Weekly Good Reads: 5-1-1

Sticky Inflation, Tech Earnings and Margins, Fed's Pivot, Japan, Nvidia’s Jensen Huang's nuggets

Welcome to Weekly Good Reads 5-1-1 by Marianne O, a 25-year investment practitioner and the author of

on investing, economy, wellness, and something I learn about AI in an intuitive voice. All the Weeklies are here, and here is the index of charts and terms. You can easily subscribe to my newsletter by clicking below.Please also check out my conversations with Female Fund Managers, Investors, and more - new this year!

Feedback is important to me, so if you like the Weekly, please “heart” it, comment or share it with your contacts. Thank you so much for your support🙏.

Market and Data Comments

Global stocks powered ahead in the past week (S&P +2.7%, Nasdaq, 4.2%, and MSCI All-Country World, +2.6%), ending a 3-week losing streak.

Government bond yield in developed markets climbed slightly. Both the US stock and bond volatilities went down - the VIX (stock volatility) fell 3.68 percentage points to 15.03% while the MOVE (bond volatility) fell 6.86 points to 104.4.

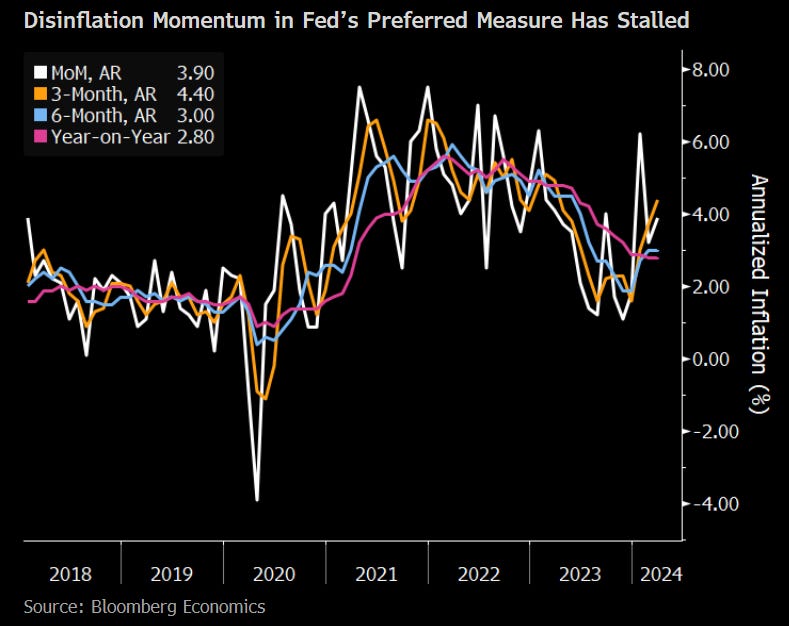

From the top chart, the US Q1 GDP came in at 1.6%, lower than the 2.1% projected due to lower inventories and net exports, but domestic final demand rose at a 3.1% clip (above 3% for three consecutive quarters), while the Q1 core PCE was surprisingly strong at 3.7% due to strong services inflation.

On Friday, the March core PCE price index, the Fed’s preferred inflation gauge, rose 0.3% m/m and 2.8% y/y, in line with expectation. The 3-month annualized core PCE is now at 4.4%, over 2x the Fed’s inflation target (see chart below). The March real consumer spending surprisingly jumped 0.5% m/m, indicating the underlying demand strength of the US economy.

by reminded us “Sticky is Not Stuck: Inflation.”

The University of Michigan Consumer Confidence dropped from 77.9 in early April to 77.2 in late April, with long-term inflation expectations rising to 3%, reflecting increasing economic uncertainty.

Market participants were humbled by the macro signals that provided different vibes this week, while earnings, especially tech, continued to push higher. Reason: Strong EPS growth of information technology; also market analysts expect the net profit margins of the tech sector to reach a high of 27.7% (blue line) by the end of 2024, over 2x that of the S&P 500 index of 13.2% (orange line, see chart below.)

The market expects a delay in rate cuts, with only a 35% chance of a first cut in July (from a 48% chance a week ago). Economists and investors are also expecting a more hawkish Fed tone in the FOMC meeting next week (see a Fed’s Pivot below), with a big hint coming from Chicago Fed President Goolsbee, the FOMC’s most dovish member, who noted “progress on inflation has stalled” and the Fed will have to “recalibrate”. So, higher for longer, it will be.

