Weekly Good Reads

Weak US Jobs, Cross-Market Long Bond Yield, Asset Manager's AI, McWages Index, Peak Gold Price, "Naikan" Questions

Welcome to a new Weekly Good Reads by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work! Please hit the 💛 button or share with others if you like it.

Sharing the quote of the week:

He who chases two hares catches neither.

~ Desiderius Erasmus

Weekly archives | Investing | Ideas | Index of charts and terms | Conversations with Investment Managers

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Please use R4A, our firm’s investment toolkit online, for free!

Market and Data Comment

Continuous weak US jobs data confirm a September Fed rate cut

Divergent trends in developed market bond markets reveal debt vulnerabilities

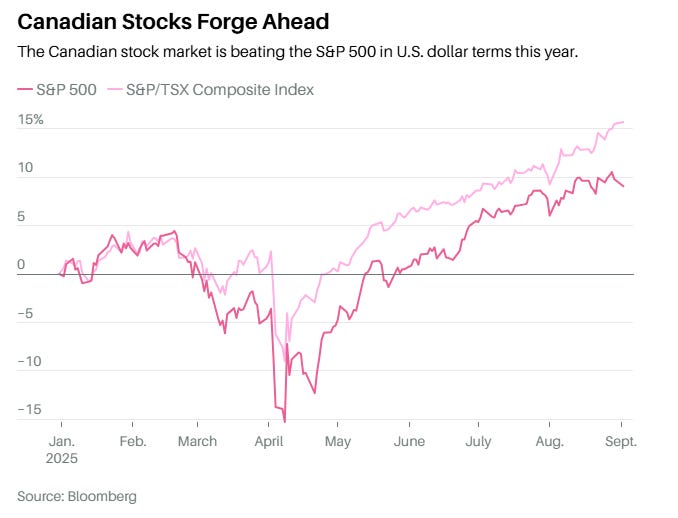

A quick review of the Canadian stock market trend

The economic data this past week has been bad news for the Trump government:

US job openings fell to 7.18 million, the lowest since 2021

The Fed Beige Book shows “nearly all districts showed tariff-induced price increases”, thus weakening consumer demand

The August manufacturing PMI (48.7) is contractionary for 6 straight months, although the services PMI (52) continues to expand

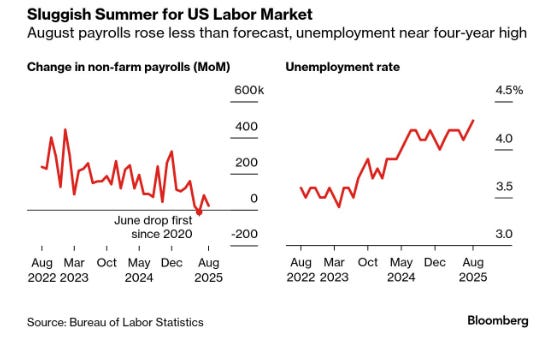

The biggest hit was another weak August jobs report, which saw a 22k increase in jobs and a revised negative job growth in June.

The August unemployment rate inched up to 4.32% from 4% in January 2025

The revised employment growth data averaged 29,000 in the past 3 months, with payrolls below 100,000 for four months. YTD, manufacturing, construction, and government have suffered the greatest job loss.

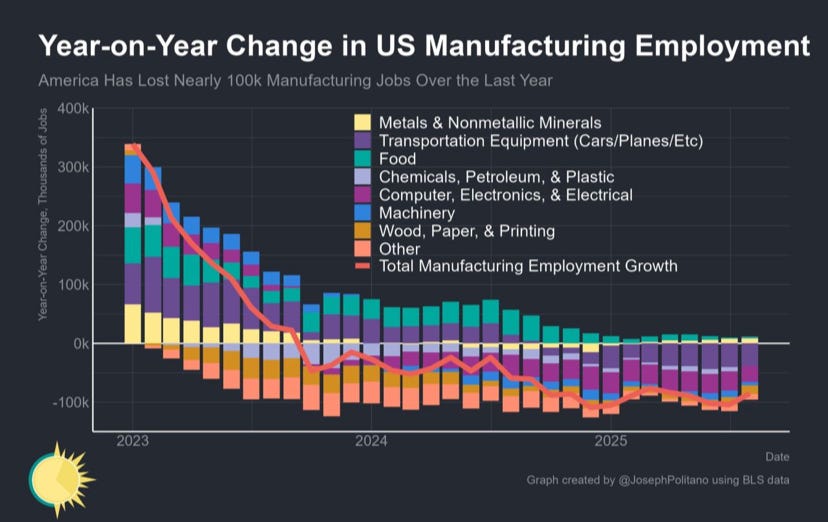

’s chart below shows how weak the manufacturing jobs have been, falling 85k year-over-year:

