: here’s an invitation to try our firm’s digital investment software for creating customized portfolios tailored just for your goals and risk profile (for free):

Market and Data Comments

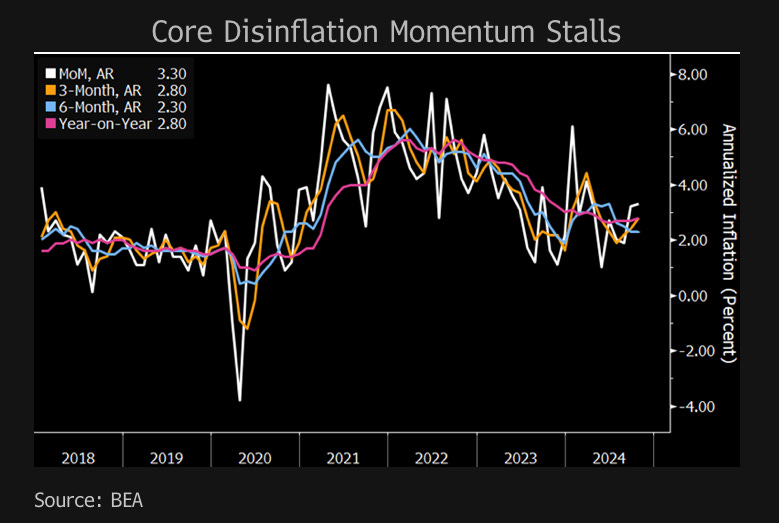

With the US Thanksgiving holiday week, market trading has been relatively light. The notable data release includes the US October core PCE price index, the Fed’s preferred inflation gauge, which rose 0.27% m/m (in line with expectations) but ticked up to 2.8% y/y thanks to rising financial costs, after staying at 2.7% y/y for the past 3 months. On a 3m annualized basis, core PCE is 2.8%, a pickup from 2.4% in September. The headline PCE rose 0.2% m/m or 2.3% y/y (inline).

US October real personal spending, however, dropped to 0.1% m/m (0.5% m/m in September) while nominal personal spending rose 0.4% m/m (0.6% in September). Nominal income, however, has risen faster than expected at 0.6% m/m (0.3% in September). Fed will still likely cut interest rates in December as shown by the slowdown in real personal spending, but the future rate path is likely dependent on the inflationary impact of Trump’s tariff.

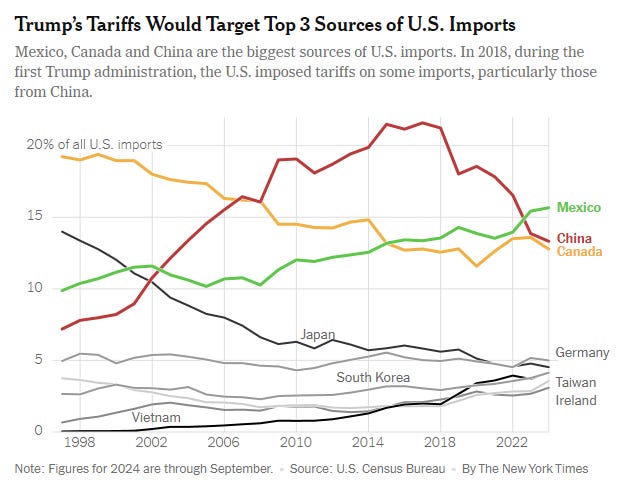

Trump threatens to impose 25% on all imports from Mexico and Canada and an extra 10% tariff on China on Day 1 of his Presidency to crack down on illegal immigrants and illicit drugs. The inflation level already looks stuck at a bit above 2%.

Euro area November inflation also ticker up to a four-month high to 2.3% y/y. Weak activity and impending U.S. tariffs should keep the ECB continue to ease.

