Weekly Good Reads: 5-1-1

FOMC, Argentina and Fiscal dominance, After-tax performance, Five No’s, Economic Moat

Welcome to Weekly Good Reads 5-1-1 by Marianne O, an investment practitioner and author of

about investing, economy and wellness ideas. Every week I include 5 links to relevant economic and investment, finance and wellness/idea pursuit as well as 1 important chart and 1 term to know. All the Weeklies are here and here is the index of charts and terms. You can easily subscribe to my newsletter by clicking below.Thank you for reading this Weekly and supporting my work 🙏.

Market and Data Comments

The stock market was in a happy mood this week. Given the Thanksgiving holiday, the only noteworthy US economic news was the November Fed FOMC minutes, which shows the Fed’s likelihood to pause again in December. This was due to their concern for tightened financial conditions and the rise in the long-term yield pushed up by a higher term premium which would slow down the economy (both have eased since then.) However, the 1-year consumer inflation expectations rise to 4.5% (the highest level since April) would point to expectations of stickier inflation ahead and the Fed keeping rates higher for longer.

The Fed now focused on slowing the economy below “potential” (short-term production capacity) as opposed to below “trend” (long-term capacity), which shows the Fed may view a stronger economic momentum as not threatening disinflation and therefore not hike any further.

The retailers warned Black Friday’s sale looked more sluggish than last year, and the rich has been curtailing spending pre-Thanksgiving sales (see Econ and Investments link No. 1 below).

Elsewhere, Europe Flash November PMIs for both manufacturing and services both surprised slightly on the upside. Despite market fear, Italy did not get downgraded to non-investment grade by Moody; in fact, Italy got an upgrade on its sovereign outlook.

China’s data continued to disappoint with both stagnant retail sales in October and declining new home prices of 0.4% month-on-month (the largest decline in 9 years). Barclays is optimistic China will stimulate more as a result. For example, the Chinese government is likely to finalize help for 50 developers (both private and public) with their financing, the shortfall has been estimated at a whopping $446 billion. If so, Q1 GDP growth in China will likely rebound.

Looking at the world, interest rates may look like they will be synchronously coming down next year or so (see the above graph by Deutche Bank on the actions of 81 central banks.)

Bloomberg Economics’ Nick Hallmark notes that the Fed, the European Central Bank and the Bank of England have likely finished raising rates as inflation softens and recession risks mount. There are outliers of course, notably Turkey and Argentina, which face extreme price pressure. But overall, nations are entering a new regime. Inflation is sufficiently under control that cuts are likely to continue outnumbering hikes next year.~ Bloomberg

Next week we will monitor US Q3 real GDP (second-release, expectation at 5.0%) on Wednesday, October core PCE and personal spending on Thursday, and November ISM Manufacturing on Friday. We will also look out for Euro area November consumer price index and the delayed OPEC + meeting on Thursday.

We now know that OpenAI has rehired Sam Altman, and who wins? Microsoft, and on all fronts in Gen AI.

Economy and Investments (Links):

Is the US Headed for a Recession? Look at What Richer Americans Do on Black Friday (Bloomberg or click here)

If You're in Cash, You Risk Missing Out, Bond Managers of $2.5 Trillion Say (Bloomberg)

Any lessons for the US from Argentina?

The U.S. is the antithesis of Argentina [whose central bank is completely subordinated to its treasury in addition to Argentina’s excessive government spending and many malaises for decades]: It has an independent central bank, little exposure to currency fluctuations and unparalleled access to capital markets. True, in 2020-21 Congress issued trillions of dollars of debt, some of which the Fed purchased under its quantitative easing program to ease borrowing conditions.

By early 2021, the broad money supply had soared 25% from a year earlier, in retrospect a tipoff that demand was growing too fast for supply to keep up. Prices soared. Still, if this was fiscal dominance, it was short lived. The stimulus ended, the Fed raised interest rates, the money supply is now contracting and inflation is closing in on the Fed’s 2% target.

Some economists—proponents of the “fiscal theory of the price level”—think inflation will rebound. “You’re seeing interest payments start to explode and it’s not obvious Congress is going to pay for that” by cutting spending or raising taxes, said Eric Leeper of the University of Virginia. Lackluster bidding at recent auctions of Treasury debt are “a pretty early indicator people are concerned about the possibility of fiscal dominance.” ~WSJ

Finance/Wealth (Link):

SPIVA After-Tax Scorecard: The Effect of Taxes on Indices and Active Funds (S&P Global)

20 years of S&P Dow Jones Indices’ SPIVA Scorecards collectively attest that the ability to consistently identify the right time to sell in order to “beat the market” is relatively rare.