The futures market fully expects a rate cut in September and contemplates a 50bp cut (not likely) and a cumulative 150bp cut by late 2026.

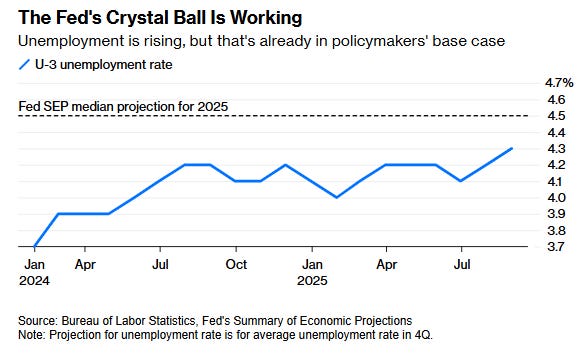

The Fed officials can say - I told you so, as back in June (SEP), they expected the unemployment rate and core inflation to end at 4.5% and 3.1% in 2025, respectively.

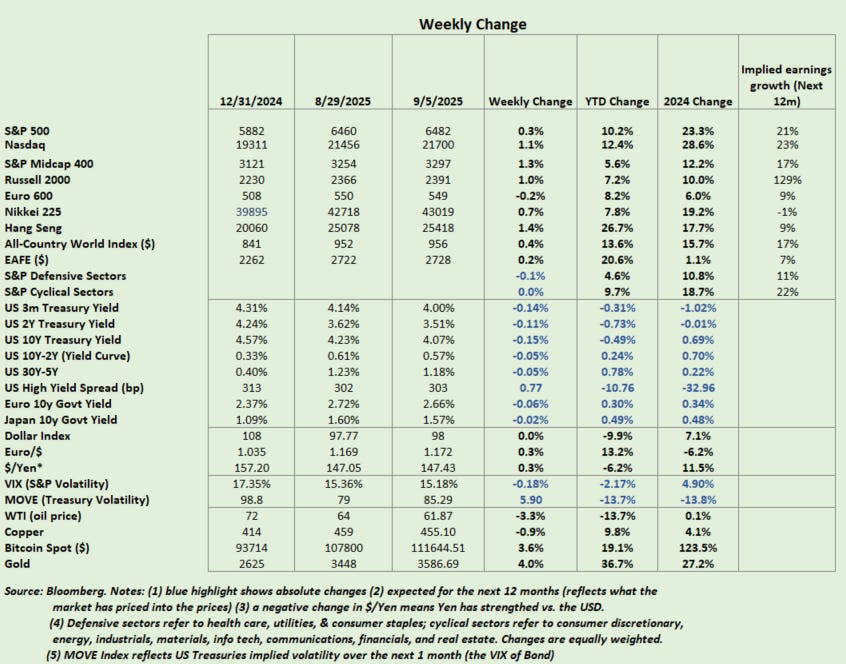

The S&P 500 and Nasdaq still ended positive for the week at 0.3% and 1.1% respectively, while the US 2-year Treasury yield fell 11bp to 3.51% and the 10-year yield fell 15bp to 4.07% and bond volatility (MOVE Index) jumped almost 6 points. Gold surged 4% to $3586.69 while oil (WTI) fell 3.3% to $61.87 this past week (see Peak Gold in One Chart Not to Miss below).

