Weekly Good Reads: 5-1-1

Core PCE, Worsening Breadth, America's Best Decade, Trade Less, Mega Tech Ownership, T+1

Welcome to Weekly Good Reads 5-1-1 by Marianne O, a 25-year investment practitioner and the author of

on investing, economy, wellness, and something new I learn in AI/productivity. All the Weeklies are here, and here is the index of charts and terms. You can easily subscribe to my newsletter by clicking below.Please also check out my conversations with Female Fund Managers, Investors, and more - new this year!

Feedback is important to me, so if you like the Weekly, please “heart” it, comment or share it with your contacts. Thank you so much for your support🙏.

Market and Data Comments

The US Fed likely welcomed the cooling Core PCE inflation, personal income, and spending growth data in April, indicating the disinflation trend continues.

The Fed’s preferred gauge of inflation, core PCE inflation, rose 0.2% m-o-m (2.75% y-o-y vs 2.81% prior), personal income grew 0.3% m-o-m (0.5% prior), and personal spending growth cooled to 0.2% m-o-m (0.7% prior), showing signs of stretched households (also see Econ/Invest #2 for the KPMG American consumer survey for uncertain economic growth prospects.)

Q1 real GDP was revised downward to 1.3% (vs. 1.6% initial estimate), while the income-side measure, real GDI, declined from 3.6% in Q4 2023 to 1.5%, dragged down by much slower firms’ profit, reflecting the impact of the tight monetary policy.

The New York Fed believed high interest rates are working through the economy and expects PCE inflation to continue to ease in 2H to about 2.5% (now 2.7% y-o-y) by the end of 2024 (see Econ/Invest #1).

In the Eurozone, May inflation ticked higher to 2.6% y-o-y (2.4% prior) with core inflation rising to 2.9% (2.7% prior) driven by wage growth and services inflation. ECB has already prepared everyone for the June first rate cut to be announced this coming week, so this development means fewer rate cuts this year than originally thought.

This week, the BofA strategist showed the breadth of the US stock market is now the worst since March 2009 (see graph below; the decline shows an equal-weighted S&P 500 index underperforming the regular index). The BofA strategist expects “value stocks to outperform growth”.

Goldman analyzed the positions of hedge funds and mutual funds at the start of Q124 seeing their rotations into cyclicals including financials, energy, consumer discretionary, and industrials in addition to playing the utilities sector (the AI power theme).

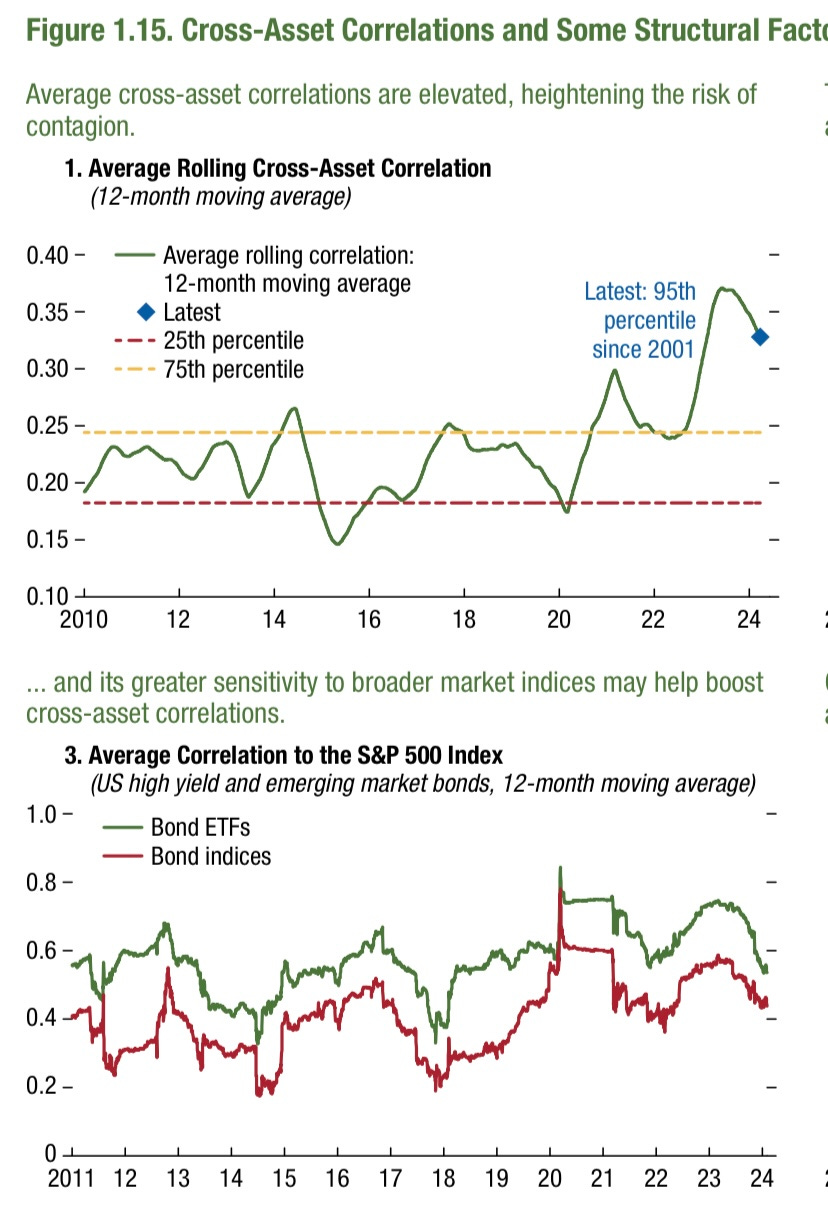

Also notice bonds have not been a reliable hedge to stock selloffs as the average correlation among major asset classes (including global government bonds, stocks, credit, oil and gold) has risen since 2H 2023 as shown by the chart from the IMF April 2024 Global Financial Stability Report, heightening the risk of contagion.

