Weekly Good Reads: 5-1-1

Core PCE Inflation, EPS Estimates, Public Debt, Trade Threats, Stablecoins, Luxury Brands, Human-AI Agents

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work! Please hit the 💛 button if you like it or share with others.

Sharing the quote of the week:

It's not whether you're right or wrong that's important, but how much money you make when you're right and how much you lose when you're wrong.

~ George Soros

Weekly archives | Investing | Ideas | Index of charts and terms | Conversations with Investment Managers

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Try R4A for free!

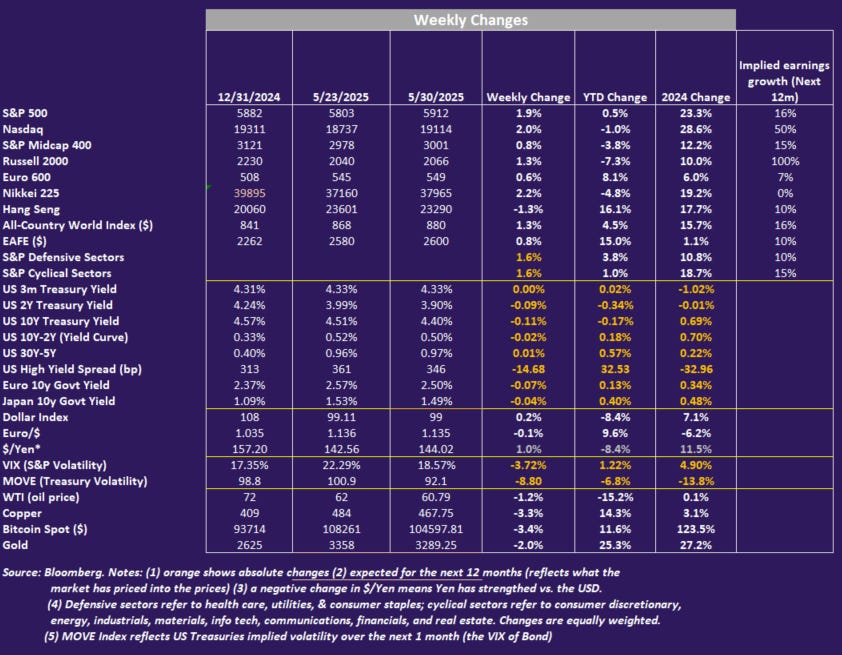

Market and Data Comment

This week’s macro and policy news has shown more optimism. First, the US Court of International Trade ruled Trump’s “reciprocal tariffs” unlawful (sectoral tariffs not affected). The market cheered, although economists largely expect the government’s appeal to win; even if that fails, there are other policy options for the government to implement these tariffs. Effective US tariff rates may end up around 15% (Bloomberg). China-US tariff talks appeared stalled with Chinese rare earth exports yet to flow to the US, and Trump doubled the tariffs on steel and aluminium imports from 25% to 50%.