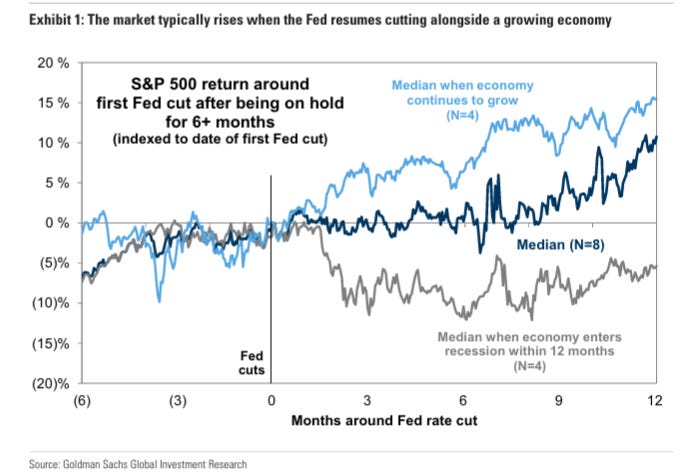

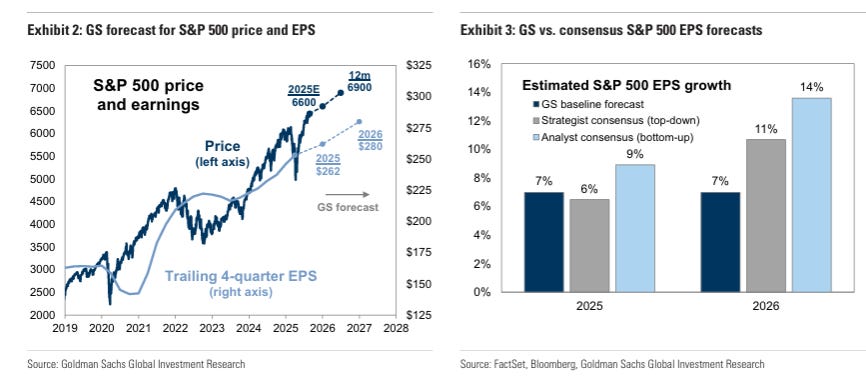

Investment banks, including Barclays and Goldman Sachs, now see 3 interest rate cuts this year, and according to Goldman, the S&P 500 can continue to rise after rate cuts if the economy continues to grow (its base case). Goldman expects earnings (base line) to grow about 7% next year.

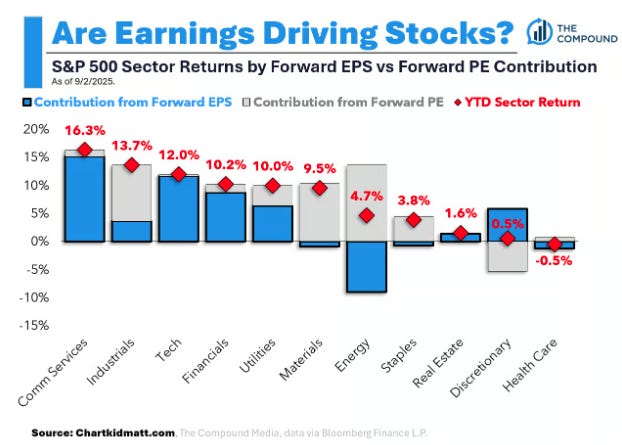

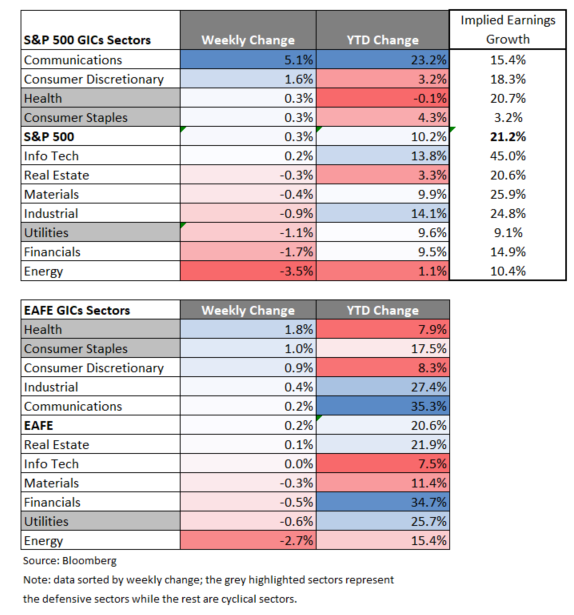

Another chart that caught my eye this week on US stocks is by Chartkidmatt.

