Weekly Good Reads: 5-1-1

Jobs, Tariff Distortion, Warren Buffett's Announcement, GDP Accounting, US Dollar and Portfolio, Mental Health

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work! Please hit the 💛 button if you like it or share with others.

Sharing the quote of the week:

The stock market is a device for transferring money from the impatient to the patient.

~ Warren Buffett

Weekly archives | Investing | Ideas | Index of charts and terms | Conversations with Investment Managers

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Try R4A for free!

Market and Data Comment

One of our most respected investors, Warren Buffett, announced at the 2025 Annual Shareholders Meeting today that he would recommend to the Board (on Sunday) to pass the torch of CEO to Greg Abel at the end of 2025 (see Econ/Invest #3). The crowd cheered with a long-standing ovation. This will end 60 years of reign at Berkshire for Buffett, but he plans to be in the office every day and be “useful in a few cases”.

One notable thing he said regarding recent market volatility was that last month or so was “not a huge move” (as compared to the 1929 crash he was born into), and “has not been a dramatic bear market.” And then this great advice:

The world makes big, big, big mistakes, surprises come out from the left field…this makes the stock market a good place to focus your attention if you have the right temperament for it but a a terrible place to get involved if you get frightened by markets that decline and get excited when stock markets go up... I don’t get fearful by things that other people are afraid of in the financial ways…The world is not going to adapt to you. You’re going to have to adapt to the world…People have emotions…but you've got to check them at the door when you invest.