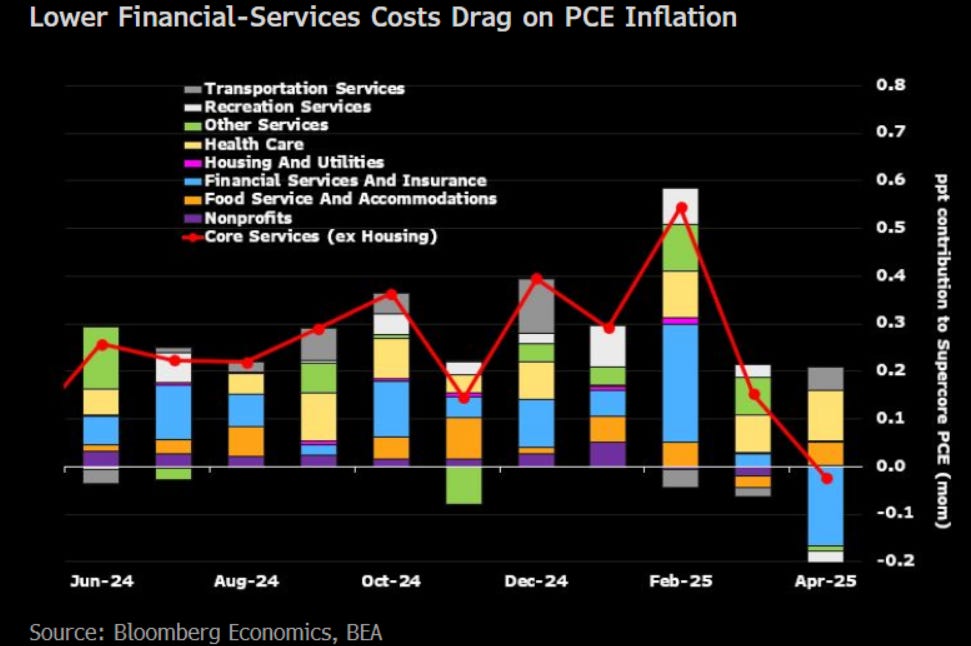

The April core PCE deflator rose 0.1% in April (2.5% y/y), dragged down by financial services costs but boosted by those sectors related to Chinese imports.

The Conference Board’s May consumer confidence rose to 98 (85.7 prior), given the relief from the temporary reduction in US-China tariffs. The University of Michigan’s May final consumer survey saw long-run inflation expectations falling to 4.2%, the first decline since December 2024. However, May’s final reading of consumer sentiment remains low at 52.2 (same as in April).

Another fundamental factor supporting the economy is the generally higher profit margins of US companies Post-Pandemic, especially for durable manufacturing, transportation and warehousing, wholesale trade, and retail trade, as reported by the Bureau of Economic Analysis. Firms are in a better position to absorb tariff costs, while any sharp rise in prices will likely hurt the firm’s revenue.

According to Factset, 78% of the S&P 500 companies beat EPS estimates in Q1, reporting on average 12.9% in earnings growth, the second straight quarter of double-digit earnings growth.

Nevertheless, analysts have also marked down Q2 EPS estimates at a greater pace than normal. Since the end of 2024, apart from the communication services, all other sectors have seen a decline in EPS growth estimates, with the energy sector having the most negative change at ~18% since December 2024 (full earnings insights here).

While the S&P 500 (+6.2%) and the Nasdaq (+9.6%) have seen the biggest rebound in May since November 2023, the market is watching the progress of the US Tax Bill, fiscal deficit trends, and tariff talks, which all affect the 10-year US government bond yield that rose 24bp in May to 4.4% (not too much change from 4.57% at the end of December). The market’s warning to Washington that it needs to put the fiscal house in order is loud and clear (See Econ/Invest #2).

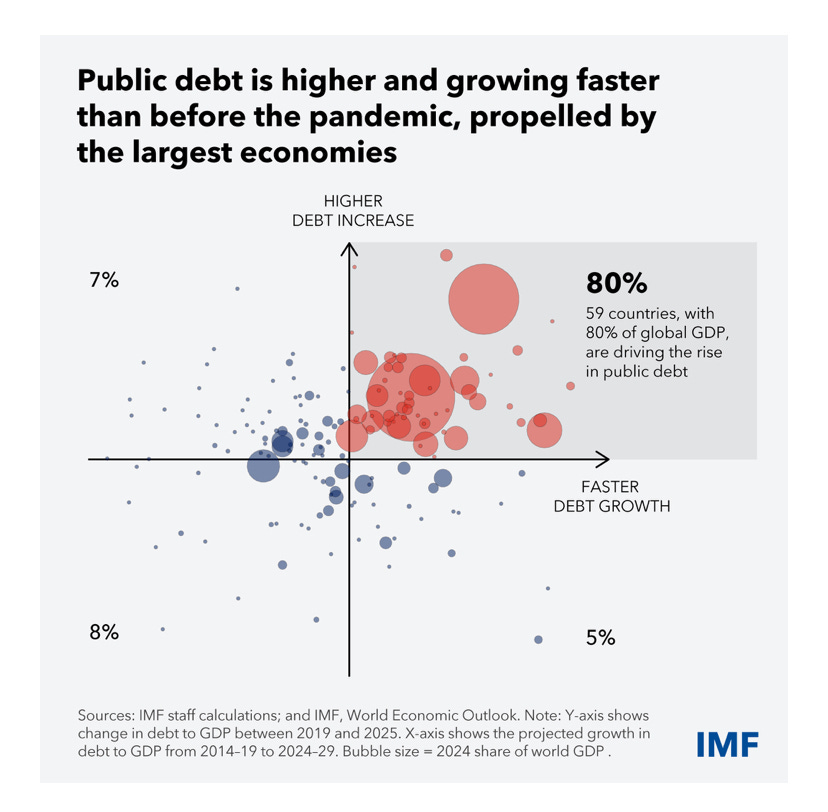

The two graphs below show that the US has increasingly financed itself with short-term bills to save costs (albeit roll-over risks are higher), while its public debt burden is projected to rise from 108% at the end of 2019 to 122% in 2025 and 128% in 2030 (IMF).