You can see that communications and tech sector returns are almost entirely driven by forward EPS rather than forward P/E (multiple expansion), so they are not necessarily expensive. However, industrials, materials, and energy forward EPS have been hurt by tariffs, but stock prices have not budged yet.

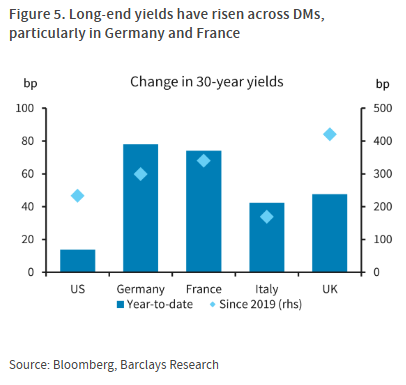

Turning to the bond market, the US bond rally prompted 10-year yields elsewhere in the world to fall, with the Euro Area bond yield falling 6bp, the UK falling 8bp, and Japan falling 2bp this past week.

This is despite fiscal woes and public debt burden being at the centre of Europe and the UK, causing their 30-year bond yields to rise dramatically YTD in Germany, France, and the UK, relative to the US (see charts below).

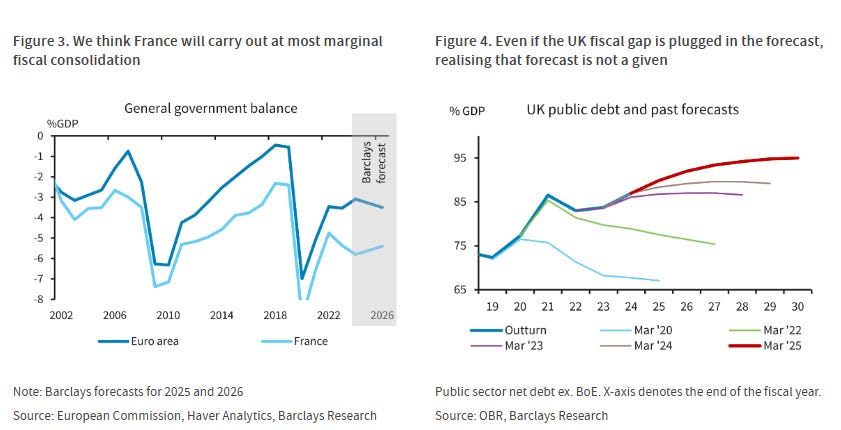

The French Prime Minister will call a confidence vote on September 8 to gauge the parliament’s resolve for budget-reducing policies. The French fiscal deficit has been stuck at over 5.5% GDP, while the UK public debt path is rapidly rising, with the chancellor calling for a 1% reduction in fiscal deficit, which will hit economic growth.

Neither the ECB nor the Bank of England is likely to cut rates further as the inflation target in Europe is reached, while inflation in the UK hit 4%.

Another country that has caught investors’ attention is Canada, whose stocks have outperformed those of the US in USD terms despite tariff uncertainty and its economic downturn. According to TD Economics:

“Like other countries in Trump’s crosshairs, Canada is facing economic hits. Its response is a domestic nation-building agenda. The game plan involves accelerating development of mining and energy projects, pumping more money into housing and infrastructure, and removing internal trade barriers among provinces. All told, Carney government’s has set a goal of “catalyzing” $500 billion in private investment over five years, worth about 25% of gross domestic product.”

The Canadian interest rate is now at 2.75% from 5% in 2024, and its trade with the US reached 40% of its GDP in 2024. While the effective tariff rate has risen from almost nil to now 6% (and rising), its market is tilted towards energy, gold miners, and banks — natural inflation hedges that provide high dividends.

This coming week, we will monitor the French Confidence Vote on Monday, the US August PPI on Wednesday and CPI on Thursday, the ECB interest rate decision on Thursday, Japan’s Q2 GDP estimate and China’s August exports growth on Monday, and China’s August CPI and PPI on Wednesday.