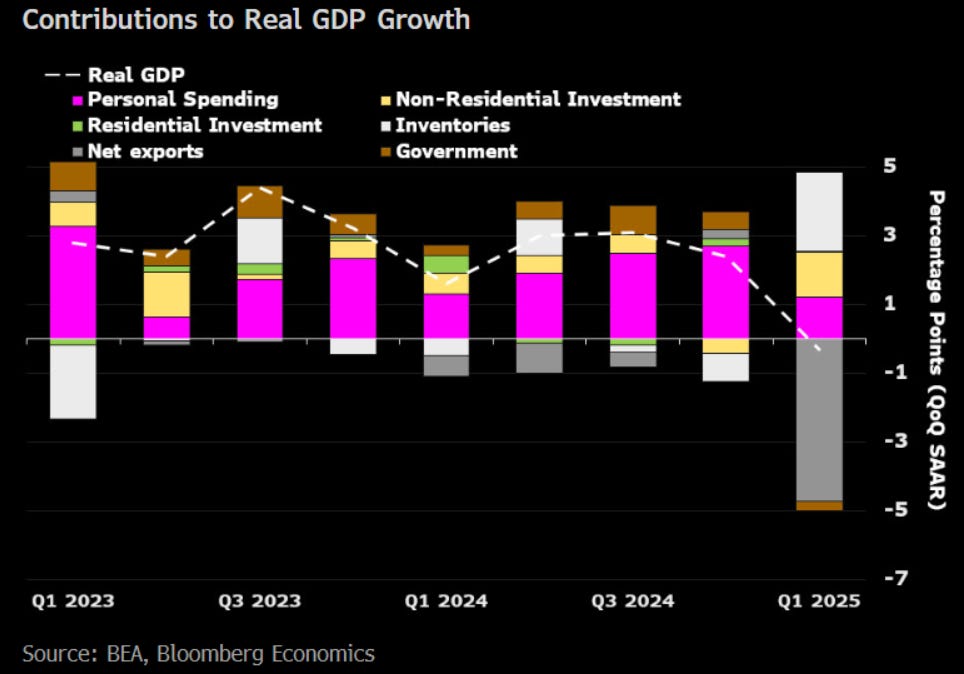

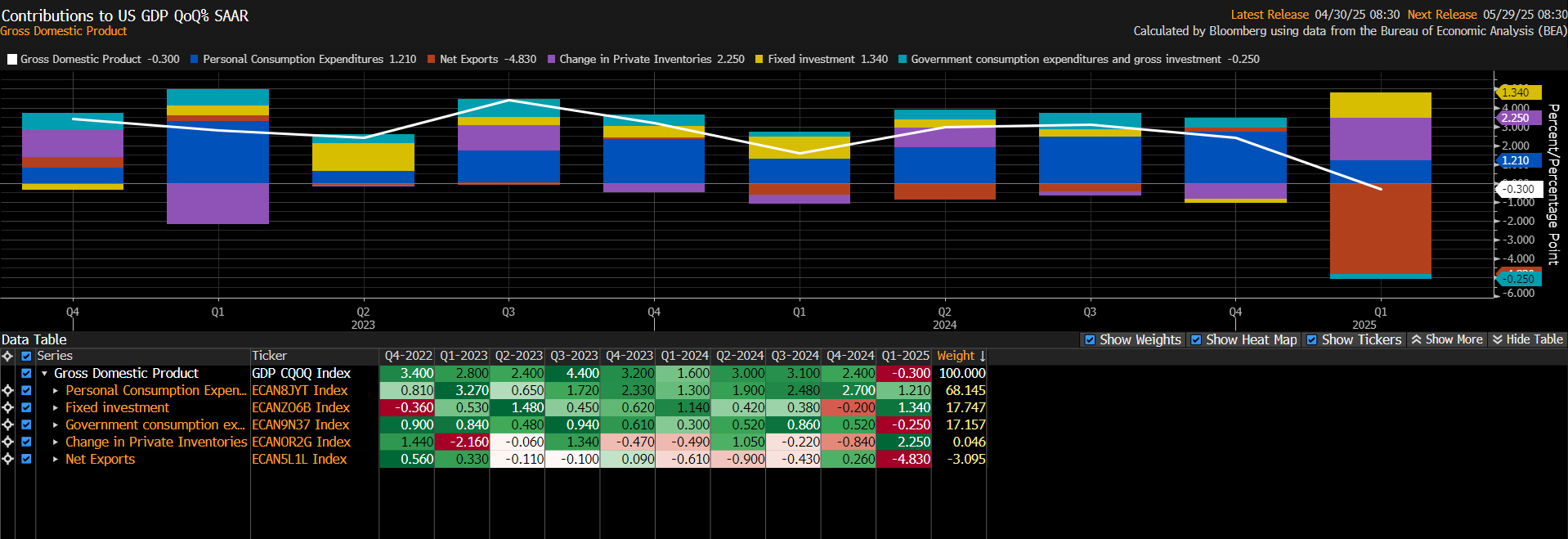

The past week gave us an initial idea of how the US economy has adjusted to the tariffs, but the real economic impact will not be reflected in the hard data until Q3.

US Q1 real GDP shrank by 0.3%, but the “final sales to domestic purchasers”, or real GDP minus international trade and inventories (see One Term To Know), was up 2.3% as some purchase decisions were pulled forward ahead of the tariffs (see chart above).

The April US payrolls grew stronger than expected at 177,000 (185k prior, 138k expected, 3m average, 155k), and the unemployment remained stable at 4.2% so far.

However, the report did not capture the full employment hit by Trump’s tariffs, and the trade* and transportation, leisure and hospitality, and construction sectors will likely get hit in the May report and beyond.

(*Linerlytica said on April 16 that container bookings for the next three weeks are reported to drop 30-60% in China.)

Bloomberg said surveyed economists saw risks from the inflationary impact of tariffs being higher than rising unemployment risks, and expects two rate cuts this year starting in September. The Fed is unlikely to cut rates in the May FOMC meeting (May 7) with the data at hand.

