Weekly Good Reads

SaaSmageddon, Crypto Winter, New Technology Spending, Rare Earths, Anthropic, Matcha Latte

Welcome to Weekly Good Reads. As a 25-year investment practitioner, I aim to share insights and topical perspectives on investing, the economy, and AI/productivity. I will sometimes write essays on investing, have conversations with great (female) investors, and provide leisurely thought pieces on wellness.

Thank you for supporting my work. Please hit the 💛 button or share with others if you like what you read.

Sharing the quote of the week:

The critical thinking skills are going to be really important... Learning to be critical about the information you see. Now that AI systems can generate very, very plausible explanations, very plausible images, very plausible videos.

~ Dario Amodei (Anthropic Founder and CEO)

Weekly archives | Investing | Ideas | Index of charts and terms | Conversations with Investment Managers

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Please take a look at R4A, a complete investment solution online, for free.

Market and Data Comment

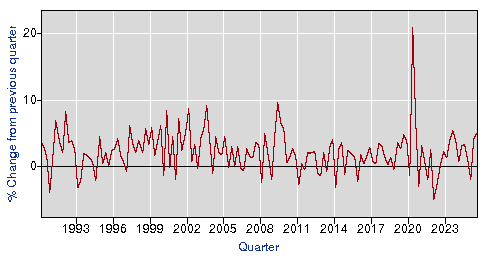

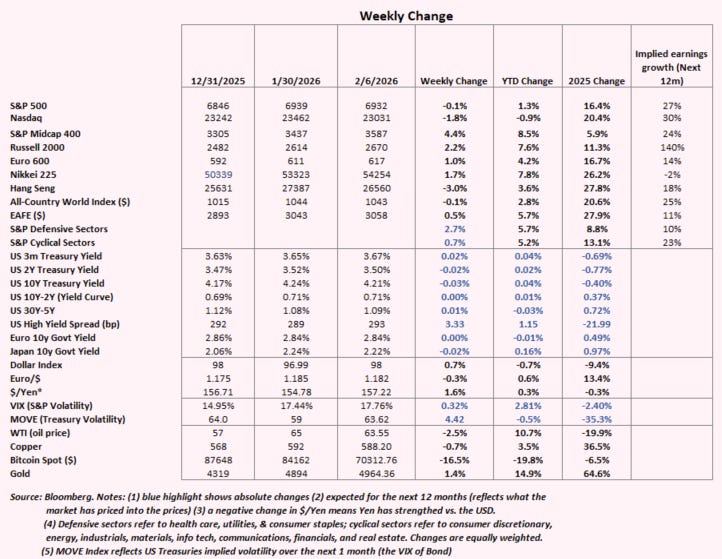

Up till the end of last year, investors have been focusing on AI winners such as Nvidia and other chip companies (the picks and shovels) and energy and materials producers, but last week saw the true carnage from AI disruption. The Software ETF (IGV) dropped 12% before rebounding on Friday to end -8.7% for the week. Other software companies like Thompson Reuters and Morningstar fell 20% and 18%, while Salesforce dropped ~10% and Service Now, ~14% (see Econ/Invest #1).

Since the end of 2023, IGV on average rose less than 1% per annum while SMH (Vanguard semiconductor ETF) rose an annualized 49% (see below chart).

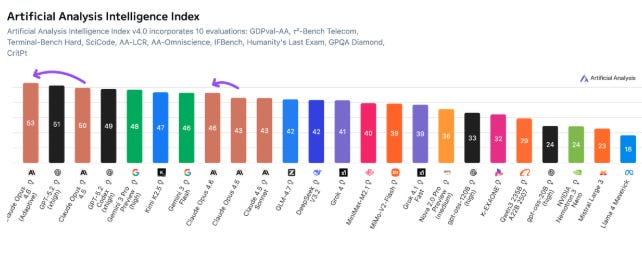

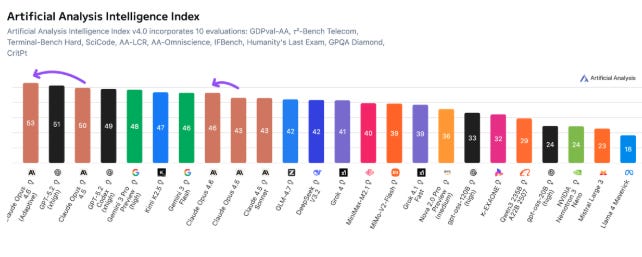

The latest catalyst of the software selloff was Anthropic, which on February 5 released Claude Opus 4.6, designed to automate work tasks from legal, data services, to financial research. This latest model tops the Artificial Analysis Intelligence index—Opus 4.6 outperforms the industry’s next-best model (OpenAI’s GPT-5.2) by around 144 Elo points, and its own predecessor (Claude Opus 4.5) by 190 points, according to Anthropic. Earlier on Tuesday Anthropic announced a legal plug-in tool that allows attorneys to more effectively review contracts and manage compliance workflows.