But the difficulty of successful market timing and stock picking are not the only factors in favor of the patience encoded in indices like the S&P 500. Further grounds may be provided by considering that even the sale of long-held profitable positions can invite unwelcome tax consequences, while the gains from short-term trading activity are normally diminished by a yet higher tax rate. Accordingly, it might seem reasonable to conjecture that outperforming broad, capitalization-weighted indices might prove even harder after accounting for the tax consequences of active trading (S&P Global)

As John Bogle's (King of passive investing) portfolio attests, use a two-asset strategy by buying a U.S. total stock market index fund and a U.S. bond market index fund to minimize tax liability and get long-term exposure to the market.

Wellness/Idea (Link):

Five Nos (Friday Forward Substack)

+ Another Reason To Be Thankful: Gratitude Can Seriously Boost Your Heart Health, According to Science (Well + Good)

Can you be more grateful - a few tips from AHA? 💖

Reflect on happiness: What makes you happy? Who or what makes your life easier? Whom do you appreciate?

Find joy: Where is your favorite place to be? What uplifts you on tough days? Recall a joyful memory that makes you happy.

Consider personal achievements: Think about something you have accomplished. Reflect on recent achievements. What are you looking forward to? (American Heart Association)

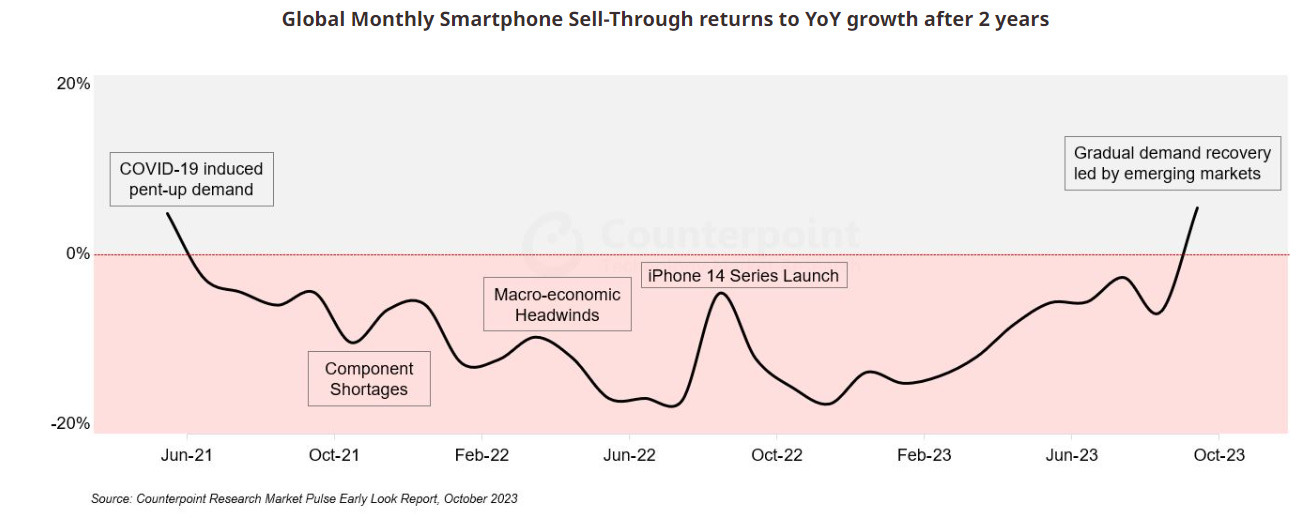

One Chart You Should Not Miss: Global Monthly Smartphone Sales

Research firm Counterpoint found that smartphone sales rose 5% yoy in October. This was the first month of year-on-year growth in smartphone sales in over two years. IDC, another research, expects cell growth sales growth in 2024.

Morgan Stanley also found there are “record upgrade intentions”, fuelled by the emergence of more powerful phones to deliver AI services. Time to look at global smartphone stocks, says Morgan Stanley.

One Term To Know: Economic Moat

The term was coined by Warren Buffet and the Moat of a company is its competitive advantage over the other companies in the same industry, thereby protecting its long-term market share and profit growth.

One example of an economic moat is a company’s large size, creating economies of scale. This is related to another moat such as sustainable low-cost advantage. Often large-scale companies can source raw materials much cheaper than smaller competitors because of their clout with suppliers.

A relatively easy way to measure moat is by looking at the gross margin of a company (revenue minus cost of sales; gross margin/sales = gross margin in %). Gross margin measures how efficient the company’s core operation is in generating profits. A high gross margin shows a company can retain a significant portion of its revenue as profit before accounting for operating expenses, interest, and taxes. A higher ratio also likely shows the company’s higher cost management/pricing ability and production efficiency.

Please do not hesitate to get in touch if you have any questions! If you like this weekly, please share it with your friends or subscribe to my newsletter.