JP Morgan’s CEO Jamie Dimon warned of a crack in the bond market to come soon, and “If we are not the preeminent military and the preeminent economy in 40 years, we will not be the reserve currency. That’s a fact. Just read history.”

To end on a positive note on the market, I share

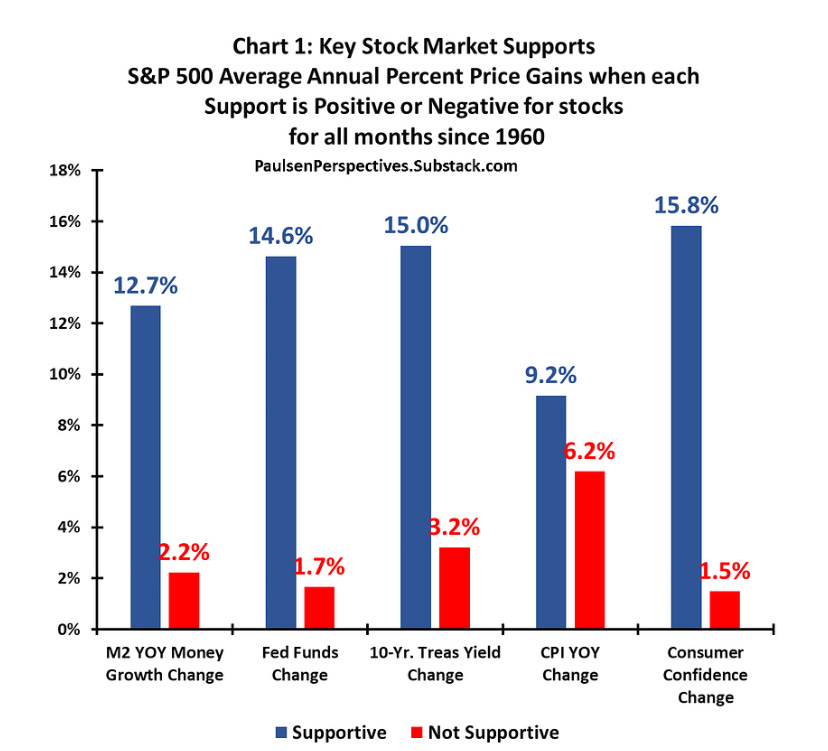

’s chart below showing how the following five factors (depending on whether they were positive or negative for stocks for the month) have driven stock market annualised performance since 1960. Should inflation and the Fed cut rates and consumer confidence rebounds (all are unused stock market support), a bull market can continue.

This week we will monitor US May ISM manufacturing index on Monday, the May ISM Services on Wednesday, April trade balance on Thursday, May non-farm payrolls, unemployment rate, and average hourly earnings on Friday, the Euro Area May inflation and April unemployment rate on Tuesday, May Composite PMI Index on Thursday, and the ECB interest rate decision on Thursday as well as the May Caixin manufacturing PMI index in China on Thursday.

Economy and Investments (Links)

Trade Threats Consume the Economy (Axios)

Even if the courts decide Trump's expansive tariffs are illegal, the White House can implement the levies through other authorities.

Wall Street Warns Trump Aides the GOP Tax Bill Could Jolt Bond Markets (The Washington Post or Archive)

“I don’t just hear it from D.C. policy people, I’m hearing it from market participants. When you’re hearing it from the people who are actually trading on the information, that gives it a much higher level of credibility than people trying to use it for political purposes,” said George Callas, who served as senior tax counsel to former House speaker Paul D. Ryan (R-Wisconsin) and now leads the public finance team at Arnold Ventures, an advocacy group. He added of Wall Street investors: “They’re saying they’re really worried about Congress’s fiscal policy. Those warnings are really growing. If you don’t hear them, it’s because you don’t want to hear them.”

What It Means to be Illiquid (The Economist or Archive)

Private equity and venture-capital firms have struggled to sell their existing investments since 2022, when central banks raised interest rates, [thus reducing the distribution to investors.]