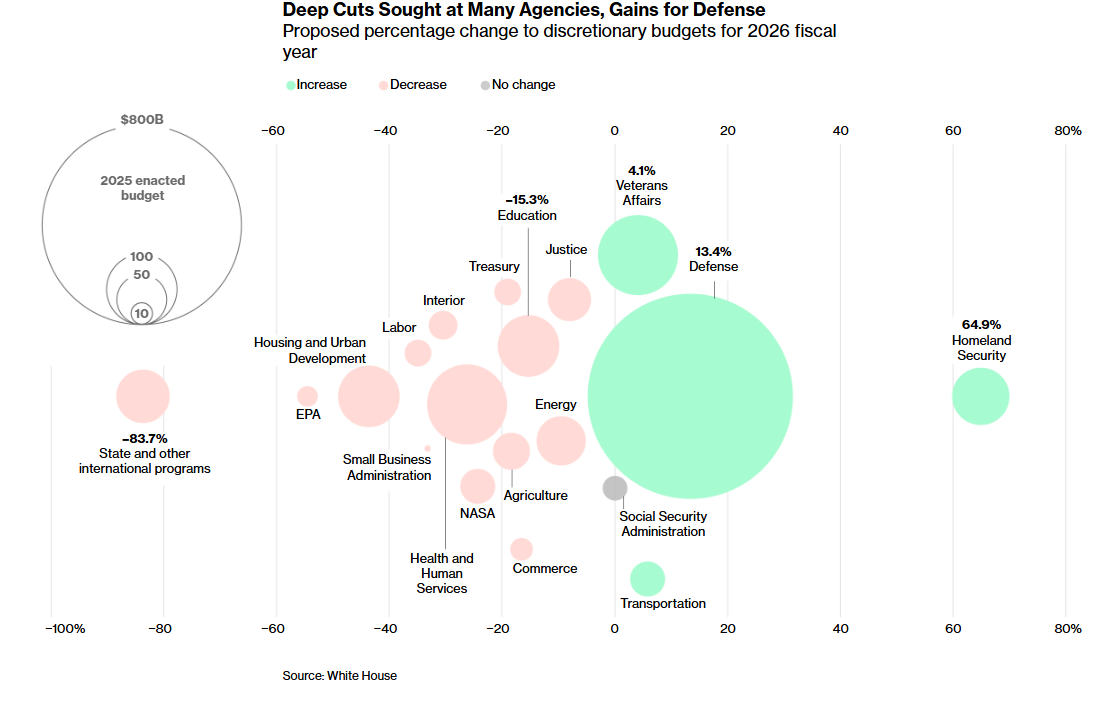

At the same time, as the Congress is preparing for a massive bill for Trump’s tax cuts priorities (expected to cost $4.6 trillion over the decade), the White House 2026 fiscal year preliminary budget came out (which rarely became reality), expecting to cut federal spending by 25% in 5 federal departments (health, clean energy, education, scientific research and international aid) but increased defence spending by 13.4% and homeland security (border security) by 65%.

China appeared ready to open trade talks with the US as “the U.S. has actively reached out to China through multiple channels to seek economic and trade negotiations,” citing unidentified “sources” (

) and is considering ways to address Trump's fentanyl concerns, while US Treasury secreatry Scott Bessent expressed trade talks optimisim with India, Japan and Korea.China’s seeming openness coincides with its manufacturing sector showing signs of a heavy hit from Trump’s tariffs. The April NBS manufacturing PMI fell into contraction (49), and employment in the exports sector would be sorely hit, and deflation will worsen.

On the back of more positive trade talk news, global stocks staged a 3% rally in the past week with the S&P 500 and the Nasdaq eliminating all losses since April 2nd’s “Liberation Tariffs”, albeit the S&P still trailed the rest of the developed world stocks (EAFE) by 15% YTD (note the Dollar Index dropped over 7.5%).

Another positive news is that capex spending growth from the US hyperscalers accelerated 71% to $81 billion, with Meta, Amazon, Alphabet, and Microsoft on track to spend $300 billion+ combined to build out AI data centres and their infrastructure.

US 10-year Treasury yield rose 7bp to 4.31% and the Dollar Index inched up 0.6% this week, while oil, copper, and gold fell 7.5%, 4.5%, and 2.4% respectively.

This coming week, we will monitor the April Euro Area PMI on Tuesday, the Fed FOMC meeting and press conference on Wednesday, the Bank of England rate decision on Thursday, and China’s April exports on Friday.