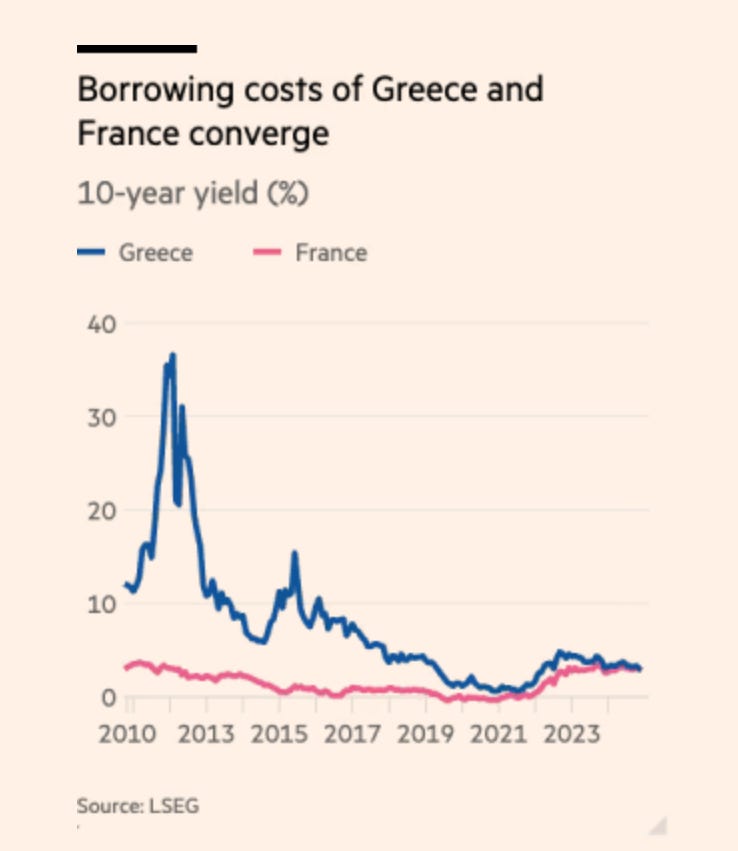

Meanwhile, French politics tension and the impasse in passing budget spending cuts caused the French 10-year government bond to rise above the Greek equivalent (Greece defaulted in 2011 and downgraded to an emerging market.)

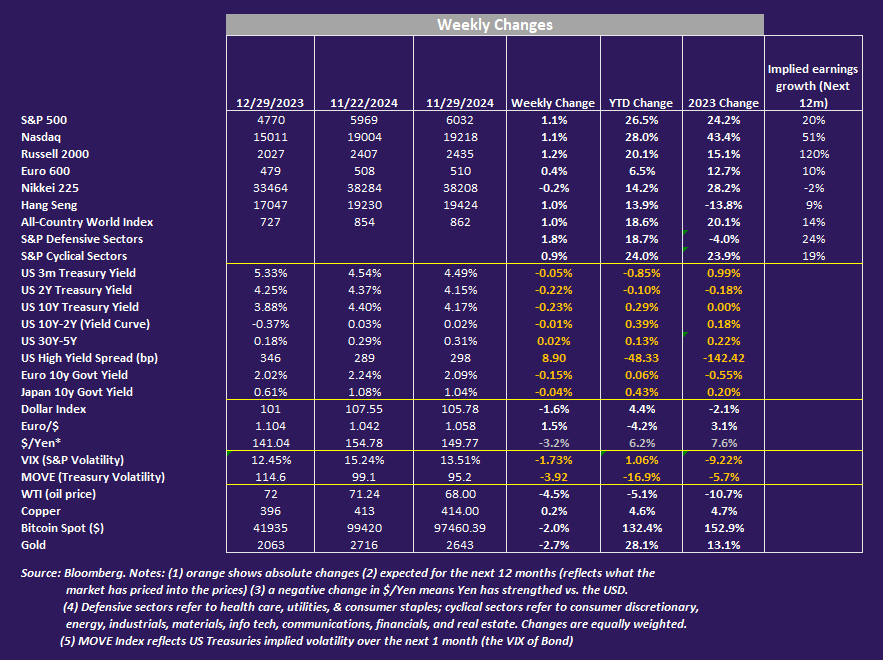

Japanese Yen rallied the most this week by over 3% to 149.77 after a higher-than expected Tokyo inflation, with the markets speculating the BOJ will raise rates in December and January.

One more note of interest—about the market this year—the upward trajectory of the US stocks (likely to be one of S&P 500 best years in history) appears to accentuate what Bank of America strategists call the “extreme disconnect” between investor bullishness on US assets and bearishness on the rest of the world (per Bloomberg).

In this coming week, we will monitor Fed Chairman Powell’s speech on Wednesday, the November ISM manufacturing index on Monday, the ISM services index on Wednesday, the November non-farm payrolls, average hourly earnings, and the unemployment rate on Friday, the Euro area November composite PMI on Wednesday, Germany October industrial production and the Q3 GDP estimate on Friday, and China’s November NBS manufacturing PMI on Saturday and the Caixin manufacturing PMI on Monday.