Finance/Wealth (Link):

The Value of Not Being Sure (Seth Klarman via

)It is much harder psychologically to be unsure than to be sure; certainty builds confidence, and confidence reinforces certainty. Yet being overly certain in an uncertain, protean, and ultimately unknowable world is hazardous for investors…uncertainty also motivates diligence, as one pursues the unattainable goal of eliminating all doubt. Unlike premature or false certainty, which induces flawed analysis and failed judgments, a healthy uncertainty drives the quest for justifiable conviction.

The Idea (Link):

Consultants Are Taking Over the World’s Corner Office (Bloomberg)

What’s behind this shift? One catalyst is the move by the Big Four accounting firms beyond auditing into strategy and execution. As they’ve expanded their scope, these firms have snatched up more of the best and brightest undergrads and MBAs. Once there, they’re trained in technical know-how, problem-solving and softer skills, while acquiring expertise across entire industries rather than at just one company. And though consultants have a reputation for parachuting in to deliver a buzzword-laden strategic vision, they also stick around to do the hard work of installing new technology and processes to improve their clients’ business.

“They are infiltrated everywhere inside corporations, and what they’re doing is much more hands-on — that’s good training for how companies are run,” says Tom Rodenhauser of Kennedy Intelligence, which covers the consulting sector. “You combine all those things, and they make good profiles for CEOs.”