Economy and Investments (Links):

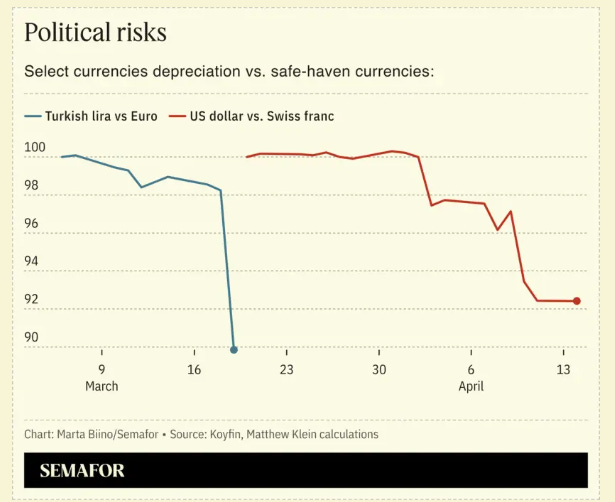

Analysis: The US is Not an ‘Emerging Market’ — Yet (Semafor)

An interesting currency comparison chart between an emerging country that is mismanaged (Turkey) and the US during the rout after April 2nd.

If they [emerging countries] make a mistake, they risk capital flight, with spiking borrowing costs and plunging currencies simultaneously crushing the economy and pushing up consumer prices. The fear of that double whammy instills discipline, which can be painful when it comes to fighting downturns, but EM policymakers know that the alternative to austerity is even worse.

It's Too Late: The Changes Are Coming (Ray Dalio)

…the United States' role as the world's biggest consumer of manufactured goods and greatest producer of debt assets to finance its over-consumption is unsustainable, so assuming that one can sell and lend to the U.S. and get paid back with hard (i.e. not devalued) dollars on their U.S. debt holdings is naive thinking, so other plans have to be made.

6 Big Things Investors Learned from Warren Buffett at This Year’s Berkshire Shareholder Meeting (CNBC)

Finance/Wealth (Link):

The US Dollar vs. Your Portfolio (A Wealth of Common Sense)

Note how foreign stocks and gold outperformed US stocks during the years when the US dollar weakened. This relationship holds well so far this year.

Wellness/Idea (Link):

Scientists are Uncovering Surprising Connections Between Diet and Mental Health (National Geographic or Archive)

The gut-brain axis and the microbiome influence many of these processes. “The microbiome is important for mental health—the gut makes 90 percent of serotonin in the body,” says Daniel Amen, a psychiatrist, founder of the Amen Clinics, and author of Change Your Brain Every Day.

More kimchi, anyone?