How does AI tools hurt software companies? Software-as-a-service (SaaS) companies typically license their platform tool to users for a fee to automate certain business functions and connect data points, streamlining business workflow and generate reports. The new AI tools automate some of these workflows and remove the need for human, or the need for a platform to perform these tasks.

Nevertheless, AI tools will need software products and improve them, not replace them, as Nvidia’s CEO Jensen Huang said, and the software selloff makes the stocks much more attractive when their earning projections have been going up, rising from 16% a few months ago to 19% for 2026 (Bloomberg Intelligence). Goldman Sachs software basket forward P/E has slumped from about 100 in early 2022 to 15 currently. The article from a16z argues that we need more software, not less (see the bottom section).

The question in investors’ mind is: will productivity growth justify all the AI spending, which will go up around 60% in 2026 to close to $700 billion just among Alphabet, Meta, Amazon, and Microsoft. Amazon will see negative free cash flow in 2026 and Meta in 2027.

As Barclays research pointed out, productivity growth is good for economic policy—less worry by governments on the debt dynamics, growth with less inflationary pressures, and a boost to potential GDP growth. In fact, this is what the Fed Chair nominee, Kevin Warsh, has argued for—lower rates based on productivity gain from AI spending without the need to borrow on the Fed’s balance sheet.

Since COVID-19, US corporate productivity has indeed been on the rise (above the long-term average of 2%) after the huge swing in the COVID years. Alphabet has seen signals on return from Google Cloud, Google search, and YouTube while Amazon’s CEO recently said that growth at Amazon Web Services was “the fastest we’ve seen in 13 quarters.”

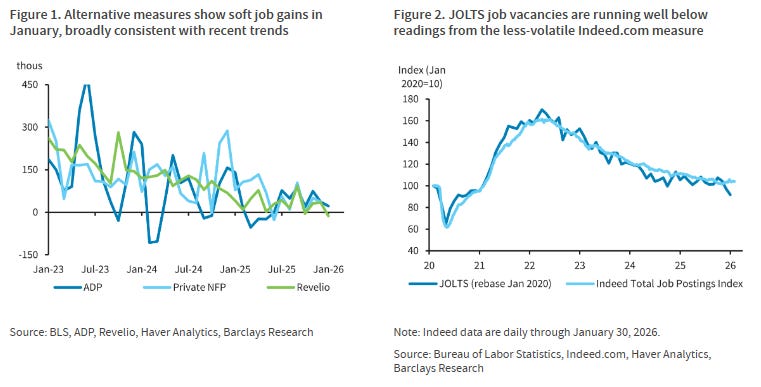

Still, investors have shown to scrutinize much more on winners vs. losers in this AI trade and will need to see ROI from the AI spend. Productivity growth will be even more important now as the US is facing more labour supply constraint resulting from ageing population, lower immigration, and more restricted international trade and supply chains. The latest JOLTs job vacancies estimates of 6.5 million (a decline of 400k in December after -500k in November) are the lowest since early 2020, representing 0.87 vacancy per unemployed worker. Yet, other soft data like the January ISM manufacturing PMI of 52.6 (+4.7 points from December) is showing growth recovery.

A couple of interesting market charts worth a mention.

