Weekly Good Reads: 5-1-1

US Jobs, UK Elections, Q3 Equity Market Outlook, Thinking Like a Lawyer, Most Livable Cities, NAIRU

Welcome to Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

Each week I share insightful/essential readings, charts, and one term, incorporating some of my market observations. You can find the weekly changes of the major indices or indicators in the Weekly Change charts. But I look beyond data and share something enlightening about life, health, technology, and the world around us 🌍!

Here’s the quote of the week:

Showing off is the fool's idea of glory. ~ Bruce Lee

I archived my Weeklies here and the index of charts and terms here. Check out my conversations with Female Investors and more, which I hope will inspire more females into finance and investment careers 🙌. Easily subscribe to my newsletter by clicking below.

Feedback is important to me, so if you like the Weekly, please “heart” it, comment or share it with your contacts. Thank you so much for your support🙏.

Market and Data Comments

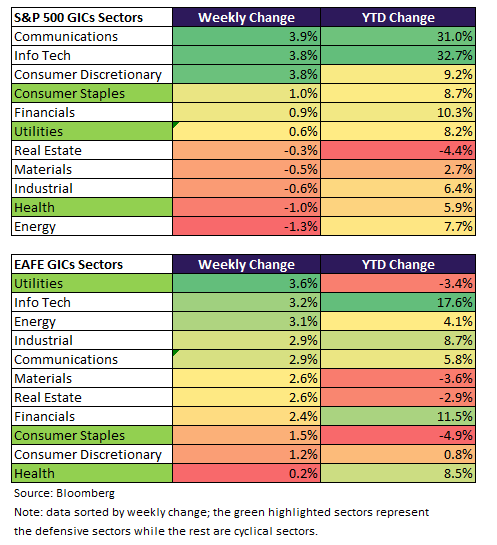

The US stock markets rose 2% (S&P 500) and 3.5% (Nasdaq) this past week as 2y and 10y government bond yields tumbled 15bp and 12bp respectively.

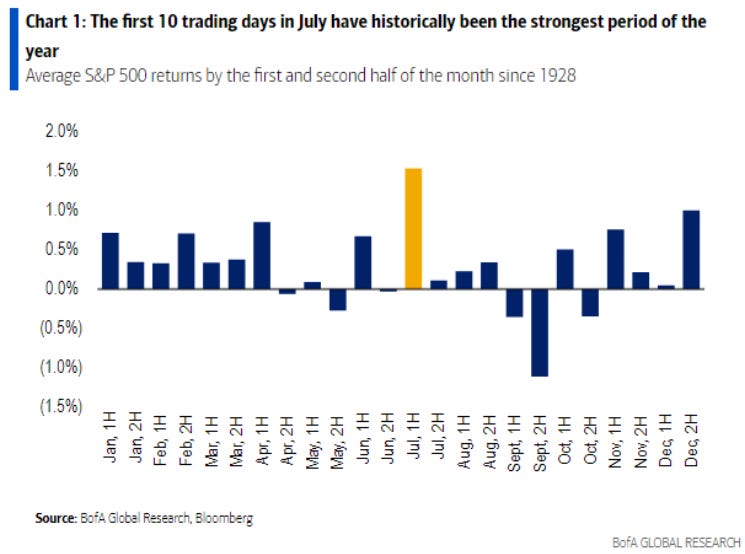

Bank of America research (graph below) found the first 10 trading days of July since 1928 have been the strongest period, rising 70% of the time and up on average 1.5%. So far in July, the US stocks are doing even better.

This week’s US stock rally, led by the communications, infotech, and consumer discretionary sectors, has been propelled by a slowing but still robust labour market, leading to the expectation of a September Fed Fund rate cut. Strong wage growth, easy fiscal policy, and AI-fuelled stock gains (wealth effect) have kept the US economy strong.

The US added 206,000 jobs in June but revised April and May’s numbers down by 111,000, resulting in a 3mma payroll gain of 177,000, while the June unemployment rate inched up +0.09% to 4.05%, which is close to triggering the “Sahm Rule” (requires +0.5% and more), an indicator of the start of a recession.

One reason to explain the rapid rise in the unemployment rate (apart from the rising number of unemployed) is the rapid increase in labour supply which means jobs cannot catch up with the increase in workers. Remember the Fed has a dual mandate of maintaining price stability and full employment so the labour market conditions will be in focus in 2H 2024. Fed’s estimate of the long-term unemployment rate is 4 to 5% (now 4.05%).

The slowing labour market is accompanied by a weakening in services ISM (-5 points to the contractionary 48.8 in June). The market has now fully priced in two rate cuts starting in September and is keenly watching if core PCE will be 0.2% m/m in June and July and below 0.2% m/m in August to confirm a September rate cut.