Economy and Investments (Links)

Bessent on Tariffs, Deficits and Embracing Trump’s Economic Plan - Bloomberg’s exclusive interview with Scott Bessent (Bloomberg Businessweek or Archive)

Bessent likes to call himself the nation’s “top bond salesman,” evoking the image of a stern-faced man with a green eyeshade going over coupon payments in a stuffy office. But in practice, the 100,000-employee Treasury under his watch has turned into a Department of Everything where, on any given day, trade deals are being negotiated, fiscal policy is being crafted, and national security is being fortified. Bessent is even serving as acting commissioner of the Internal Revenue Service. All of this gives him enormous sway over the US economy and reveals that, in practice, his role goes far beyond that of sounding board for the president…

Reasserting the dollar’s supremacy is one of the goals on Bessent’s list. So are fixing US bank regulation and ensuring that economic policy doesn’t benefit the financial class while leaving American workers behind.

The Labor Market is Cratering (Axios)

The big picture: The huge debate among economic policymakers is why hiring is so lackluster — less demand for staff, less supply of them (or a combination of both).

Harsher immigration policy is contributing to a huge shift in population trends. That makes it difficult to know how many workers the economy needs to add to keep the unemployment rate steady.

The Bond Doom-Mongers Have Got At Least One Thing Right (FT or Archive)

The inconvenient truth for Team UK Doom is that long-term government debt from rich countries is weakening everywhere, sending borrowing costs slowly but surely higher…All around the world, money managers are saying “enough”. The sheer amount of debt they are being asked to absorb is enormous, and the slow wind-down of key long-term pension demand means the appetite particularly for long-dated debt has simply shrunk. If governments want to stretch out repayments far in to the future, they must be willing to pay much higher interest rates to investors.

Finance/Wealth (Link):

5 Conversations to Test Whether Your Asset Manager’s AI Adds Value (Enterprising Investor)

(From the perspective of asset owners and investment consultants)

1. Definition and Scope: How Does Your Manager Define AI in Investing?

2. Organization and People: Who Runs AI at Your Asset Manager and How Are Teams Structured?

3. Experience and Added Value: How Long Has AI Been in Use, and What Has It Contributed?

4. Risks and Limitations: What Are the Pitfalls of AI in Investing?

5. Outlook: How Will AI Shape Asset Management and Client Communication?

Wellness and Idea (Link):

Ask These 3 “Naikan” Questions for a Happier, Healthier Attitude Toward Life (Mini Philosophy, Big Think)

Naikan is a nod to that Stoic idea of gratitude. It’s where the moral debt flips upside down — where you see the world not in terms of what it owes you or what it’s denied you, but in what it’s given you. But the Buddhist idea at the heart of Naikan is known as “dependent origination.”