Elsewhere, Europe’s April composite PMI painted a picture of recovery, and Europe is on a surer path to disinflation, with Q1 GDP expected to be positive at 0.1% y/y, led by consumption, ending 18 months of stagnation, while April inflation (next week) is expected to be around 2.6% y/y.

The Bank of Japan cautiously kept its interest rate policy the same albeit signalled rate hikes this year as core inflation should again hit the 2% target. The Yen has continued to depreciate against the USD (-11% YTD) given no interest hike in Japan and the likely delay in interest cuts in the US although the weaker Yen has boosted Japanese stocks.

This coming week, we will monitor the US April ISM manufacturing and the FOMC interest rate decision and Powell’s Press Conference on Wednesday, the April nonfarm payrolls, unemployment rate, and average hourly earnings on Friday, the Euro Area Q1 preliminary q/q GDP on Tuesday, the Euro Area April manufacturing PMI on Thursday, and China’s April NBS manufacturing and Caixin manufacturing PMI on Tuesday.

Economy and Investments (Links):

Why the Stock Market is Disappearing (The Economist or via Archive)

He [JP Morgan’s CEO Jamie Dimon] identifies demand for environmental, social and governance reporting and the pressure of quarterly earnings reports as part of the trend’s explanation. But for the most part, the disappearing stockmarket is a side-effect of something more positive for company founders: they simply have more options..If founders do not want to go public, they now face less pressure to do so. There are plenty of funds that are willing to invest in them regardless.~THe Economist

The Origins of the 2 Percent Inflation Target (Richmond Fed)

Industrial Metal Prices Jump as Investors Bet on Rising China Demand (FT)

An index tracking the performance of six industrial metals on the London Metal Exchange has climbed 8 per cent since the start of 2024, outpacing a 6.3 per cent rise for MSCI’s index of worldwide stocks.

The index, which also includes lead, aluminium, tin and nickel, has risen sharply this month as investors grow more confident that an extended period of high global interest rates, intended to curb inflation, will not choke off economic growth. At the same time, analysts have raised concerns that production snags from miners will constrain supplies. ~FT

Finance/Wealth (Link):

The News is Making You Miserable (A Wealth of Common Sense)

A recent study looked at more than 370 million stories on the Internet to determine how negative language can impact news consumption. Lo and behold, the more negative the headline, the more likely people are to click on the story, regardless of what the story is about.

You don’t even have to sit through an entire story to be mad now. You can just read a headline or see a screengrab.

Negativity drives eyeballs.

~ A Wealth of Common Sense

To counter this, go outside, enjoy nature, read a book or watch a movie, chat with friends and families in person, and exercise.

Wellness/Idea (Link)

Generation Z is Unprecedentedly Rich (The Economist)

+ Love For Food: Hunger For Change (Chris Westlake on Tableau Public)