Of note this past week was fireworks in the US (literally and figuratively about Joe Biden’s candidacy) and in the UK (the Labour Party had a landslide win, ending 14 years of chaotic Conservative Party rule.) Here’s a fun take on the UK election outcome.

The newly-elected UK Prime Minister Keir Starmer promised “stability and moderation” after turmoil in the previous governments and weak real GDP growth performance (Q1 2024 was 0.3% y/y) since end-2021, hurt by the cost of living housing crisis ever since interest rates jumped over 5% (mortgages are mainly 2 to 5 years). This caused consumer spending to suffer. The new Chancellor Rachel Reeves promised “the most pro-growth Treasury in our country’s [UK’s] history”.

This coming week we will monitor the US June CPI on Thursday and PPI on Friday, China’s June aggregate financing next week, June CPI and PPI on Wednesday, and June exports on Friday as well as the French parliamentary elections (second round) next week.

Economy and Investments (Links):

Are Markets Broadening? + Q3 Equity Market Outlook (BlackRock)

This earnings season fell in line with our expectation that software, semis, and broad tech would remain leaders. We don’t think that a market-wide broadening is a necessary occurrence insofar as earnings remain concentrated in certain sectors – the market chasing after fundamentals means that it’s doing its job!

Our team has focused on leaning more into tech+ and where earnings have the most potential. Right now, we think that techy sectors continue to provide us with an ample earnings engine while we buy others selectively and hunt for tactical opportunities.

Getting It Right: Meeting Uncertainty (Speech by Mary Daly, President of the (Federal Reserve of San Francisco)

1 Big Thing: The Case Against the Doom-and-Gloom View for American Workers (Axios Macro based pm the Report on American Work Project: Toward a New Consensus)

Finance/Wealth (Link):

The Federal Reserve’s Little Secret (The Atlantic)

Given all that, you might reasonably expect the relationship between interest rates and inflation to be thoroughly understood by the economics establishment. Not so. Over the past two years, reality has looked nothing like the theories found in economics textbooks. The uncomfortable truth is that no one really knows how interest rates work or even whether they work at all—not the experts who study them, the investors who track them, or the officials who set them.

Wellness/Idea (Link)

Why Everyone Should Think Like a Lawyer (The Economist or via Archive)

Perhaps the most valuable lesson from lawyers is both the most obvious and the most scorned. The antidote to work anxiety is not taking your mind off work with meditation or Netflix. It is disciplined preparation. There are rewards in leaving no stone unturned. By putting in the hours, even if these are not billable, managers can ensure they are as ready as they can be for the uncertainties that lie ahead. As an added bonus, hard graft wins them the respect of colleagues and subordinates.

+ Can You Tell Me Something Hopeful?

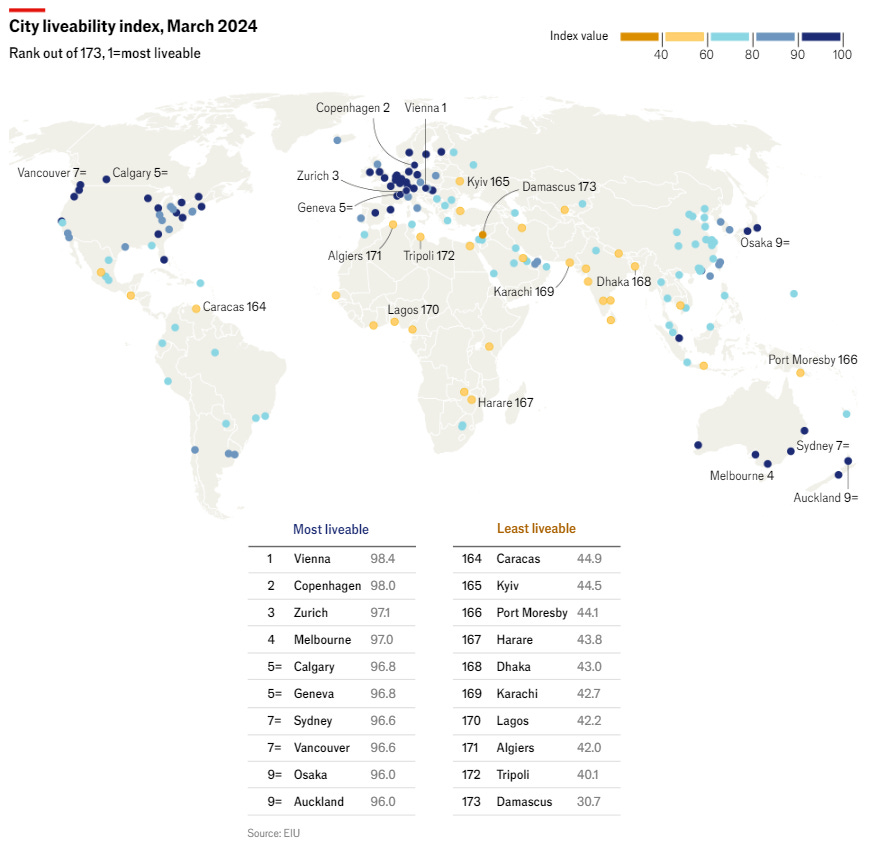

One Chart You Should Not Miss: The World’s Most Livable and Expensive Cities (Archive links: here and here) (Source: EIU)

The EIU ranks 173 cities in 5 categories: stability, health care, culture and environment, education, and infrastructure. Vienna tops the rank for the third year in a row, while Hong Kong (my home country) is the biggest climber and Tel Aviv the biggest faller.