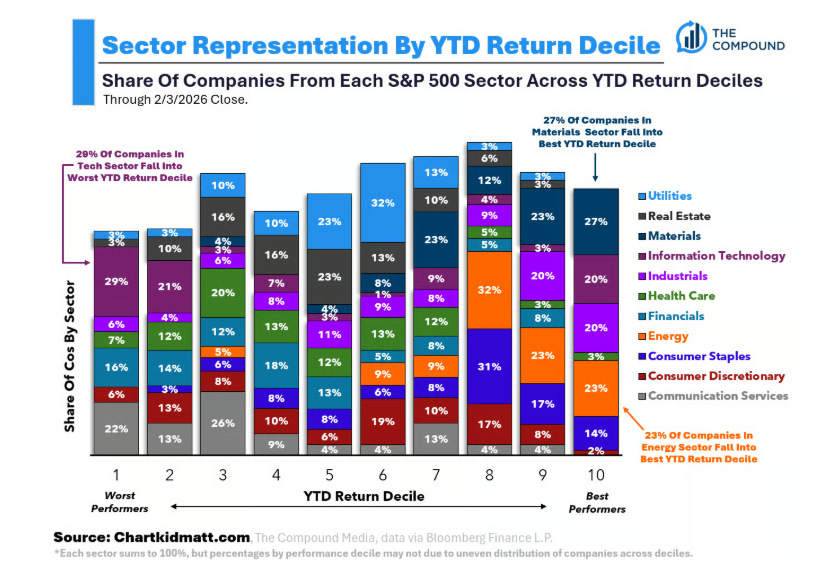

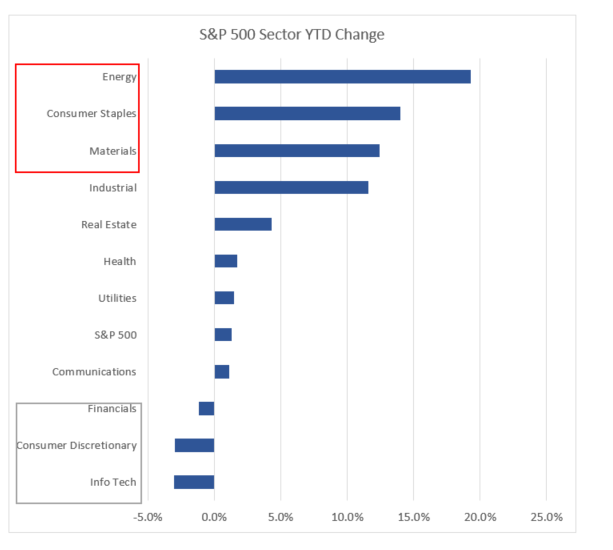

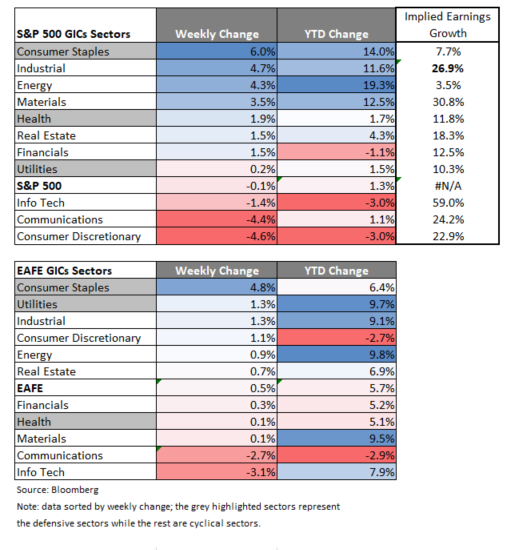

The following is a chart showing the YTD return (data through 2/3/26) by Chart Kid Matt of each of the 11 S&P 500 GICs sectors. The takeaway:

…companies within the Energy, Materials, Staples, and Industrials sectors are crushing it while companies in Comm Services and Financials are lagging. Tech is mostly bad (50% of companies are either in the worst or second to worst decile of YTD performance).~Chart Kid Matt

So the traditional sectors in the economy continue to do well despite the mayhem in software, communication services, and financials, representing an ongoing rotation trade away (marginally) from Big Tech. YTD, S&P 500 is still up 1.3%.

Crypto investors have also been facing its worst “winter” with bitcoin dropping ~50% from its October 2025 peak, coincidentally as software stocks collapsed ~32% from its September 2025 peak. Sometimes called “digital gold” or “digital cash”, crypto currencies have failed to be the hedge during times of geopolitical uncertainty and are now more correlated with software (internet stocks) than with the overall Nasdaq index. Quantum computing is believed to be able to crack cryptography. Coupled with deleveraging (Yen carry trade unwinding due to rising Japanese bond yields and a potential Yen intervention) and bullish investors like Strategy not being to add more to positions, bitcoin winter has gotten worse (see more on Econ/Invest #2).

