Weekly Good Reads: 5-1-1

Hard vs Soft Data, Fed Powell’s Job, Treasury Term Premium, How Not to Invest, Bear Market

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work!

Sharing the quote of the week:

Whatever you're meant to do, do it now. The conditions are always impossible.

~ Doris Lessing

Weekly archives | Investing | Ideas | Index of charts and terms | Conversations with Investment Managers

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Try R4A for free!

Market and Data Comment

Investors have recently noticed the divergence between hard and soft data (sentiment survey). For example, the US March retail sales surged 1.4% m/m, the biggest jump in more than two years, thanks to consumers’ rush to purchase major items, including cars, electronics, and appliances, to get in front of the price increase due to tariff implementation.

The Atlanta Fed’s GDPNow is tracking Q1 real GDP growth at -2.2% (annualized) (only -0.1%, excluding the impact from gold imports and exports) compared to the Blue Chip consensus of about +0.5%, as of the time of writing.

The IMF, which will release its new global economic outlook this coming Tuesday, will likely mark down global growth due to the trade system reboot, but does not see a recession.

The uncertainty of an on-and-off tariff implementation policy by the US holds back corporate investments (both domestically and internationally), not exactly the recipe for bringing back manufacturing jobs to the US.

Rising tariffs hit growth upfront as evidences show that higher tariff rates were paid by importers through lower profits and consumers through higher costs. Even if jobs return to the home country, this takes time (per IMF).

The worst hit will be smaller businesses, which now make up over 80% of the total US employment and capex, and have to cancel orders or find money to pay for tariffs, with worse implications on the US macro economy, should the tariff uncertainty carry on long enough. An unstable government is a tax on business costs, whether it is a developed or an emerging country.

Trump has put the Fed in a bind between controlling inflation and maintaining full employment (see Econ/Invest #1). Fed Powell said significantly larger than anticipated tariffs will likely have the same larger impact on economic effects, which will include higher inflation and slower growth. Fed governors also do not seem to agree on whether the inflationary impact will be short-lived, putting the Fed in a wait-and-see mode. Any clear signs of a slowdown in employment will likely cause the Fed to resume cutting rates, in my view.

Since the US elections, the term premium of the US Treasury has been rising, whether because of the worry of the US fiscal situation and rising debt, a jump in consumer inflation expectations (more recently), or US trade policy instability. The market will be closely watching Trump’s actions on Fed Chairman Powell’s position (firing is still an implausible but disastrous scenario), and who will be the next Fed chair.

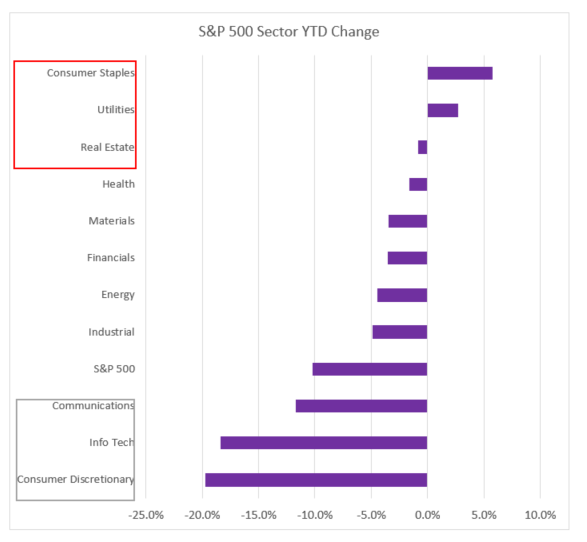

YTD, US stocks have fared worse than their developed market counterparts (except for Japan) — see Weekly Change Table — albeit the S&P 500 has avoided a bear market so far (see One Term to Know).

Different causes of a bear market lead to different lengths of time for the market to break even, as Goldman pointed out (see chart below), with a structural-led bear market taking the longest to recover (9 to 11 years, 2x as much as cyclical-led). This correction so far is event-led but the bear can morph into a cyclical event, with rising recession risk.

While no market indicators have done as badly as during COVID or 2008-2009 Great Recession in the recent market dislocation, I will be watching the dollar index, US high yield credit spread, 10Y US Government Bond yield, Global Financial Stress Index as well as the various volatility indices including VIX (stocks) and MOVE (bonds) as signs for market breakdown.

This coming week, we will monitor the IMF World Economic Outlook to be released on Tuesday during the IMF/World Bank Spring Meetings, the Euro Area April preliminary Composite PMI on Wednesday, and the US March existing home sales on Thursday.

