Weekly Good Reads: 5-1-1

Soft-landing data, Record high in stocks, Chinese growth measures, Lucky vs. Repeatable, ERP, Value-At-Risk

Welcome to Weekly Good Reads 5-1-1 by Marianne O, a 25-year investment practitioner and the author of

on investing, economy, wellness, and something new I learn in AI/productivity. All the Weeklies are here, and here is the index of charts and terms. You can easily subscribe to my newsletter by clicking below.Please also check out my conversations with Female Fund Managers, Investors, and more - new this year!

Feedback is important to me, so if you like the Weekly, please “heart” it, comment or share it with your contacts. Thank you so much for your support🙏.

Market and Data Comments

Data-obsessed markets and central bankers breathed a sigh of relief as the US April headline CPI (+3.4% yoy, 3.5% prior) and core CPI (+3.6% yoy, 3.8% prior) were softer than expected, with the first sign of housing rents disinflation albeit insurance and other services categories still see a strong inflationary impulse.

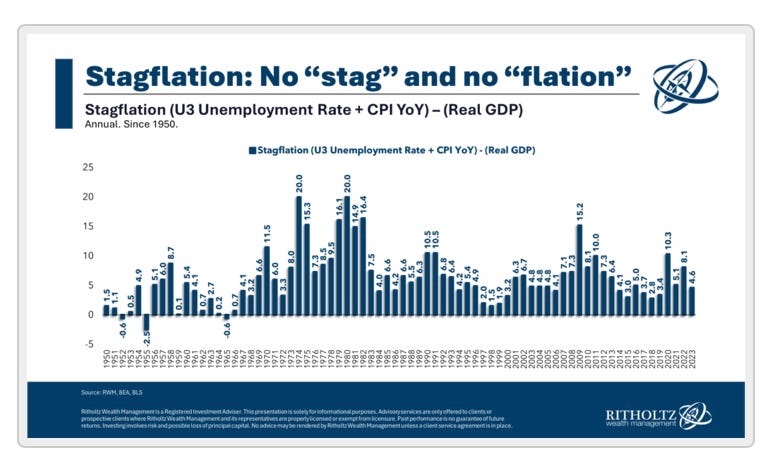

Recent softer CPI and PPI data signal a softer core PCE in April (due May 31) just as stagflation talk resurfaced.

The chart above by The Big Picture plots a simple stagflation indicator based on Unemployment (U3) + CPI Inflation (yoy) – Real GDP (see Econ/Invest #3). With 10 as a “benchmark”, the current number of 4.6 is nowhere near the stagflation seen in the 1970s, early 1980s and 1990s, and a brief period in 2020.

With the US April retail sales coming in weaker than expected and industrial production going sideways, a soft landing appears in place.

Global stock markets cheered and ended up around 1.5 to 2.1% higher while the US 10y government bond yield fell 8bp and the MOVE (bond volatility) index dropped almost 5 points.

14 out of the major 20 global stock markets from the US, Japan, Brazil, the U.K., Canada, and Australia hit a recent high (Brazil to Australia are helped by commodities rally), as did the less-tech-weighted Dow Jones, which passed 40,000 points this week.

Europe’s recent economic data also pointed to GDP and employment recovery. The ECB and the Bank of England continue to see a disinflation trend in their economies and expect the first interest rate cut in June.

China reported stronger-than-expected April industrial production and export growth ( a deliberate focus by the government on the manufacturing industry to revive the economy), in contrast to the weak domestic demand and housing data. All but one city out of 70 in China reported lower home prices in April. However, trade tensions with the US and likely the EU present ongoing challenges for China.

The good news is that several local governments in China started to address excess housing inventory by purchasing unsold properties at a discount and converting them into affordable housing. The government also announced lower down-payment requirements for home buyers and eliminated the national mortgage rate floor. The main Chinese benchmark CSI 300 Index doubled the performance of the S&P 500 from its low on Feb 2 till May 17, rising about 16% compared to the S&P’s 7.4%.

’s latest piece and his unique view on China’s recent measures are worth reading.But wait, something else doubled the performance of CSI 300 during this period, and it’s copper, which rose 32.6%, fuelled by supply disruptions and an increasingly supportive macroeconomic backdrop!

This coming week, we will monitor the G7 chiefs and central bankers’ talks on the global economy, the May FOMC minutes and UK April inflation rate on Wednesday, the Euro Area and UK May preliminary composite PMI on Thursday as well as Japan’s April CPI on Friday.