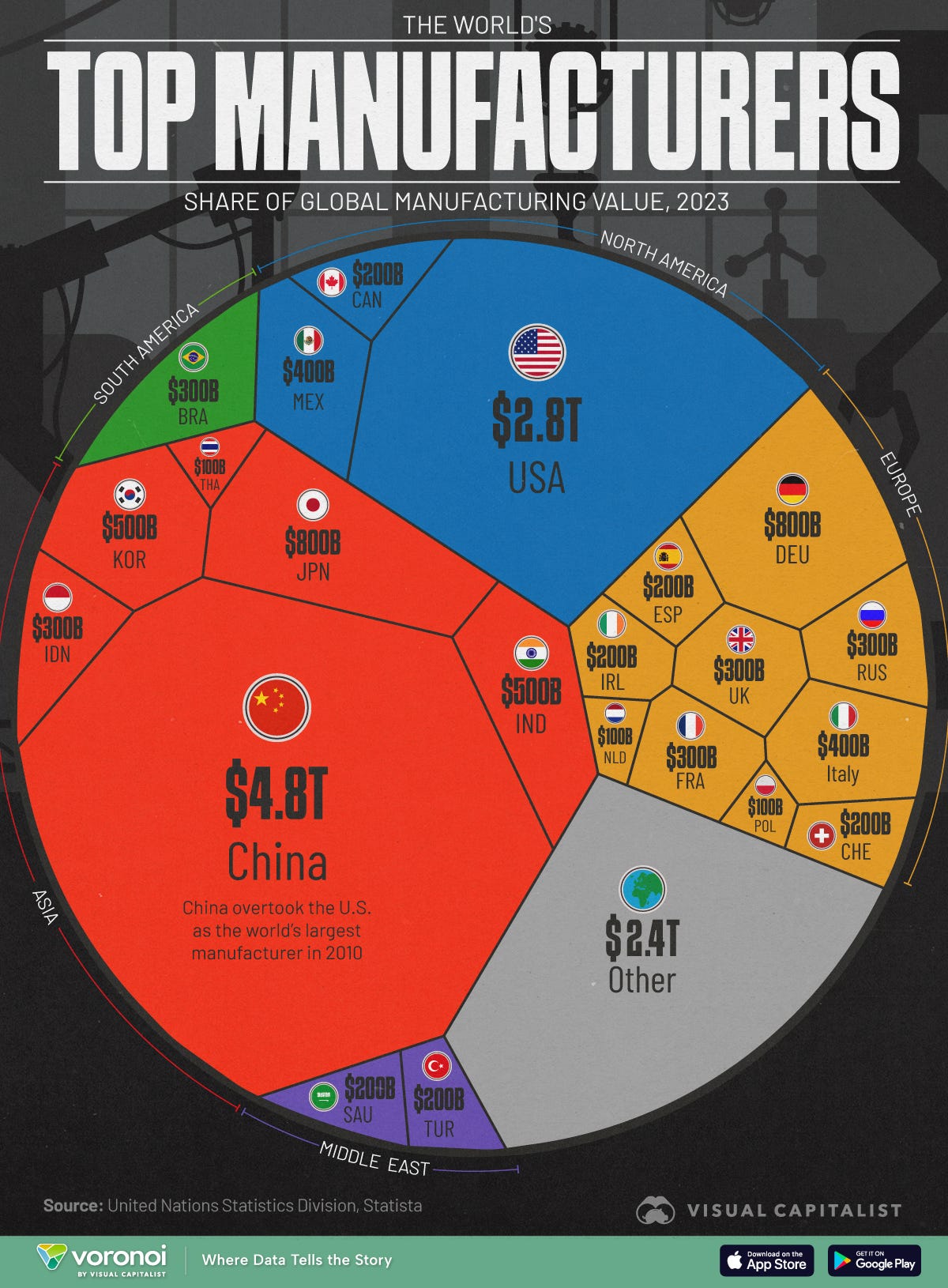

One Chart You Should Not Miss: World’s Top Country Manufacturers

One Term to Know: Real GDP Accounting

Gross Domestic Product (GDP) measures the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific period. Real GDP adjusts for inflation while nominal GDP does not.

GDP = C + G + I + NX

where

C = Consumption (public and private)

G= Government Spending

I = Investment (public and private [including change in inventories])

NX = Net Exports (Exports- Imports)

In Q125, the US contracted by 0.3% (quarterly annualized). You also noticed net exports was -4.83%, a big negative, while change in private inventories (+2.25%) boosted the real GDP, showing how tariffs have dramatically influenced the behaviour of the US consumers and businesses before the implementation of the tariffs.

The surge in imports may likely reflect the stock-up of inventories by businesses and residents buying more foreign imports (at the expense of domestically-made goods).

Note that the import value is a double-counting in consumption or investment. If a firm imports goods to beef up inventories, that value is already counted in investments. If a consumer buys foreign goods, that purchase is already counted in investments. Hence imports are subtracted from exports to avoid any double-counting. However, many may be mistaken that a surge in import reduces GDP while that just mean more consumption and or investment on the other side. The GDP accounting equation is a little misleading in that sense. (I corrected this explanation from an earlier version thanks to

.)

Given the tariff distortion on the Q1 GDP in the US, economists have referred to a line item called “final sales to domestic purchasers” to gauge the demand by its residents.

It is the sum of personal consumption expenditures, gross private fixed investment, government consumption expenditures and gross investment. In other words, it represents the total value of goods and services purchased by residents of a specific country, regardless of whether those goods and services were produced domestically or imported.

In Q1 25, growth in final sales to domestic purchasers was 2.3%, a decent number, but it has weakened from the average of 3% in 2024.

🌻Things I learned About AI/Productivity:

New ways to interact with information in AI Mode (Google)

AI Mode allows you to ask longer, more complex questions and explore further with follow-up questions and links to helpful content from across the web. And we’ve added updates, like new tappable and visual cards for products and places so you can take the next step, a new side panel on desktop to help you pick up where you left off and more.

21 Days Away from AI: What I Missed—and Why It Matters (

)Follow Cindy, a data scientist and quant researcher, in her journey crossing Climate, AI, and Finance!

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.