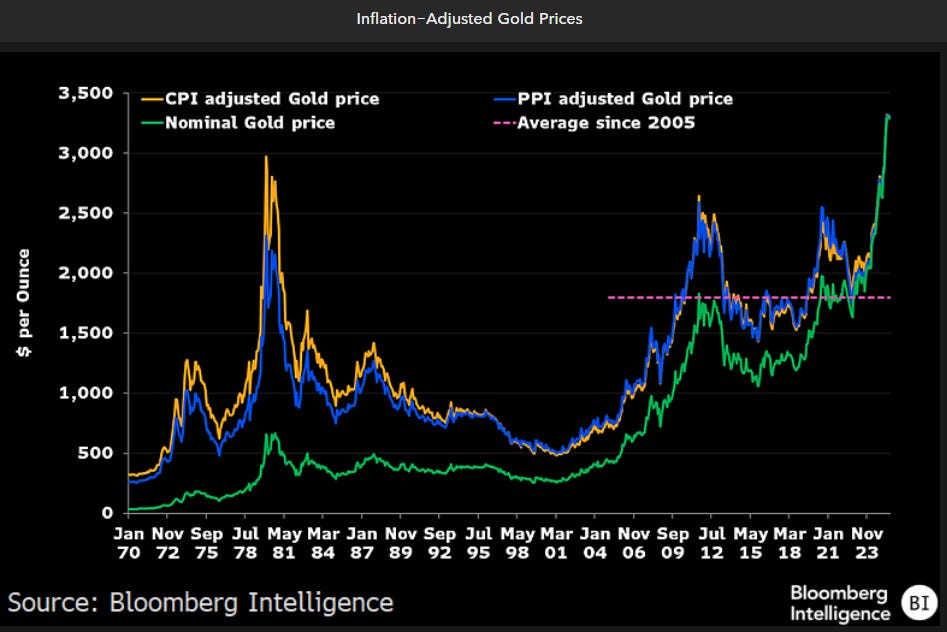

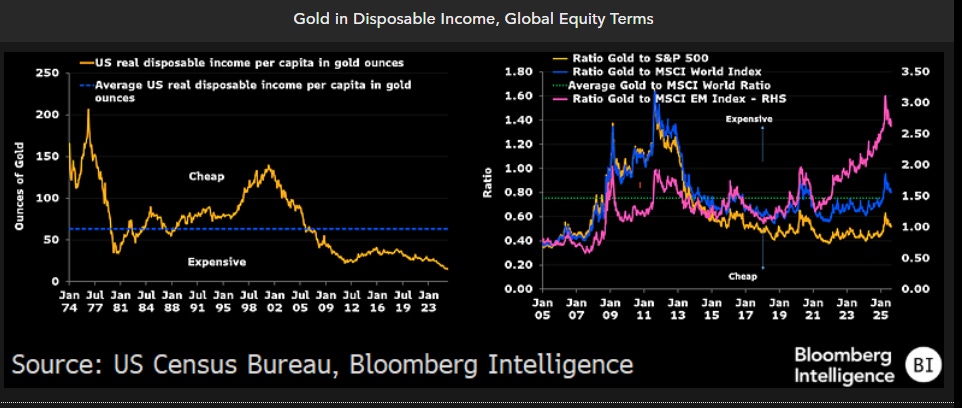

One Chart You Should Not Miss: Peak Gold Prices

With gold at above $3,500/oz, the inflation-adjusted gold price (averaging CPI and PPI-adjusted inflation at around $3,316) has become the most expensive since the US left the gold standard in 1974 (Bloomberg Economics).

Comparing gold price to equities (bottom right chart), gold is only cheap against the S&P 500 (at a 0.52 ratio) while at about 0.8x to MSCI World and about 2.7x to Emerging Market Equities, which makes the latter look cheap. These ratios suggest gold should be at around $3,000 compared to $3,587 as of September 5, 2025.

Geopolitical tension and investors’ need for tail-risk hedge have driven gold demand in the past couple of years.

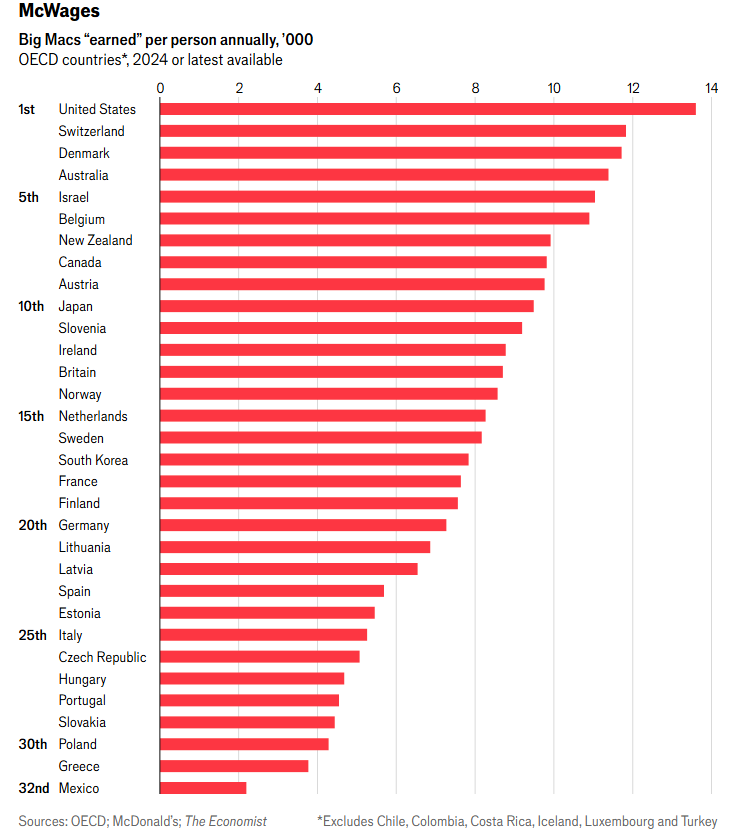

One Term to Know: The McWages Index (The Economist)

A PPP-Labour Market Framework: The Economist's McWages index uses a purchasing power parity framework to compare real wages across OECD markets, using Big Mac pricing as a standardized basket.