One Chart You Should Not Miss: The Soft Power of Japan

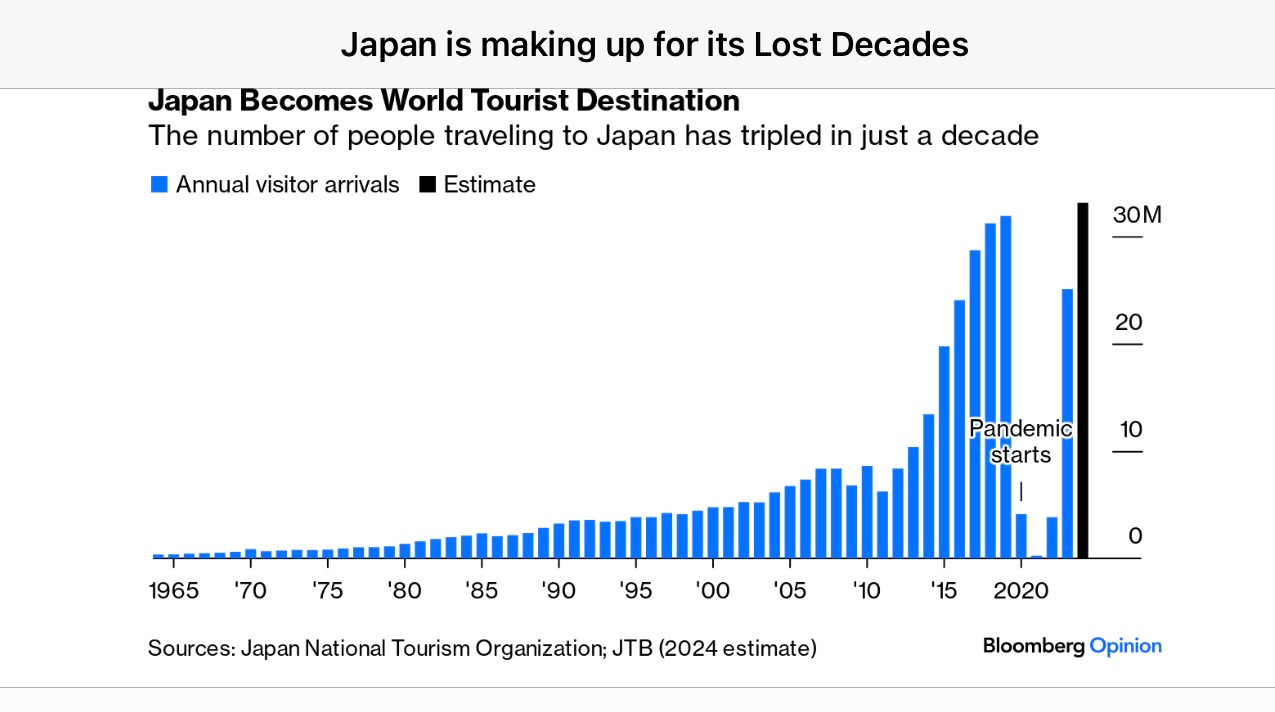

According to Bloomberg, tourism is “perhaps Japan’s greatest economic success story of the past 30 years.” In March, a record 3.1 million tourists visited Japan during cherry blossom season, reflecting the country’s strong position on the global stage, no doubt helped by the weak Yen.

More evidence of Japan’s come-back and revitalization from its “lost [3] decades” and deflation: the stock market roared back in 2023-2024 and exceeded its 1990’s peak this year; global diplomacy is flourishing, corporate’s return-on-equity has been rising, and of course, its pop and food culture have never ceased their popularity. The Japanese anime market alone is worth about $30 billion and may double in the next decade (Bloomberg).

One Term To Know: A Fed Pivot

A Fed Pivot refers to the US Central Bank reversing its policy stance and outlook and switching course from an expansionary (loosening) to contractionary (tightening) monetary policy, or vice-versa.

The Fed has a dual mandate of maintaining stable inflation and full employment. When the economic fundamentals change (e.g. the economy slows down or overheats), a change in the Fed’s existing monetary policy (change in interest rate and/or quantitative easing/tightening) is warranted.

A change in the monetary policy is pervasive, affecting businesses and government forecasts, but the change always works with a lag, so the effect on the economy can be felt several months away.

The Fed needs to communicate a change in its monetary stance so as not to jerk the market into overreaction.

A Fed Pivot can also refer to the Fed signalling or talking about changing monetary policy directions, but without taking any actions. Bloomberg found in December last year by analyzing 60,000 headlines, Fed Chairman Powell delivered a major (dovish) pivot. “By hinting at a swifter shift toward rate cuts, he gave markets a boost and helped the economy dodge a downturn.” Now, with the disappointing first 3 months of inflation data, the Fed may have to pivot again.

The Fed often deliberates how long they need to maintain existing monetary policy so financial conditions are not too loose or too tight for too long.

’s latest piece discussed in detail how the Fed “pivoted” its views towards the future monetary path.

See the chart below for how the Fed enacted a series of rate cuts or rate hikes to counter the changing economic conditions. The grey bars indicate US recessions.

[🌻New] One Thing I Learn About AI:

At the Stripe Sessions Global Internet Economy 2024 Conference this past week, Patrick Collison, Stripe’s co-founder asked Jensen Huang, CEO of Nvidia what he thought of the future of AI, and here’s what he said, amongst the 20+ other nuggets he shared (will be in another post):

If your company is not engaging AI aggressively, you are doing something wrong. You company will go out of business because another company is going to use AI.

As the marginal cost of intelligence is practically zero, there are a lot of things you could do you would not have done otherwise.

I ask Perplexity AI lots of questions every day.

~Jensen Huang, CEO, Nvidia

Please do not hesitate to get in touch if you have any questions!

Also please check out my latest Conversations with Investment Changemaker

below.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

Fun read and good insight on the US economy.

How persistent do you think this recent bout of inflation is going to last?