Weekly Good Reads: 5-1-1

Moody's US Downgrade, Tariffs, Q1 Profit Guidance Momentum, Power of Habits, Industrial Policy, AI Engineers

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work! Please hit the 💛 button if you like it or share with others.

Sharing the quote of the week:

Any great power that spends more on debt service than on defense risks ceasing to be a great power.

~ Niall Ferguson

Weekly archives | Investing | Ideas | Index of charts and terms | Conversations with Investment Managers

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Try R4A for free!

Market and Data Comment

The biggest news for the market this past week was the US-China tariff announcement, with the US “reciprocal” tariff reduced to 30% on Chinese imports (and likely 10-30% eventually), and a 10% tariff by China on US imports for 90 days (see chart above). (According to the Fact Sheet from the White House, the US will retain all duties imposed on China prior to April 2, 2025). With a universal tariff of 10% on the rest of the countries and sectoral tariffs at 25%, US tariffs may end up at 14-17%, still a sharp jump from around 2.5% before Trump got into office.

The US-China trade embargo was no longer a likely scenario. The US economy is also not expected to get into a recession (Barclays, Goldman), while Euro GDP growth will be flat, and that of China, around 4% in 2025.

The S&P 500 Index rebounded ~20% since the April 8th low (led by tech, consumer discretionary, and communications), and is now positive YTD (S&P, +1.8%, and Nasdaq, -0.25% YTD). The VIX dropped 4.7% to 17.2%.

The US 10-year Treasury yield is only 9bp lower YTD at 4.48% as of May 16, 2025 and jumped 10bp this past week as the S&P 500 rallied ~5%. The Dollar Index was barely up, +0.8%, while gold, a favourite hedge this year, plunged 3.6% for the week.

The 10-Year yield remains high despite a softer-than-expected CPI (+2.3% y/y, albeit a further rise in goods inflation) and PPI, +2.4% y/y, helped by services deflation. Still, the recent University of Michigan consumer survey reported a jump in long-term inflation expectations to 7.3% for a one-year horizon (highest since 1981) and medium-term inflation expectations at 4.6%.

The US April retail sales were +0.1% m/m (1.7% m/m prior), with consumption on tariff-related goods most impacted, although food service spending remained robust.

After the market closed on Friday, Moody’s downgraded the US credit rating to Aa1, stripping its triple-A status. This is the first time in history that the US has received no triple-A rating from any credit rating agency.

Moody’s warned of the decline in fiscal metrics despite US financial strengths, expecting its fiscal deficit to widen to 9% by 2035 from 6.4% in 2024 due to rising interest payments and entitlement spending while relatively low revenue generation. US federal debt (held by the public) reached $29 trillion ($36.2bn in total, including various government accounts) in 2024. The Committee for a Responsible Federal Budget projects that the tax bill could add up to $5.2 trillion to the national debt over 10 years (see Econ/Invest #1). US public debt ballooned from 60% in the early 1990s to 122% in Q4 2024. A recession will gravely exacerbate the public debt-to-GDP path.