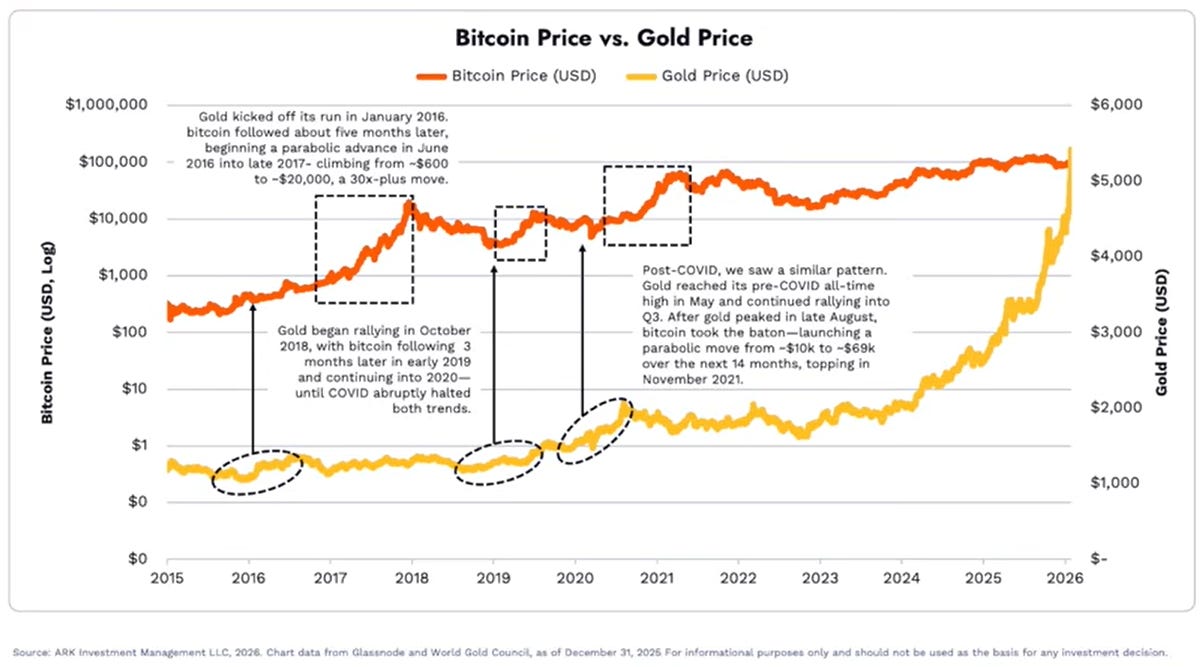

However, Cathie Wood from Ark Invest recently argued that bitcoin’s parabolic rise has traditionally followed that of gold (see below chart). The fact that gold and silver have stabilized after the recent rout may help.

At the time of writing, Asian stocks rose strongly on the back of Japan’s prime minister Takaichi’s LDP Party’s overwhelming election win, which adds near-term stability to governing, and a rise in large caps especially semiconductors and defense stocks. Bond and currency also remain stable after the win, and many strategists now believe the LDP government may act less urgently on fiscal stimulus.

This coming week, we will monitor several Fed governors speech (Waller, Bostic, Miran, Logan), January retail sales on February 10, the January nonfarm payrolls, average hourly earnings, and unemployment rate on February 11, and the January CPI on February 13, and China’s TSF, and the January PPI and CPI on February 11. The UK Prime Minister’s position also hangs on a thread after further exposure of Mandelson’s (his former political ally and ambassador to the US) Epstein link. Note the earnings from US consumer-spending sensitive companies including Walmart, Disney, Coca-Cola, AirBnB, and MacDonald this week.

Economy and Investments (Links)

Big Tech’s ‘Breathtaking’ $660bn Spending Spree Reignites AI Bubble Fears (FT or Archive)

Higher capex “telegraphs that it may take longer for AI strategies to play out”, said Dec Mullarkey, managing director of $300bn asset manager SLC Management. “Not welcome news for investors that are already fixated on when AI-related revenue will start to show up.”

Related: When Will the “Software Smash” End? (Milk Road Macro)

Bitcoin Drops Below $61,000, Wiping Out Gain Since Trump’s Win (Bloomberg)

The latest drop comes as digital assets face continued doubts about their real-world use, as well. Once touted as an inflation hedge or a rival to gold or the US dollar as a stable store of value, Bitcoin has continued to trade more like a high-risk asset and has failed to serve as a haven during times of financial market stress. In fact, its growing presence in institutional portfolios has at times made it more vulnerable to broad de-risking, particularly during bouts of volatility in tech equities and precious metals, like what has been seen in recent weeks.

