Weekly Good Reads: 5-1-1

Job reports, bond sell-off, Bidenomics, and Janus words

Welcome to another issue of 5-1-1! I am Marianne O, an investment professional and author of The Learner’s Mind on investing, economy, and wellness ideas. For this Weekly, I include 5 links to relevant economic and investment news, finance, and wellness/idea pursuit based on what I read. I also include 1 important chart and 1 investment term to know. You can easily subscribe to my newsletter by clicking below.

Market and Data Comments

The global equity market drifted down 1.31% this week: the S&P 500 coming down 1.11% and Nasdaq down 0.91%. Except for real estate, all sectors are down this week after an exceptional first-half equity performance.

The below chart shows how the technology, communications services, and consumer discretionary sectors (cyclical/growth sectors) led the S&P 14.57% rally year-to-date while the energy sector (last year’s biggest winner) turned negative and performed the worst this year.

June US Employment report shows a slower-than-expected gain of 209,000 (309,000 in May) but this slowdown is still not big enough to prevent a July interest rate hike.

Of note is the slowdown in private sector payrolls in services in the leisure and hospitality sector after the backfilling of positions earlier this year while government jobs backfilling has increased.

Better news for the Fed: the wage-price passthrough has not been that significant for decades, according to Morgan Stanley. The slowing trend in jobs growth and inflation may support July being the last rate hike this year. Here is why Goldman thinks core inflation will keep declining.

The big news this week is the move up in US government bond yield, which has wiped out any price gains of bonds this year. 2 and 5-year government bond yields moved to the highest level since 2007, while the 10-year yield moved above 4%, this year’s high. The bond yield rose even more elsewhere since mid-May in the UK, Australia, and Canada. Why? They all reflect the repricing of the interest rate paths of the central banks.

That surprised many forecasters who preferred bonds over stocks earlier this year. The stock market rally has also been fueled by investors being too defensive and playing catch-up in riskier assets.

Next week’s important data include US consumer price inflation on July 12 and the major U.S. banks’ earnings reporting.

Economy and Investments (Links):

Greedflation is a Nonsense Idea (The Economist or click here.)

10 Top Company Stocks to Watch in Q3 2023 (Bloomberg Intelligence)

The US Middle Class’s Economic Anxiety Will Decide the 2024 Election (Bloomberg or click here.)

Finance/Wealth (Link):

Bond bull markets: lessons from the past (FT) - this is an important lesson for those investors seeking safe havens. Bonds experienced a 40-year bull market due to disinflation and deflation. These bullish factors are no longer. One thing we do know, interest rate peaks are closer than ever before, so switching to longer-duration bonds starts to make sense.

Wellness/Idea (Link):

Why You Believe The Things You Do (Morgan Housel)

A lot of times we’re not interested in truth – we’re interested in the elimination of uncertainty, and that fact alone causes us to believe things that have little relation to reality.

~Morgan Housel

Bonus: Some words have two opposite meanings. Why? (The Economist)

Now I know why I am so confused about using “comprise” and “comprise of”. This is because some words can mean the opposite of themselves!

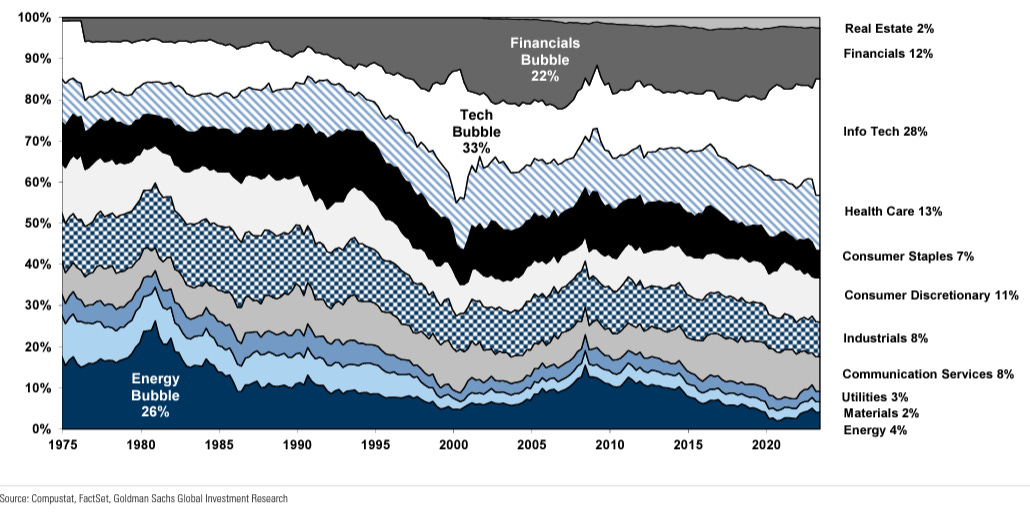

One Chart You Should Not Miss: Changing sector composition of the S&P 500 Index

In the previous Weekly, I discussed the importance of knowing first what a market index is made of when you consider buying a broad market exchange-traded fund (ETF.)

Here are two graphs from Goldman Sachs showing how the sector composition in the S&P 500 has shifted significantly from 1975 to June 2023.

The first chart shows the changes by sector by market capitalization and the second chart shows the changes by sector by net income contribution to the S&P 500. It is interesting to see while energy is only 4% by market cap, it contributes 13% of the net income! In contrast, tech is 28% of the S&P but contributes only 18% of net income (quite the opposite effect). Energy is highly cyclical so there were times when the companies made no money while tech companies saw an increasing net income contribution.

One Term to Know: Bidenomics

According to the White House, Bidenomics is rooted in the recognition that the best way to grow the economy is from the middle out and the bottom up. Its vision centre on three key pillars:

Making smart public investments in America

Empowering and educating workers to grow the middle class

Promoting competition to lower costs and help entrepreneurs and small businesses thrive

Please do not hesitate to get in touch if any questions! If you like this weekly, please share or subscribe to my newsletter.