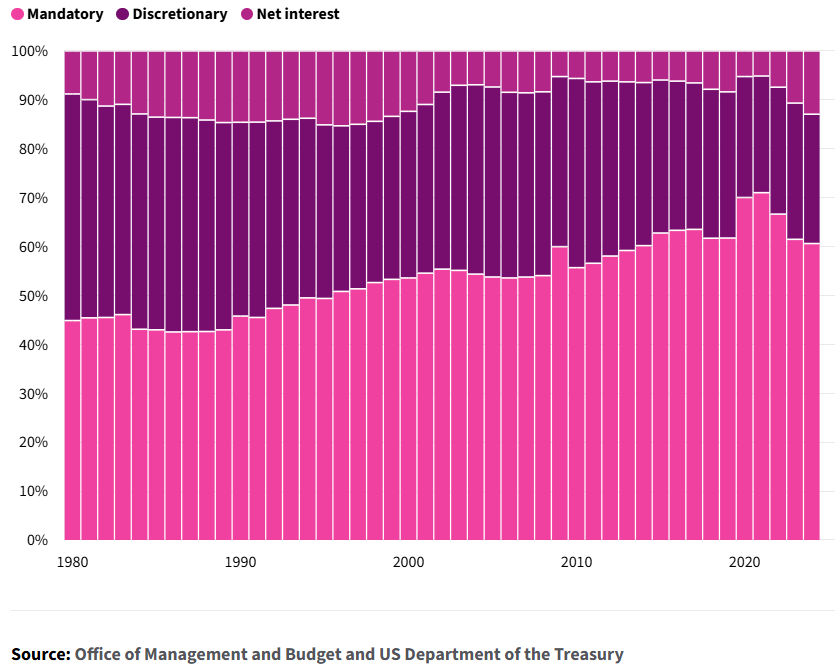

For reference, US fiscal spending has increased 2.9 times from 1980 to 2024 at $6.8 trillion (vs. population increase by 1.5 times). From the chart below, 61% of federal spending is mandatory (e.g. Medicare and social security), while only 26% is appropriated by Congress (discretionary).

Based on the reported Q1 earnings, the profit guidance momentum, which is the proportion of the S&P 500 members that raised their earnings outlook compared to those that held or reduced (see chart below), fell to the lowest level since 2013 (Bloomberg). Companies from the US, Europe, and China have cited rising costs, weak consumer sentiment, and a lack of business confidence as a result of trade tensions, albeit reporting better-than-expected earnings results.

With Trump admitting his government could not handle all the trade talks, he would announce unilaterally (again!) tariff rates for all countries over the next two to three weeks. Expect US stocks to weaken in the near term, especially with market focus on the deteriorating US debt situation.

This coming week we will monitor US May S&P Global Composite PMI on Thursday, April new home sales on Friday, Euro Area April inflation on Tuesday, Composite PMI on Thursday, and Germany Q1 GDP on Friday, UK April CPI on Wednesday, Japan April CPI on Friday, and China’s April retail sales, industrial production, YTD fixed asset investment on Monday, and May 1y loan prime rate announcement on Tuesday.

Economy and Investments (Links)

Moody’s Strips US of Top-notch Triple-A Credit Rating (FT)

Moody’s said it expected federal deficits to widen to almost 9 per cent of GDP by 2035, up from 6.4 per cent last year, owing to increased interest payments on debt, entitlement spending and “relatively low revenue generation”.

“This one-notch downgrade on our 21-notch rating scale reflects the increase over more than a decade in government debt and interest payment ratios to levels that are significantly higher than similarly rated sovereigns,” the agency wrote.

The Anecdote Economy (Axios)

"It's more than any supplier can absorb. And so I'm concerned that consumer is going to start seeing higher prices. You'll begin to see that, likely towards the tail end of this month, and then certainly much more in June"—Walmart CFO warned.

China’s Achilles Heel (Semafor)

China’s eagerness to strike a trade deal comes from its status as an economic outlier: Its citizens don’t shop. China’s consumer spending as a percentage of GDP is lower than all but two advanced economies: Ireland, whose GDP is artificially inflated by tech and pharma companies using it as a tax haven, and Singapore, where expenses like housing and health care are subsidized.

Finance/Wealth (Link):

These Investors Cashed In by Holding Firm When Markets Slumped (WSJ)

Skillman, a Santa Fe, N.M., resident whose portfolio is split between stocks and bonds, stood pat throughout the market gyrations of early 2025. “I never panicked,” the 60-year-old investor said. “Timing the market is fruitless. No one has a crystal ball.”… He and other investors with an equally steely resolve are being rewarded in a big way. President Trump’s easing of his harsh tariff policies has stoked a comeback in stocks, with major indexes recovering their losses since he rolled out his plans on April 2. The S&P 500 returned to positive territory for the year on Tuesday, rising 0.7% to its highest close since Feb. 28 and extending gains that began Monday after the U.S. and China agreed to suspend most tariffs.

The Wellness/Idea (Link):

Why the Power of Habits Might Just Live Up to the Hype (Atlassian)

We may know how to form good habits, but how about breaking bad ones?

Identify the habit you’d like to leave behind.

Add friction to the undesired action.

Create a desirable alternative.

Recognize when you successfully avoid the undesired action.

One Chart You Should Not Miss: The Trump Effect (Returns vs. Tariff Vulnerability)

Oxford Economics plotted the rank of stock market returns vs. the country’s tariff vulnerability rank (measured by their reliance on American revenue, the size of their manufacturing sectors, and their sensitivity to global industrial cycles) in April (since April 2nd).

There is a strong negative relationship—the lower the tariff rank, the higher the stock market return.

The best-performing stock markets have generally two characteristics: (1) low exposure to American tariffs and stock markets dominated by industries less affected by tariffs, and (2) strong domestic growth.

For example, the IBEX Index (Spain's major stock index) returned much better than Italy and Germany, both of which have a worse tariff vulnerability rank. Spain is growing strong due to tourism and the inflow of immigrants, and its stock market is dominated by energy and utilities, sectors which tend to be more defensive when the market turns down.

One Term to Know: Industrial Policy

Industrial policy refers to government efforts to support and develop specific sectors of the economy, usually through funding, tax incentives, regulations, or public–private partnerships.

Note that there have been about 4,000 trade-distorting industrial policy measures worldwide between January 2023 and June 2024 (IMF & Global Trade Alert), indicating a new wave of industrial policies revival.

The goals of industrial policy are to promote innovation, secure key supply chains, boost domestic manufacturing, and achieve broader social goals like clean energy or national security, aiming at fixing market failures (e.g., underinvestment in R&D) without distorting competition.

said in his recent talk on tariffs that one benefit of industrial policy is “technological spillover”, where supporting tech companies spring up (as in the Silicon Valley) around tech giants targeted by industrial policy. Critics, however, warn of the risks in “picking winners” and misallocating public resources.Since 2020, the US has launched a major shift toward industrial policy, marked by large federal investments. This has become a central policy tool for the US to compete in a more fragmented and tech-driven global economy.

The policies include the CHIPS and Science Act ($280 billion through FY 2027in semiconductor production and applied scientific research and 52.7 billion specifically for semiconductors), the Inflation Reduction Act (including around $370 billion for clean energy and $64 billion for Affordable Care Act extension), and the Infrastructure Investment and Jobs Act (over $1 trillion for infrastructure and manufacturing). These laws aim to rebuild American capacity in high-tech and green sectors and create high-quality jobs. The US also created new programs to support battery production, critical minerals, and biotech.

The US approach can mobilize massive resources quickly, targets strategic goals like climate and security, and encourages private investment. But the downsides are slow program rollouts, political pushback from allies, and the risk of inefficient spending. Compared to its peers, the US strategy is more subsidy-driven and flexible but may lack long-term coordination, not to mention that the wrong industry can be backed like the memory (DRAM) chips for national security reason (turned out to be a commodity).

🌻Things I learned About AI/Productivity:

Microsoft Engineers Replaced by AI? (LA Times)

The job cuts come as the rise of artificial intelligence, which can also generate code, is raising questions about how technology will impact software engineers and other workers.

Software engineering roles made up 53% of Microsoft’s job cuts in Silicon Valley, according to data provided to the EDD. Positions in product management, applied sciences, electrical engineering and other fields were also eliminated.

In April, Microsoft Chief Executive Satya Nadella said that as much as 30% of the company’s code is written by AI during a conversation with Meta Chief Executive Mark Zuckerberg at the social network’s AI developer conference.

AlphaEvolve: AI’s Highlight of the Year (The White Box)

In succinct terms, [Google’s] AlphaEvolve is an iterative search system that uses Large Language Models (LLMs), like Gemini, to iterate over code to find new solutions to given open problems.

In layman’s terms, it’s an orchestrator system that takes in a human task and uses an LLM or set of LLMs to propose new changes to the code, evaluating the quality of the changes, and readapting, creating a recursive self-improving loop that has yielded incredible results.

Design, Code, and Create, With Our Biggest AI Launch Yet (Canva)

My most favourite software, Canva, has announced a powerful suite of AI-powered creativity.

💫 We launched Canva AI, your all-in-one creative partner for generating designs, images, and text from a simple prompt, while Canva Code lets you build interactive experiences – no coding required – and add them to any design.

💫 AI-powered Canva Sheets unlock data-driven design – no spreadsheets skills needed.

💫 Our Photo Editor got a major AI glow-up, making precision edits and generating backgrounds as easy as point and click.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.