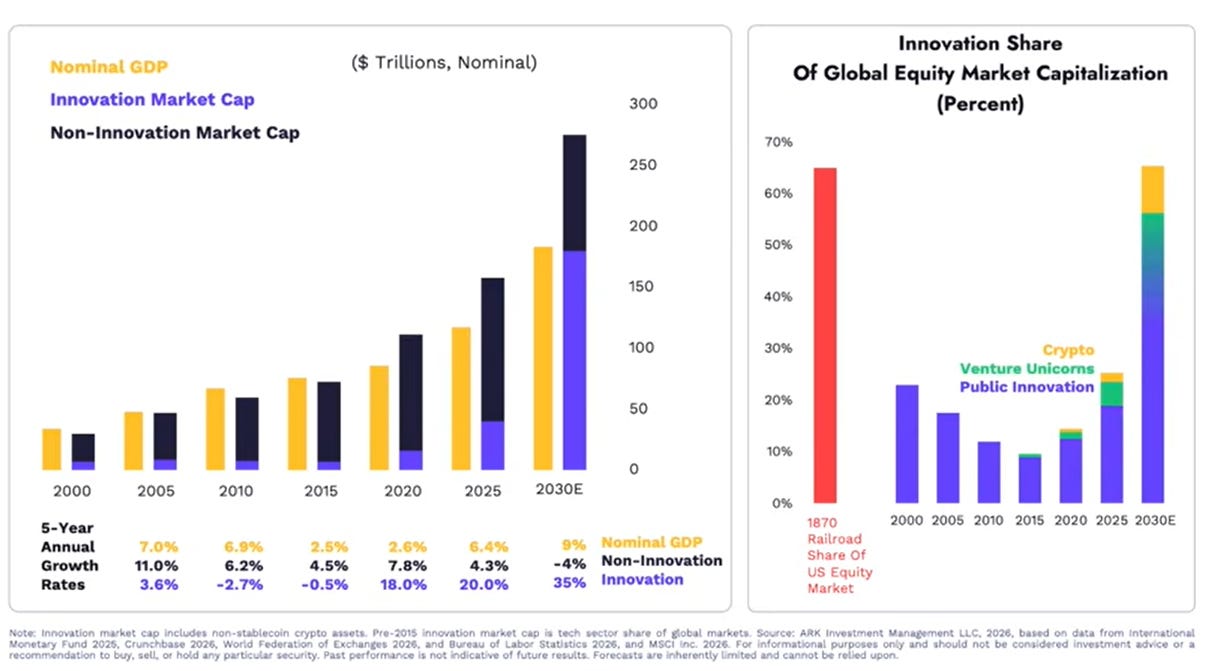

Big Ideas Report (2026) (Ark Invest and ETF Express)

A central theme of this year’s report is acceleration. ARK Invest writes that advances in artificial intelligence now extend far beyond software, reshaping physical systems, scientific discovery, capital formation, and productivity across the economy.

From AI-native biology transforming healthcare, to intelligent machines redefining labour, to digital networks re-architecting financial infrastructure, ARK writes that its research highlights how innovation is scaling faster and interacting more deeply than ever before.

Drawing on research across both public and private markets, Big Ideas 2026 reflects how innovation often develops long before it is fully visible in traditional benchmarks. The report is intended for a global audience of investors, business leaders, policymakers, and anyone seeking a clearer view of where innovation is heading next.

Wealth and Wellness (Link):

Wealth

The Stock Market Just Got Shaky. Where to Find Solid Ground (WSJ)

If you hold a low-volatility fund (or your own basket of boring stocks), you’re likely to outperform the S&P 500 in the short run whenever the market stumbles.

In the long run, you’ll probably fall behind whenever most investors want exciting stocks instead—and you would better be prepared for those periods to last for years. In the very, very long run, however, boring stocks might well come out ahead.

And so will you, if you can stick with them when they’re a lot more boring than they happen to be right now.

Wellness

Is a Matcha Latte Better For You Than a Builder’s Brew? (The Economist or Archive)

One striking paper was published in Molecules in 2019. Its authors analysed data on 3,349 individuals aged 50 and up. After adjusting for smoking, coffee consumption and other variables, they found that those who drank green tea scored higher than black-tea drinkers on a “successful ageing” health index that assigned scores for such things as body weight, health and levels of physical and social activity.

