Weekly Good Reads: 5-1-1

Refinancing Risks, Money Market Funds, China Exceptionalism, Sharpe Ratio, Bloomberg Tech Conference, Backward Walking

Welcome to Weekly Good Reads 5-1-1 by Marianne O, a 25-year investment practitioner and the author of

on investing, economy, wellness, and something new I learn in AI/productivity. All the Weeklies are here, and here is the index of charts and terms. You can easily subscribe to my newsletter by clicking below.Please also check out my conversations with Female Fund Managers, Investors, and more - new this year!

Feedback is important to me, so if you like the Weekly, please “heart” it, comment or share it with your contacts. Thank you so much for your support🙏.

Market and Data Comments

There were few major data releases last week except for the latest US weekly initial jobless claims, which rose 231,000, higher than the 212,000 expected and the highest level in 8 months, signalling a future rise in the unemployment rate.

The University of Michigan Consumer Sentiment Index slumped from 77.2 (end of April) to 67.4 (beginning of May), as consumers got more worried about short-term inflation and the future rise in the unemployment rate.

Elsewhere, the Bank of England kept interest rates unchanged at 5.25%. Like the Euro Area, CPI disinflation continues. April flash Euro Area CPI was 2.4% yoy, beckoning the first interest rate cut in June, while UK March inflation was 3.2% yoy with supply-side factors expected to push inflation down to the 2% target area.

June rate cuts are likely for the Euro Area and the UK, while the US is pricing in 2 rate cuts with the first one in September.

Divergence in inflation paths is in play amongst the US, Euro Area, and China (see the chart below.)

Chinese exports recovered nicely in April (+1.5% yoy vs -7.5%% in March) while imports were +8.4% yoy (vs. -1.9% in March) with hopes of economic recovery. Trade surplus between China and the ASEAN nations has grown rapidly with April Chinese exports growth to ASEAN at 20.4% yoy vs. -1.6% yoy to the U.S.

Read this discussion of “China Exceptionalism” among Chinese experts at the SIC conference, views not widely discussed in Western media.

One speaker mentioned: “…whole [China’s trade surplus] growth has come from trade with emerging markets. If you go back to just five years ago, China’s exports to Southeast Asia, to ASEAN countries was about 60% of China’s trade to the US. In the past five years, China’s trade with the US has basically flatlined. Meanwhile, China’s trade with the ASEAN has more than doubled. Today, China’s trade into Southeast Asia is 120% of China’s trade with the US. So today, for China, Southeast Asia is arguably now more important than the US.”

In other words, global decoupling is benefitting China, who has grown its exports to the fastest-growing region.

The other topic of interest is how the US utilities sector has outperformed the S&P 500 and Nasdaq (+12.3%, 9.5%, 8.9% YTD respectively) albeit underperforming the AI-charged communications sectors (+18.8% YTD). See the chart below.

Why? AI needs a lot of electricity to power the data centres, and the utilities/power sector is a clear beneficiary. Usually, AI and value themes don’t combine, but there may be a case to look at the defensive sector of utilities providing yield and a ‘growth” theme.

wrote about this exact topic with a super-interesting chart:

A Bloomberg article (see Finance/Wealth section below) discussed the looming debt refinancing for the small-cap companies in the US, much higher than that of the S&P 500 (large-cap) companies (also see the chart at the top). That is likely why investors still flock to the quality large-cap companies including the “Magnificent Seven” - the Russell 2000 (small-caps) only rose 1.6% YTD vs 9.5% of the S&P 500.

In the coming week, we will monitor the US’ April PPI on Tuesday, April CPI and retail sales on Wednesday, April housing starts on Thursday, and China’s April PPI and CPI on Saturday, April retail sales, industrial production, and fixed asset investment (YTD to April) on Friday.

Economy and Investments (Links):

The big picture: At the {Milken Institute Global} conference, many suggested that it was the ZIRP phenomenon of the 2010s that was an anomaly — not the current period of high rates….

The bottom line: "When people talk about inflationary pressures from all the AI investment, the energy transition or deglobalization — all that means is that the interest rates necessary to keep inflation at 2% will have to be much higher," Carlyle's Thomas said.

Four Reasons We Are at Peak Goldilocks and Why That is Not Good (Bloomberg or via Archive)

Will a Computer Take My Job? (Constance Hunter on LinkedIn)

…while a computer may take your job, it may also give you a substitute job that pays more because it adds more value to an enterprise, as was the case for workers who switched from retail to warehouse work during the pandemic.

Finance/Wealth (Link):

A $600 Billion Wall of Debt Looms Over Market’s Riskiest Stocks (Bloomberg or via Archive)

Wellness/Idea (Link)

Backward Walking Is the Best Workout You’re Not Doing (Time)

Backward walking is an underrated way to engage your glutes, shins, and the muscles in your feet and ankles, says Joe Meier, a Minnesota-based personal trainer and author of Lift for Life. Plus, it mitigates the impact of each step, reducing the force exerted on the knees and lower back. Part of its appeal, he adds, is that it’s so accessible—and suitable for people of any age and fitness level.