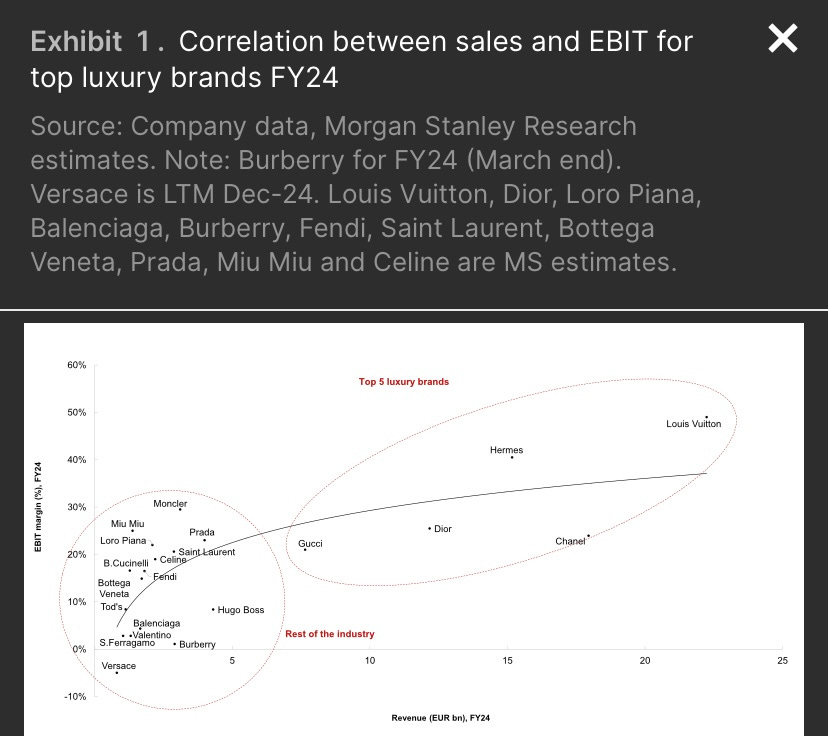

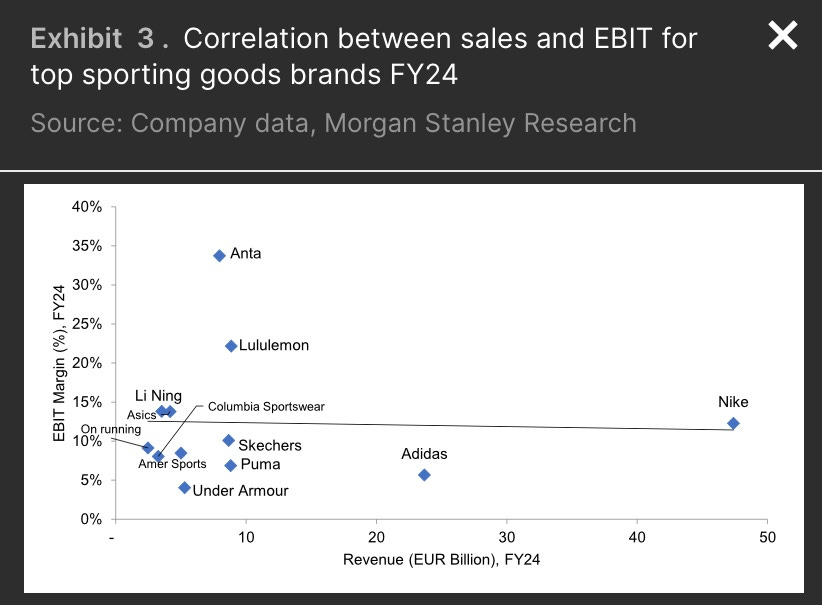

One Chart You Should Not Miss: Correlation Between Size and Profits in Luxury Brands

According to Morgan Stanley, in the luxury goods sector, focusing on the top 20 brands, the profitability correlates highly with size (increasing from 0.65 in 2016 to 0.74 in 2024). In contrast, the correlation is very low in the global sporting goods sector.

The top 5 mega brands (Louis Vuitton, Chanel, Hermes, Dior, and Gucci) accounted for 72% of revenue growth and 87% of profit growth from 2016 to 2024. While in 2025 the personal luxury market is likely to contract (~3.5%), the long-term competitive advantage of scale of the “mega luxury brands” will continue.

One Term to Know: What is the Purpose of Stablecoins

Stablecoins are cryptocurrencies designed to maintain a consistent value. The primary purpose of stablecoins is to provide stability within the cryptocurrency market. The stability is achieved as the value of stablecoins is pegged to other assets, such as fiat currency or a reserve asset (like the U.S. Dollar), commodities (like gold), or another financial instrument.

The most popular and largest stablecoin tokens by market capitalization is Tether (USDT) (~$153 billion), followed by USDC (~$61 billion) at the point of writing.

As of Q1 2025, USD stablecoins have surpassed $220 billion in market capitalization (representing 99.8% of all fiat-denominated stablecoins) and now account for roughly 1% of U.S. M2. Stablecoin issuers are now the 20th largest holder of US Treasuries.

New US Stablecoin legislation is opening the door for new market entrants, including banks and enterprises, whose extensive distribution channels could drive competition and shift market dynamics.

Stablecoins are not bitcoins. By avoiding volatility in prices, as in other popular cryptocurrencies, stablecoins can be useful for:

efficient transactions, whether for everyday purposes or trading on crypto exchanges

playing the role of a store of value

bridging money movement between traditional finance and the decentralized finance (DeFi) ecosystem

faciliating DeFi applications by serving as collateral in lending and borrowing platforms and providing liquidity for decentralized exchanges.

🌻Things I learned About AI/Productivity

Claude 4, Anthropic Agents, Human-AI Agents (Stratchery)

It remains to be seen how far away we truly are from agents that are reliable enough to be left alone to do work, and, needless to say, there are major second-order effects that will result from this being the case. In the meantime, however, I think there is a massive AI-enabled opportunity that is currently being missed by all of the major model-makers, or at least their product teams: human-AI agents.

The AI Hype Index: College students are hooked on ChatGPT (MIT Technology)

AI could also finally lead to a better battery life for your iPhone and solve tricky real-world problems that humans have been struggling to crack, if Google DeepMind’s new model is any indication. And perhaps most exciting of all, it could combine with brain implants to help people communicate when they have lost the ability to speak.

3. Gemini Gets More Personal, Proactive and Powerful (Google)

I agree that Gemini is very easy and more intuitive to use than ChatGPT. Just load up say a painting in your camera and ask a question. ChatGPT can’t even do that!

I'm not afraid to say it, I use Gemini more than I use ChatGPT, and honestly, I think it's just easier to use. The other day I used Gemini Live to help cook a meal, and it was incredible asking AI questions based on what it could see through my smartphone's camera. Gemini also offers Deep Research, which we've tested thoroughly, and even image and video generation that's as good as some of its competitors. In terms of consumer AI tools, Gemini is leading the pack in my opinion, and I expect Google to further the gap with OpenAI's ChatGPT at I/O later today. ChatGPT may be more powerful depending on your use cases, but for the average consumer, Gemini ticks all the boxes. ~Techradar review

Thanks for reading!

Please do not hesitate to get in touch if you have any questions.

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.