One reason for this might be their respective L-theanine content. Green tea contains nearly 28% more per cup than black tea does, a study found in 2016. In addition to promoting soothing brain chemicals, L-theanine has been shown by recordings of brain activity to amplify alpha brain waves—electrical oscillations that seem to sharpen mental focus without causing jitters

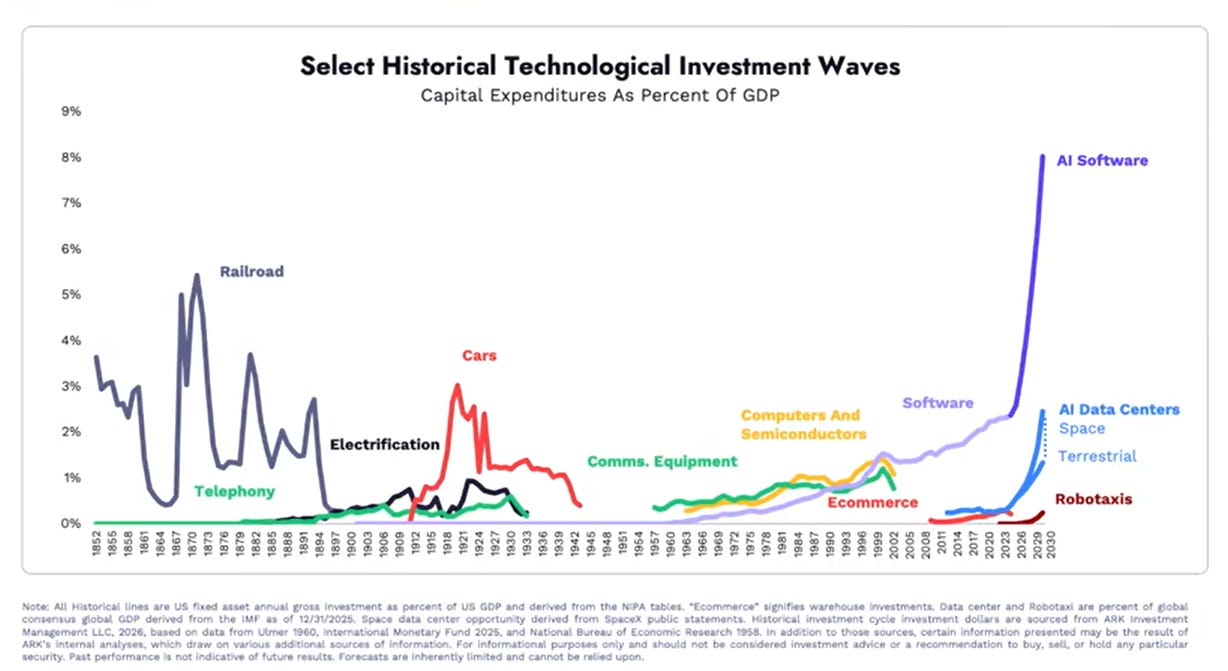

One Chart You Should Not Miss: Growth Rates and Spending of New Technology

“The fibre (referring to the telecom companies’ overspending in the 90’s and 2000’s) went dark, but the GPUs are alive”, said Cathie Wood (YouTube). According to her, we are at the beginning of the AI revolution, and the AI spending cycle will be much longer than the telecom era. Disruptive technologies is expected to grow to dominate global markets, as her charts from the Big Ideas 2026 report show.

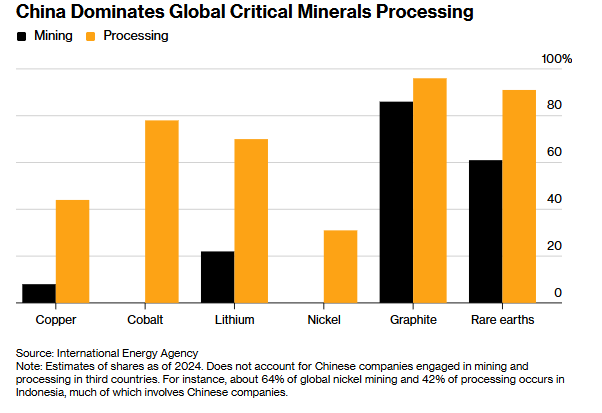

One Term to Know: Rare Earths

Rare Earths, in FT words, have become the plaything of the US-China trade war.