European cities occupy the top 3 and the best 4 out of 10 (4 Asian cities are also in the top 10). Zurich and Geneva are both amongst the most liveable and most expensive cities.

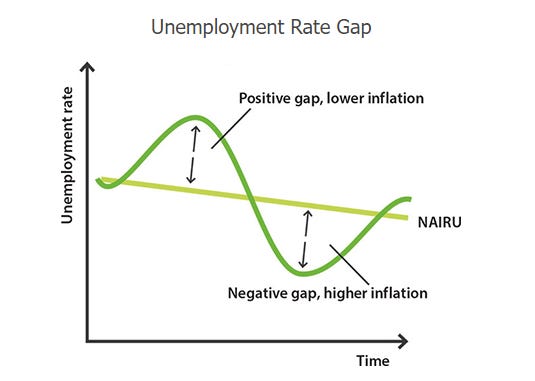

One Term to Know: Non-accelerating inflation rate of unemployment (NAIRU)

NAIRU is the unemployment rate that would result when the output gap is zero; that is when the economy is growing at its potential with no unusual wage and price pressures (St. Louis Fed). In other words, it is the lowest rate of unemployment without triggering a rise in wages and price inflation.

NAIRU is a theoretical rate; but why is it important? NAIRU (and the unemployment rate gap) is one of several tools policymakers use to assess how far the economy is from full capacity and what this means for labour market outcomes, wage growth, and inflation.

For example, if the unemployment rate is higher than the NAIRU, it means there is a positive unemployment rate gap and inflation will likely drop below the Central Bank’s target. The Central Bank may want to stimulate the aggregate demand of the economy by lowering interest rates and conducting other monetary policies, helping to lower the unemployment rate.

This trade-off between inflation and the unemployment rate is denoted by the short-run Philips Curve (dark green line). NAIRU is different from the natural rate of unemployment as NAIRU represents the unemployment rate consistent with steady inflation in the near term, say, over the next 12 months. The NAIRU is at point A. Note that in the long term, there is no trade-off between inflation and unemployment.

Factors influencing NAIRU include globalisation (e.g. freer movement of labour), up-skilling programs, underemployment, labour scarcity, or long-term unemployment, etc.

[🌻] Things I Learn About AI/Productivity:

I learned about Guidde, GPT-powered video documentation to help your team be more productive. The tool enables explanation of the most complex tasks in seconds with AI-generated documentation. The Chrome extension is free, and the free plan includes 25 videos. It looks promising for teams.

Mary Meeker, a Midas List VC and ex-Wall Street stock analyst, famous for her Internet Trends Reports (yearly from 1995 to 2019) has just published a special report “AI and Universities”.

We are fortunate that America is leading the world here and has a foundational focus on deterrence in an increasingly hostile world. Our universities and regulators have a responsibility to rapidly and deeply understand the global stakes that AI presents for freedom, democratic values, good and evil…and take strong stands. AI creates once-in-a-lifetime opportunities for evolution, creativity and leadership (akin to the post-WWII Space Race). As these things are, it’s riddled with risks. Now, we need to focus, galvanize attention and minimize our mistakes.

Ultimately, bringing AI to learning and teaching requires what Sal Khan calls “educated bravery.” While technologies developing in real-time are always unpredictable, their thoughtful use may well prove exponentially beneficial to students and teachers alike. We should not be paranoid and restrictive about utilizing these technologies, but thoughtfully curious.

BIS Annual Economic Report 2024 (BIS)

Their annual economic report drew lessons over the last quarter of the century on monetary policy and included a special overview of AI’s economic impact.

The centrality of data demands a rethink of central banks’ traditional roles as the compilers, users and disseminators of data…Our conventional approach to data favours using existing structured data sets organised around traditional statistical classifications. However, the age of AI will rely increasingly on unstructured data drawn from all walks of life, collected by autonomous AI agents. Data availability and data governance are key enabling factors for central banks’ use of AI. Both will require investment in technology and in human capital. Above all, the challenges of the age of AI necessitate close cooperation among central banks. Central banks need to come together to foster a “community practice” to share knowledge, data, best practices and AI tools.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

Here’s my latest conversation with a female fund manager, Sachee Trivedi:

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.