+ How Bad are Ultraprocessed Foods, Really? (New York Times or via Archive)

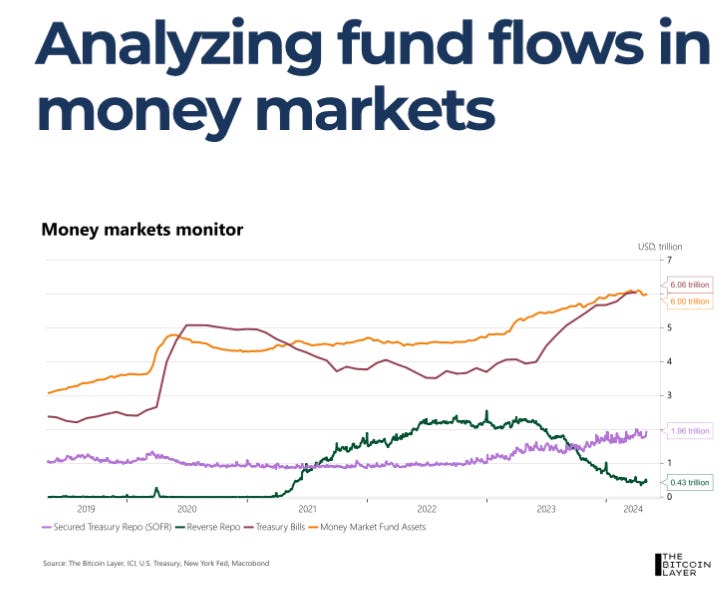

One Chart You Should Not Miss: Fund Flows in Money Markets

Note how Money Market Funds (MMF) in the US are allocated across the above 4 instruments.

Since May 2023, the Fed’s reverse repo flow has declined while that of private market repo (SOFR) (due to larger Treasury issuance) and Treasury Bills (due to rising yields) have increased.

Within the money market, funds are also shuffling away from credit assets (prime) to government-issued securities - Treasuries, agency, and repo - as the SEC will make it more expensive for investors to yank money out of the credit-based MMF starting in October as per Bloomberg.

One Term To Know: Sharpe Ratio

For fund managers and their investors, an important statistic to compare investment performance is the Sharpe Ratio, which measures the excess return of the portfolio over the risk-free rate (or sometimes over an industry benchmark) divided by the volatility (measured by standard deviation) of the portfolio excess returns (or portfolio returns).

It calculates the risk-adjusted return of an investment, relative to a riskless asset such as US T-bills or Treasury Bonds. It is not enough to know the projected return of an investment; more importantly, does the extra volatility the investor is taking justify its returns?

Sharpe Ratios are useful in comparing the risk-return tradeoffs of different investments/funds/portfolios/stocks, for different historical periods, or future periods. Portfolio managers can also adjust their portfolio investments to achieve a desired level of Sharpe Ratio. The higher the Sharpe Ratio, the higher (better) the risk-adjusted return. A Sharpe Ratio of at least 1 is considered good.

For example, fund A has an expected return of 12% and a portfolio volatility of 15%, while fund B has a projected return of 10% and a portfolio volatility of 9%. The risk-free rate is 3%. Fund B has a higher Sharpe ratio of 0.78x versus Fund A’s 0.6x despite Fund B having a lower expected return.

While the Sharpe Ratio is easy to calculate, it has several limitations due to its restrictive assumptions:

(1) It assumes stock returns have a normal distribution, ignoring fat tails and skewness of returns.

(2) It is highly sensitive to the period and the risk-free rate chosen. A risk-free rate has to be chosen appropriately and cannot be a constant.

(3) The Sharpe ratio is calculated based on historical data, which does not represent what the future risk-adjusted return will be.

(4) Sharpe ratios only consider risk and return metrics. When comparing funds/ portfolios, other factors may need to be considered: for example, the investment process, style, sector exposure, etc.

[🌻New] One Thing I Learn About AI:

I end with some thoughts and quotes from the best of Silicon Valley’s minds at the recent Bloomberg Technology Summit in San Francisco (please see my LinkedIn post.)

The event was 90% about AI (the future and risks), but topics on healthcare cyberattacks and California building a new city northeast of San Francisco also stirred up concerns and interests.

The celebrity at the conference was Ameca, the humanoid built by Engineered Arts.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more!

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

I’m all caught up now! Great read to start my Sunday!

Mounting debt will be a big problem for already underperforming small caps. This is a natural consequence of the increasing market concentration. This is not very alarming for consumer companies but I would avoid small cap tech stocks that require huge capex. Their innovation spaces will likely be dominated by the mega caps.