In 2025, rare earths have come to symbolise the global battle over critical minerals like never before — and become shorthand for the way in which the West is scrambling to compete with China’s dominance in supply chains.~FT

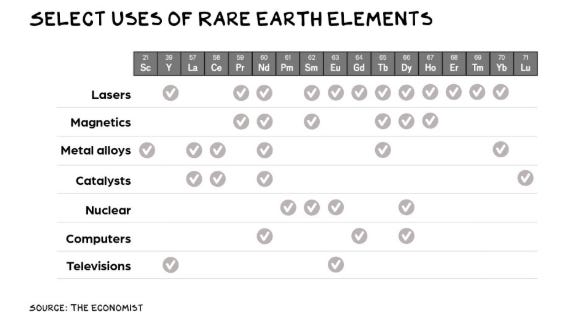

Rare earth elements (REEs) are a group of 17 metallic elements with unique magnetic and electronic properties that make them critical to modern technology—from permanent magnets in electric vehicle (EV) motors and wind turbines to precision electronics in smartphones and defence systems.

Although the raw rare earth metals market is relatively small compared with other commodities, it has been growing rapidly: one forecast put the global REE market at around $8.1 billion in 2024 and projected to reach about $15.8 billion by 2030 (~12 % CAGR). Other analysts see a broader rare earth metals market expanding from roughly $19 billion in 2025 to over $36 billion by 2034 (~7.6 % CAGR), reflecting the increasing deployment of clean-energy and high-tech systems. This growth is underpinned by soaring demand; e.g., magnetic rare earth demand tied to EVs and wind power is projected to triple by 2035.

On the supply side, China is the dominant player in both mining and processing of rare earths. China accounts for roughly 70% of global rare earth mining and more than 85–90% of refining capacity, giving it strategic leverage over global supply chains. Other countries with noteworthy production include the US, Myanmar, and Australia, but their output and processing infrastructure remain far smaller than China’s. This concentration has geopolitical ramifications: export controls, trade tensions, and efforts by the US, Japan, Europe and other economies to diversify supply are becoming regular headlines as governments try to mitigate supply risks and build resilient industrial ecosystems.

For investors, rare earths matter because they are fundamental building blocks of the future economy. The shift to electrification of transport, expansion of renewable energy capacity, and proliferation of advanced electronics all depend on materials like neodymium, dysprosium, and praseodymium. This multi-decade demand trajectory, combined with persistent supply concentration and geopolitical risk, means rare earths sit at the intersection of technology, industrial strategy and national security. Understanding these dynamics helps investors see where growth bottlenecks and supply vulnerabilities could shape global markets.

🪷Things I learned About AI/Productivity

Anthropic Releases New Model That’s Adept at Financial Research (Bloomberg)

The company on Thursday unveiled Claude Opus 4.6, which it says can scrutinize company data, regulatory filings and market information to come up with detailed financial analyses that would normally take a person days to complete. Opus 4.6 is also meant to be better at a range of other work-related functions, including making spreadsheets and presentations, as well as software development.

Related: Claude Opus 4.6 takes first place in the full Artificial Analysis Intelligence Index (Artificial Analysis)

2026.06: SaaSmageddon and the Super Bowl (Stratechery)

Building on that Microsoft article, Ben and I discussed the future of Saas companies on this week’s Sharp Tech, including a more than half-trillion dollar collapse of the Nasdaq 100 this week. Is the market’s skepticism fair? We dive into why software companies have more moats than their skeptics acknowledge, but nevertheless face a variety of headwinds that are likely to spur painful corrections to the valuation of these companies, consolidation, and substantial layoffs.

My Favourite Read/Listen on Substack this Week

Thanks for reading!

Please do not hesitate to contact me if you have any questions, and check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please 👍and share it with your friends, or subscribe to my newsletter🤝.

A thoughtful and data-rich snapshot of how AI-driven productivity gains are reshaping markets, challenging software business models, and forcing investors to re-evaluate where real value creation will emerge next

The thesis of AI's negative impact on software is not new, as you show in the chart of relative performance since 2023. Although growth rate has been fine in the near term, I wonder if there will be more of a divergence in the future. Enterprises / businesses still need software but the marginal cost of software production (due to their AI brain) is no longer close to zero, also pricing power and potential to increase revenue per customer are quite different from software to software.