This coming week, we will monitor the US May non-farm payrolls, unemployment rate, and average hourly earnings this coming Friday, the ECB monetary policy meeting on Thursday, China’s May exports on Friday as well as election watch for 3 major Emerging countries including India, South Africa, and Mexico, and in June 6-9, the Europeans voting for the EU parliament.

Economy and Investments (Links):

High Interest Rates Are Working, Fed's Williams Says (Bloomberg or via Archive)

The Fed Cut Reflexivity Paradox (Apollo Daily Spark)

Financial conditions are significantly easier than when the Fed started raising interest rates in March 2022…Because fiscal policy is still a significant tailwind to the economy, and easy financial conditions have been offsetting Fed hikes…The more the Fed insists that the next move in interest rates is a cut, the more financial conditions will ease, making it more difficult for the Fed to cut.

Americans are more optimistic about their personal financial situations than the growth prospects of the U.S. economy over the next year, while exhibiting various degrees of enthusiasm, comfort and skepticism in the forces shaping the consumer experience…The report reviews these perspectives through the lens of compound volatility: the combination of near- term risks, such as geopolitical and technology-driven disruption, and longer-term structural changes to the U.S. economy, including the energy transition and sticky inflation.

Finance/Wealth (Link):

+ The lesson of Loki? Trade less (Tim Harford)

I’ve called this the Investor’s Tragedy. The more attention we pay to our investments, the more we trade, and the cleverer we try to be, the less we will have at the end of it all.

Wellness/Idea (Link)

America’s Best Decade, According to Data (Washington Post or via Archive)

But any political, racial or gender divides were dwarfed by what happened when we charted the data by generation. Age, more than anything, determines when you think America peaked.

One Chart You Should Not Miss: Institutional Ownership of Large-Cap Tech Stocks

Each quarter, Morgan Stanley tracks each tech stock’s average weight within the top 100 actively managed institutional portfolios relative to the stock’s weight in the S&P 500. As of Q1 2024, 4 mega-cap stocks are “under-owned” by institutional investors — Apple, Microsoft, Amazon and Nvidia despite a majority of these mega-cap tech outperforming the S&P 500 YTD.

One Term to Know: “T+1” Stock Settlement in the US

On May 28, 2024, the US switched to “T+1” for stock settlement. “T” stands for “trade” or “transaction” date. Before the computer age, stock settlement used to be “T+ 5” or longer. Between 1993 to 2017, it was “T+3”. Then it became T+2 until May 28 this year. Mexico and Canada have also moved to a “T+1” settlement.

The day when a security is bought or sold (traded) is the trade date. “T+1” means the security needs to be delivered and funds settled on the next business day (called the settlement date). For example, if a stock is sold on Monday, the client will receive her money on Tuesday (assuming no public holidays).

The SEC has said that “a shorter settlement window means lower odds that the buyer or seller might default before the transaction is completed. That translates to lower margin requirements for the broker and a lower risk that high volumes or volatility will force a broker to restrict trades.”

However, a T+1 settlement means US stocks will be out of step with the global currency market which settles in “T+2”. For foreigners, that means USD funds have to be lined up before doing a US stock transaction.

Some also fear there may be more settlement failure risks given the shorter time to settlement, or there will be too little time for the regulator to block fraudulent trends from happening.

[🌻] One Thing I Learn About AI:

San Francisco Federal Reserve held a lively event on “AI-Nomics: The Nexus of GenAI + Economy” with speakers including the President, the Fed Board of Governors, the Chief Innovation Officer at the SF Fed, and the Chief Economists at LinkedIn and ADP. Some highlights include:

Based on LinkedIn research:

(1) workers have added Gen AI skills on their LinkedIn profile 162x faster across many industries in the last year, especially in marketing and design jobs (adoption speed for GenAI is very fast)

(2) what are the economists’ skills Gen AI cannot replace: Communications (the #1 skill of any job), management, public speaking (all communications skills), labour, energy, and health economics (domain knowledge to explain analyses.)

Workers need to pivot to value-added skills e.g. technical digital skills changing quickly from MatLab to Python.)

On judgment and prediction: AI helps with prediction (they are statistical models and often a prisoner of past information), but AI cannot make good judgments.

The real new innovation of Gen AI is not in tech but in humans: how to get humans to innovate away from their standard practice and protocol that limit their productivity e.g. ADP rolling out tools to call centre operators educating them about all payroll structures in the world.

Productivity impact: research shows workers are saving up to 30 minutes a day with Gen AI; for software engineers: they are acquiring more skills faster, thus acquiring different jobs.

How to level up on Gen AI skills: engage in multi-disciplinary and multi-industry conversations, expand your industry horizon, and read books on AI applications in industries different from yours.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more!

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

Great thoughts and charts, thanks for sharing! As for inflation, it looks as if we’re get another leg down before considering the return of any inflationary spikes higher.

Thanks so much to @Andrew brons for restacking my post!!