Economy and Investments (Links):

- at )

It’s also worth noting how little of this productivity boom can be ascribed purely to technological innovation—other high-income countries like the UK, EU, Japan, Australia, etc have the same access to the teleworking tools and artificial intelligence programs that the US has, but none of them have productivity booms on the scale of the US. It’s the combination of technological innovation and macroeconomic incentives for its rapid deployment which, when combined, brought American productivity growth back up.

- at )

Political identity is a particularly strong influence on how we interpret facts, which leads us to live in different realities. Neither reality is perfectly accurate. After all, just this month we flipped on the dime in the exact same fact environment. This, of course, compromises decision quality. The less accurately we model the objective facts, the worse our decisions will be.

- at )

High inflation was a problem, reaching levels not seen in decades and lasting longer than expected. Inflation is close to normal now, but the higher prices still loom large. In contrast, the labor market has been the success story of the recovery—getting millions back to work quickly, supporting large wage gains, especially among low-wage workers, and creating millions of new jobs. Those successes are crucial to countering the hardship of higher prices, but the successes did not loom as large in the public mind. Partly, it is psychology. Partly, it is storytelling.

Finance/Wealth (Link):

Earnings, Cash Flows and Free Cash Flows: A Primer, (

at )- )

I completely agree owning quality stocks, with due attention to starting valuation, will do very well for your portfolio in the long term. I have written about quality stocks here but will write a new post about my quality universe soon (stay tuned!)

- at )

Ryan verified his numbers about timing in the market!!

Wellness/Idea (Link):

- at )

- ) (hat tip to )

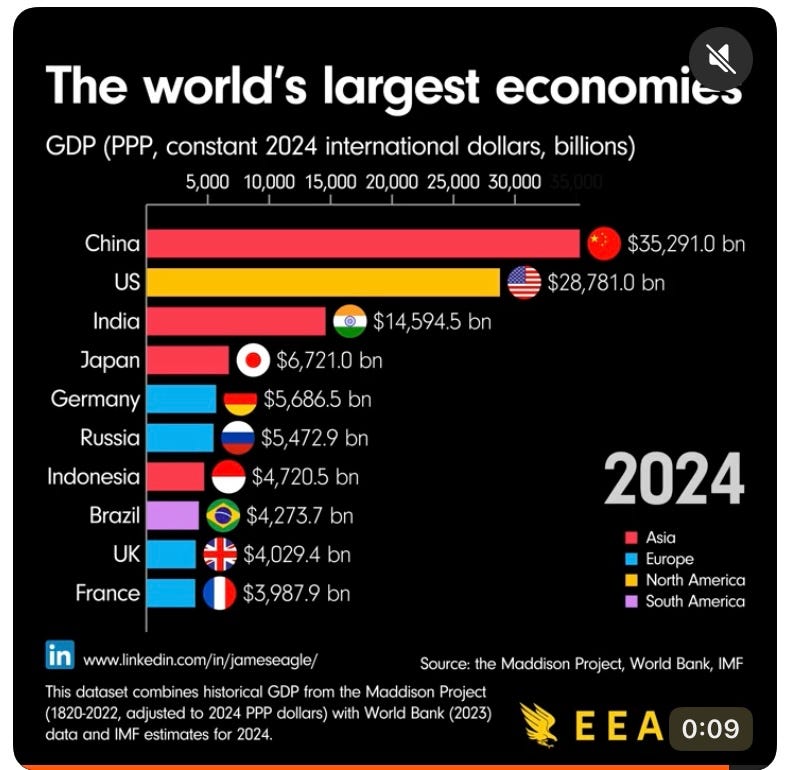

One Chart You Should Not Miss: The largest world economies using Purchasing Power Parity (PPP) - based on what money will buy in each country

By

1834:

2024 (Commonality? China and India’s dominant size!)

One Term to Know: Finese

I have a better grasp of the proper way to “finessing” after reading

’s pieces. There is a lot more under the hood. Part II is here.

[🌻] Things I Learn About AI/Productivity:

How to use NotebookLM for personalized knowledge synthesis (

at )The most comprehensive use cases of NotebookLM you will find!

Gradually, then Suddenly: Upon the Threshold (

at )

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

I’m flattered for the shout out!

Thanks a lot for the shoutout Marianne!