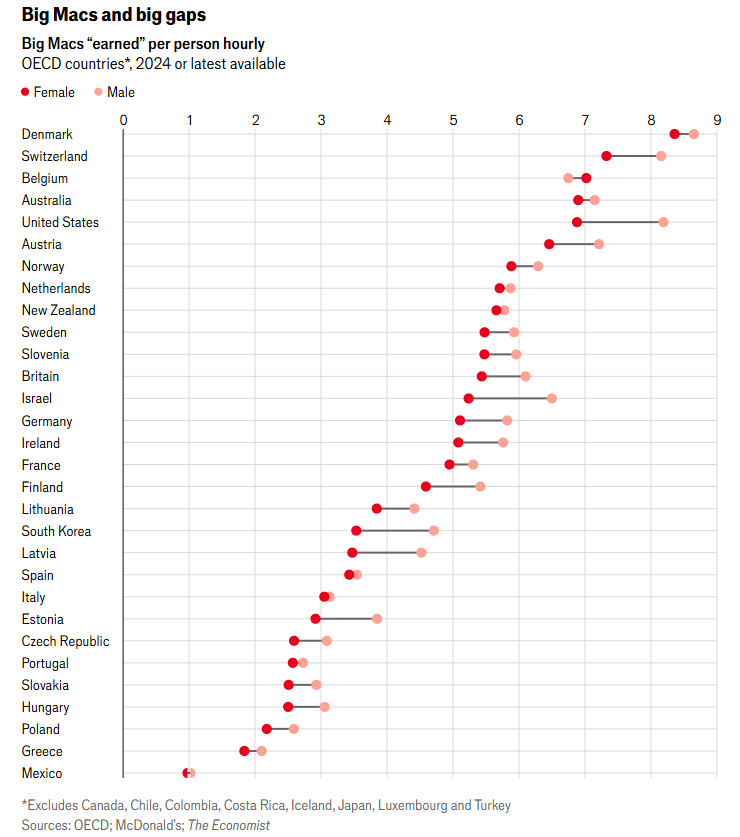

The methodology adjusts for part-time work and divides it by the cost of a Big Mac in local prices. US workers can buy 13,601 Big Macs a year versus 1,826 in Mexico, while on an hourly basis, Denmark leads at 8.5 units per hour worked, highlighting significant labour efficiency differentials across developed markets.

Regional Wage Inflation: Currency-adjusted wage growth is diverging significantly from food price inflation across key European markets. Germany experienced 13% Big Mac price inflation against 4% wage growth, dropping five positions in the ranking and signalling potential consumer spending pressure. Similar dynamics have affected the UK and Irish markets.

Gender Pay Gap: Cross-market analysis reveals persistent gender wage disparities averaging 0.5 Big Mac equivalents per hour across OECD countries. The US shows the largest differential at 1.31 units, while South Korea exhibits the highest proportional gap at 25%. Belgium is the only market with inverted gender dynamics, where women out-earn men by 0.27 units hourly.

🪷Things I learned About AI/Productivity

Top 10 AI Tools You Need in 2025 (There’s An AI For That)

Leonardo (Generating images and video)

Claude (Analyze long form document very well),

Suno (Music creation)

Deepseek (Super ability to think ahead and strategize)

NotebookLM (powerful knowledge assistant)

Thea (AI Tutor)

Perplexity (AI-Powered Search Engine with accurate links and sources)

Gemini (Integrated with all Google’s tools)

Freepik (AI Image Generator)

Open AI (TAAFT list of powerful prompts)

Thanks for reading!

Please do not hesitate to contact me if you have any questions, and check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please👍and share it with your friends, or subscribe to my newsletter🤝.