Economy and Investments (Links):

From Tokyo to New York, Stock Markets Are on a Record-Hitting Spree Around the World (Bloomberg or via Archive)

The S&P 500 has set 24 new all-time highs in 2024 after going two years without one, as US stocks have been on a $12 trillion rally since late October. One part of that is hopes for a soft landing with the economy staying strong while inflation cools, which is spurring bets the Federal Reserve will ease monetary policy as soon as later this year…Another part is enthusiasm for artificial intelligence technology…Another part is enthusiasm for artificial intelligence technology.~ Bloomberg

What Xi Jinping Gets Wrong About the Chinese Economy (The Economist or via Archive)

What Stagflation? (The Big Picture)

+ In This Economy Book - The Why and How (

)We know that writing a book is no small feat, let alone an Economics book on what really matters in money and markets. It is “An illustrated guide to the mad math and terrible terminology of economics, from one of the internet’s favourite financial educators.” Congratulations, Kyla!

Finance/Wealth (Link):

Lucky Against Repeatable (Morgan Housel, Collab Fund)

After the dot-com crash], the lesson people learned from that was not, “I should never speculate on overvalued financial assets.” The lesson they learned was, “I should never speculate on internet stocks.” And so the same people who lost 90% or more of their money day-trading internet stocks ended up flipping homes in the mid 2000s, and getting wiped out doing that. It’s dangerous to learn narrow lessons.

The great thing when you ask, “is this repeatable?” is that you start to focus on things that you and I – ordinary lay people – have a chance of repeating ourselves.

Wellness/Idea (Link)

The Food that Protects Diabetes and Health Health (second article, Arnold Pump Club)

Research suggests that fiber could be one of the best things to eat to protect your body from heart disease, diabetes, and other health conditions….However, only about 4 percent of men and 12 percent of women eat enough fiber per day. The average person consumes about 15 grams of fiber daily, and you want to aim for 30 to 35 grams each day.

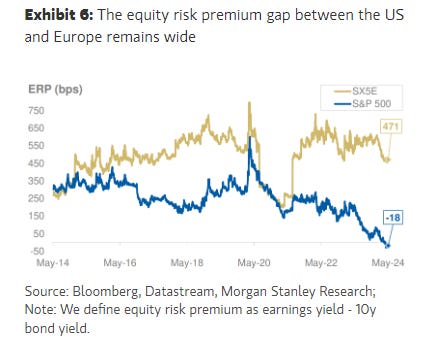

One Chart You Should Not Miss: Equity Risk Premium between the US and European Stocks

The equity risk premium (ERP) is what an investor expects to earn from stocks over a risk-free bond (proxied by a 10-year government bond). As stocks are generally riskier than bonds (as measured by higher volatility), investors need more compensation/ reward to hold stocks versus bonds. The higher the ERP, the more attractive is stocks over risk-free bonds.

In the chart below, Morgan Stanley measures the ERP as the earnings yield of an index (the inverse of the P/E ratio) minus the yield of the 10-year Government Bond.

The S&P 500’s ERP (as defined by Morgan Stanley) has been trending lower, now at -18bp, while that of the Euro Stoxx 50 (Europe) index is about 470bp. This gap between the US and European ERP is historically wide, as the info-tech heavy S&P 500 has a much higher multiple than the European index which has more weight in energy, consumer sectors, and industrials, trading in lower multiples.

One Term To Know: Value At Risk

JP Morgan developed and popularized value-at-risk (VaR) in the early 1990s to measure financial risk. It has been widely used by financial institutions like banks and investment companies, corporations, regulators, risk management professionals, and academics.

VaR measures how much money you may lose from your portfolio on a “bad day” - it specifically tells you the most you may lose in a specific period (e.g. a day/week/month) with a certain level of confidence.

For example, you have $10,000 in your portfolio and the VaR is $1,000 at a 95% confidence level for one day. That means there is a 95% chance you won’t lose more than $1,000 from your portfolio in one day, but there is a small chance (5%) of losing more than $1,000.

While the measure is relatively easy to quantify and interpret and is a popular way for organizations to identify potential losses for risk-taking and capital allocation, two key disadvantages are (1) VaR assumes that securities returns are normally distributed, which often is not the case in reality (2) VaR does not quantify the extreme losses beyond the VaR threshold, which means the potential losses can be underestimated during severe events.

Other risk measures such as Conditional Value-at-Risk (CVaR) calculate the expected loss if the above threshold is crossed. CVaR quantifies the amount of tail risk a portfolio has. CVaR and VaR can be used together for risk measurement.

[🌻] One Thing I Learn About AI:

The world will begin to see “AI Overviews” in Google Chrome so Google Search will answer our queries with a paragraph or two written by generative AI including the reference links. However, Axios argued, “this system still relies on web-based information, but it doesn't nourish the creators of that information with users' visits.”

This will likely hurt publishers and retailers’ referral traffic, make humans less likely to contribute to the web’s collective pool of knowledge and make information discovery less dynamic, timely, and interesting.

My take: I have joined the beta for over 6 months and have liked the AI summaries with supported URLs very much as they speed up my information search by 2x. I especially like the related questions that Google provided, leading to a more comprehensive appreciation of the problem I am trying to solve. Saving time in search allows humans to be more creative and strategic in other areas, so this is a good thing.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more!

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

Some interesting charts this week