One Chart One Idea: Reshoring

The shifting macro trend and a new investment theme

In the One Chart One Idea series, I hope to explain one key economic, financial, or business phenomenon simply and factfully within 3 to 4 minutes. I welcome feedback on the topics you love to know more about.

What is Reshoring

Reshoring is the process of returning the production and manufacturing of goods back to the company’s original country or simply “back home”. Reshoring is also known as onshoring, inshoring, or backshoring.

Reshoring is the opposite of offshoring, and offshoring has been a dominant structural trend for Western economies in the past several decades.

The relocation of manufacturing production from the West to the East originated from trade liberalization, for example, with China’s entry into the World Trade Organization in 2001. Developed countries took advantage of the abundant labour supply and cheaper cost in developing countries, resulting in many companies shifting their manufacturing base to Greater China, which has developed a robust supply chain for materials and components.

Macro implications: US manufacturing sector is now only 10% of GDP. Germany’s manufacturing has declined from 25% to 19% in the past 20 years. Manufacturing prowess in the developing world has raised productivity and GDP growth there, but the opposite in Western economies.

With COVID-19, trade wars, and the Ukraine-Russian war, the fragility of the global supply chain was exposed. Inflation got out of Jeannie’s Bottle.

An arms race for re-industrialization has started due to decarbonization, de (re-) globalization, and remilitarisation.

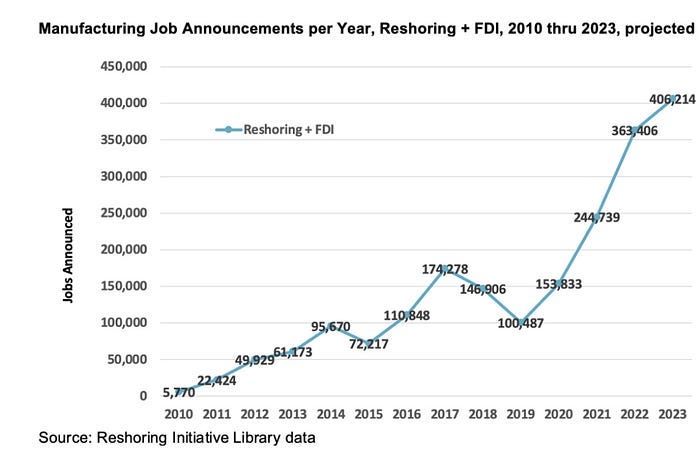

According to Reshoring Institute (chart below), reshoring is evident as manufacturing jobs announcements are projected to exceed 400,000 in 2023 in the US. Apart from the need to improve supply chain resiliency, the West also wants to resurrect the social and economic costs associated with the millions of manufacturing jobs lost.

The US Chips and Science Act directs about $280 billion (~$53 billion for semiconductor manufacturing) over the next ten years to bolster US semiconductor capacity, catalyze R&D, and create regional high-tech hubs and a bigger, more inclusive STEM workforce, according to McKinsey.

UBS study in March surveyed 1,600 senior executives who intended to move parts of the supply chain nearer home (“near-shoring”) — 78% in Europe, 70% in the U.S., and 54% in China have plans to do so.

Macro implications: Capex spending in the West will continue to rise, pushing up real interest rates, production costs, and prices as excessive savings have been spent (on investments) and countries are building redundancies in supply chains. Diversification of the supply chain from China takes time. Instead, companies are adding more production capacity outside of China while retaining major factory facilities in China (examples are Tesla and major pharma such as AstraZeneca and Pfizer.)

Investment Implications

Reshoring is a major investment theme for investors in the medium and long term in US semiconductor manufacturing and clean energy production. The first thematic ETF for American reshoring, ticker RSHO, began trading in May in the US, leveraging the ongoing upgrade of American industrial technology across multiple industries. Companies that supply semiconductor equipment and develop industrial components for automation tools will benefit from the re-industrialization trend.

This article is for informational purposes only. It should not be considered financial or legal advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.

Other One Chart One Series posts you might enjoy: