Weekly Good Reads: 5-1-1

FOMC, Trade Talks/Deals, $ vs. Asian Currencies, Tariff Buying Guide, Longevity Economy, International Investment Position

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work! Please hit the 💛 button if you like it or share with others.

Sharing the quote of the week:

The secret to winning is learning how to lose. That is, learning to bounce back from failure and disappointment—undeterred—and continuing to steadily march toward your potential. Your response to failure determines your capacity for success.

~ James Clear

Weekly archives | Investing | Ideas | Index of charts and terms | Conversations with Investment Managers

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Try R4A for free!

Market and Data Comment

As widely expected, the FOMC kept the target interest rate unchanged at the range of 4.25% to 4.5% and planned to roll off Treasuries at $5 billion per month (reduced from $25 billion per month) and $35 billion per month for agencies starting in April.

The FOMC statement repeated what Fed Powell had said before, that risks of higher inflation and higher unemployment had risen. Appearing slightly hawkish, the FED preferred to wait to see weakness (if any) in the hard data and was in no rush to adjust rates and emphasized the need to anchor consumers’ long-term inflation expectations.

The market reacted by pushing the first rate cut to July instead of June and priced in two cuts of 50bp in total by December.

The far bigger focus of the market was on trade talks progress, especially between the US and China, who are meeting for the first time in Switzerland during the weekend, after Trump’s tariff hike. Earlier in the week, the UK and the US announced a provisional trade deal where it eliminates the sectoral tariffs on steel and aluminum for the UK and reduces car tariffs from 25% to 10% for a quota of 100,000 cars, while the UK will open access to US ethanol and beef and fast track US goods through customs.

The market may not overreact to this trade deal, as the UK goods are only 2% of US imports (and the US has a trade surplus with it), while the minimum tariffs remain at 10%, and there are more details to iron out. Barclays raised the question of whether these trade talks will end the rules of the multilateral trading system and whether the parties will commit to keeping the deal. PIMCO warned investors not to underestimate Trump’s resolve to restore the tariffs that upended the market in early April, and the risks of recession were the highest in years.

The US-China meeting should be viewed as tariff descalation negotiation (see Econ/Invest #1), which may ultimately lower the tariffs from the US on China to 50 to 60%, according to many geopolitical analysts.

China, while enjoying an 8.1% jump in exports in April, saw a 21% decline in shipments to the US as trade was re-directed to India/Southeast Asia (shipments up 20%), and the EU (exports up 8%). However, US-China container shipments have tanked 30-40% both ways. If these US-China tariffs continue, Chinese goods rerouting via Southeast Asia will jump, leading also to concern about Chinese goods dumping into Southeast Asia.

Another consequence of the trade war is the continuous decline in the US Dollar, especially against Asian currencies. A prime example is the Taiwanese Dollar, which surged 6% in early May, partly because the central bank allows the currency to appreciate amid trade talks, and because companies rush to repatriate earnings into local currencies and investors buy local stocks and dump US assets as the dollar weakens.

The message to hone is that the world cannot turn back to pre-”Liberation Day” tariffs and must deal with the economic and trade order shift, which has major implications for the countries’ currencies and their local economies — for example, China’s top regulators held an extraordinary joint briefing to announce a slew of policy easing and consumption-related liquidity boosting actions (also see Econ/Invest #2). More proactive fiscal policies are needed in light of the deflationary pressure and weak demand in the Chinese economy — April CPI fell to deflation (-0.1% y/y, 0.1% m/m) while PPI (-2.7%) fell to a 6-month low.

Here are a few key market indicators for market stress I am monitoring (see chart below). While the US stocks have surpassed the end of March levels, the dollar appears stabilizing at these low levels (black line), and the VIX (purple line) and high yield spread (blue line) have sharply declined, the financial stress index (green line) has not recovered while the US 10 year Treasury yield (orange line) remains somewhat elevated at 4.38%, +7bp this past week.

This coming week, we will monitor the US April CPI on Tuesday, the April retail sales, PPI, industrial production on Thursday, and housing starts on Friday, the Euro Area Q1 GDP and March industrial production on Thursday, Japan’s Q1 real GDP on Friday, and China’s April total social financing next week.

Economy and Investments (Links)

U.S.-China Meetings Might Cut Tariffs. Uncertainty Won't Go Away (Barron’s or Archive)

…neither markets nor the economy may be off the hook even if the Geneva talks go off without a hitch and result in a rollback of tariffs. And there still is the risk that the meetings don’t yield a de-escalation, or worsen tensions.

“Unless there is a real dramatic reversal where the Trump administration openly, or privately, waves a white flag, the stalemate the U.S. is in with China and others is likely to endure, certainly through the end of 2025,” said Scott Kennedy, a senior adviser focused on China at the Center for Strategic and International Studies.

The Economy Doesn't Get Rewired Overnight (Axios)

The big picture: Seismic economic shifts — of the kind that look to have been set in motion by trade war escalation — usually ripple through the economy only over the course of months, even when the precipitating event is sudden.

(1) Whether this episode turns out to be a temporary hiccup or a painful recession, we shouldn't expect to see clear-cut evidence in the data for quite some time.

(2) Similarly, while the stock market rally from the recent April 8 low — and accompanying stabilization in the bond market — has been fast and furious, it's not uncommon for asset prices to retrace losses, at least temporarily, in times of economic disruption.

Asian Investors Fear More Volatility After ‘Extraordinary’ Currencies Moves (FT or Archive)

Investors described the 6% surge in the Taiwanese Dollar in May as a “once-in-a-lifetime event”. This happened because Taiwan has accumulated a big stockpile of US$ assets due to its large trade surplus with the US ( by selling semiconductors). Now, the companies and investors are concerned about a weakening US dollar and have rushed to repatriate these earnings into local currencies, causing them to appreciate rapidly.

Investors rushed to buy domestic stocks and sell American bonds held via local funds, dumping the greenback and hitting one of the biggest, and least hedged, dollar piles of any Asian economy…Stephen Jen, chief executive of hedge fund Eurizon SLJ, said in a note that exporters in China, Taiwan, Malaysia and Korea were collectively holding trillions of US dollars offshore that could be repatriated, which would cause an “avalanche” of rising local currencies.

Finance/Wealth (Link):

America Is Getting Older. How to Play the Longevity Economy (Barron’s)

The code words to look for regarding this new investment opportunity in the longevity economy are things like “easy,” “convenient,” “wellness,” and “performance.”…

And let’s not forget about the “F” word—fun…This demands innovation in everything from adaptive fashion tech to immersive travel experiences to social platforms designed for mature users without signaling the offerings are for “old” people. The opportunities extend into luxury markets, wellness tech, and what I call ageless retail…

A big investment opportunity in these areas is also women. Within the aging population, the catalysts of innovation, the chief consumer officers, are women. They live longer, and are the primary caregivers and most trusted advisors to younger people. And they buy almost everything you can imagine.

+ Why Gen X is the Real Loser Generation (Economist or Archive)

Gen Xers have also done a poor job accumulating wealth. During the 1980s, when many boomers were in their 30s, global stockmarkets quadrupled. Millennials, now in their 30s, have so far enjoyed strong market returns. But during the 2000s, when Gen Xers were hoping to make hay, markets fell slightly. That period was a lost decade for American stocks in particular, coming after the dotcom bubble and ending with the financial crisis.

Wellness/Idea (Link):

The Ultimate Tariff Buying Guide (Bloomberg or Archive)

One Chart You Should Not Miss: China As the Top World Manufacturer

According to a Morgan Stanley study, despite trade diversions, at a global level, China was able to find alternative markets for its products and retain No. 1 market share in most key global exports. If we map all products in the world, China has a leading market share in the majority of manufacturing products and across sectors (see chart below). It is often much harder to shift the production of goods due to higher costs, longer lead times, and greater investment risk, and so re-routing of trade will likely continue.

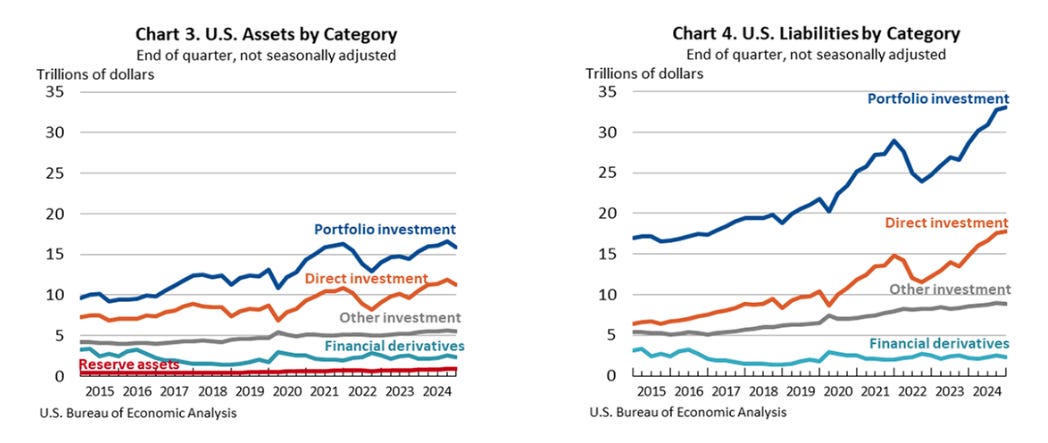

One Term to Know: Net International Investment Position (NIIP)

There are three key concepts of NIIP:

NIIP measures the gap between a nation’s stock of foreign assets and a foreigner's stock of that nation's assets. It shows a country's international assets versus liabilities at a specific point in time.

Assets: These are things a country owns abroad (like investments in foreign companies, stocks, bonds, and real estate).

Liabilities: These are things a country owes to foreign entities (like when foreign investors buy a country's stocks, bonds, or real estate).

It can be viewed as a country’s balance sheet with the rest of the world at a particular moment, reflecting the country’s financial condition and creditworthiness. In other words, NIIP reflects a country's financial relationship with the rest of the world.

For example, a nation with a positive NIIP is a creditor nation (country owns more abroad than it owes), and a debtor nation if NIIP is negative (country owes more than it owns).

The following charts show the Net IIP of the US since 2015, showing a growing gap between liabilities and assets:

What has caused this rising negative gap? According to the US Bureau of Economic Analysis, US liabilities jumped by $7.86 trillion to a total of $62.12 trillion at the end of 2024, driven by U.S. stock price increases and by financial transactions that largely reflected foreign purchases of U.S. long-term debt securities and stocks, especially a jump in portfolio investment and direct investment liabilities, showing growing foreign demand in US investable securities as well as direct investments.

🌻Things I learned About AI/Productivity:

Open AI Chief Sam Altman: This is “Genius-level Intelligence” (FT or Archive)

While Silicon Valley has been sinking massive investment into AI, DeepSeek, a Chinese start-up, released a model this year developed on a limited budget. That suggested that AI models were becoming commoditised and the US technological edge over China was diminishing. Altman says there is an “asterisk” to the commoditisation narrative: “Most of these models will be commoditised. The frontier models I don’t think will be.” He is, of course, expecting to prevail in frontier models but also win in the commoditisation game, given how many users are already attached to ChatGPT.

And how will OpenAI deliver the returns on massive investment? Altman hints at his ultimate goal, but describes it as just one compelling idea: when a subscription to ChatGPT becomes a personal AI, through which users log into other services. “You could just take your AI, which is gonna get to know you better over the course of your life, have your data in and be more personalised and you could use it anywhere. That would be a very cool platform to offer.”

LinkedIn’s New AI Tools Help Job Seekers Find Smarter Career Fits (Fast Company)

Powered by large language model (LLM) AI, the new search tool interprets the intent behind job seeker queries and job descriptions, making it easier to match people with opportunities in a job market that often frustrates both applicants and employers…

Another new feature, “job match,” helps users assess their fit for a role before applying. By analyzing both job descriptions and user profiles, the AI identifies how closely someone matches a job’s criteria and highlights areas where qualifications are strong or lacking—such as experience with a particular technology.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

As informative and thought-provoking as always! A small typo: "The market reacted by pushing the first rate hike to July instead of June and priced in two hikes of 50bp in total by December." - you probably meant rate cuts.