Also, Big Tech earnings announcements begin this week with Tesla on Tuesday and Alphabet on Wednesday. Their guidance not necessarily past results will be key to watch especially their capex spend on AI and data centers and how they expect these to return profits. Microsoft, Meta, and Amazon will be on April 30 while Apple will be on May 1 with Nvidia on May 28.

Economy and Investments (Links):

Donald Trump’s Tariffs Put the Federal Reserve’s Jobs and Inflation Goals at Risk, says Jay Powell (FT or Archive)

While US rate-setters would aim to “balance” their goals of keeping inflation near 2 per cent and maximising employment, they would need to remember that “without price stability, we cannot achieve long periods of strong labour market conditions”, Powell said in remarks to the Economic Club of Chicago.

Powell also said the president’s tariffs announced so far had been “significantly larger than anticipated”, adding that “the same was likely to be true of the economic effects, which will include higher inflation and slower growth”.

Is the World Losing Faith in the Almighty US Dollar? (FT or Archive)

[E]ven though the dollar’s unique role may be sustained by inertia and a lack of alternatives, it can still lose value. Despite its declines in April, the DXY dollar index is still 12 per cent higher than it was at its lows in 2020, and almost 40 per cent over its nadir in early 2008. Many foreign exchange analysts are now ripping up their previous forecasts and predicting further falls for the dollar.

For example, Goldman Sachs — previously optimistic on the dollar — now predicts the US currency will fall to $1.20 against the euro and ¥135 against the Japanese yen over the next 12 months, equivalent to another 6 per cent weakening from the current levels. “The negative trends in US governance and institutions are eroding the exorbitant privilege long enjoyed by US assets, and that is weighing on US asset returns and the dollar, and may continue to do so in the future unless reversed,” Goldman’s foreign exchange analysts warned.

Mapping the American Economy’s Internal Lines of Fragility (

)Over the past four decades, the U.S. economy has come to lean ever more heavily on its financial sector, often at the expense of factories and real‑world production.

In 2000, financial services accounted for roughly 7 percent of GDP; by 2023, that share had climbed to 8.5 percent, even as manufacturing’s slice fell from about 12 percent to 10 percent—shifting $400 billion of economic weight away from “making things” and into trading paper.

Meanwhile, decades of rising stock buy‑backs and consolidation have buoyed headline growth but failed to lift living standards for most Americans.

Finance/Wealth (Link):

Avoid the Unforced Investment Errors Even Billionaires Make (The Big Picture)

The author discussed the 5 common behaviours (errors or better actions) of investors in his book “How Not To Invest: The ideas, numbers, and behaviors that destroy wealth - and how to avoid them”: (1) paying more fees than they realised (2) buying after a huge market run (3) put “mad” money (not more than 2% of your total) in a cowboy account (4) not selling any of your holdings when you receive a windfall (5) chasing yield.

Decades as an investor and trader on Wall Street have taught me that panics come and go. Drawdowns, corrections, and crashes are not the problem – your behavior in response to market turmoil is what causes long-term financial harm.

Wellness/Idea (Link):

Your Mantras (Axios)

Big ideas often come in small packages, and we've received nearly 1,000 emails from readers around the country and the world sharing the one-liners they live by.

My personal favourite from the list 💖 — what is yours?:

🗞️ "'Wear a belt and suspenders at the same time,' meaning have a backup plan and be prepared for anything. Got this from my old boss at The Miami Herald, a legendary sports editor and journalist named Ed Storin." —Paul Anger, Griffin, Ga.

One Chart You Should Not Miss: US Goods Exports to China by States

While the market may focus on the 145% tariff rate Trump imposed on China how much China has been exporting to the US, about $439 billion in 2024, the US still sent $143.5 billion worth of energy, agricultural and other goods to China, nearly 50% of which are energy supplies and produce that come from just five states Texas, California, Washington, Louisiana and North Carolina. These goods are now subject to the 125% tariffs imposed by China.

One Term to Know: Bear Market

A bear market generally refers to a 20% drop from a previous peak of a broad market index such as the S&P 500 over two months or more. It can also refer to the poor sentiment, risk aversion, and selling of stocks by investors over a prolonged period.

A bear market is different from a correction, which means the index drops between 10% to 19.9% from its previous high.

Causes of a bear market can include economic slowdown and sometimes (not always) recessions, bubble bursting, pandemic, big economic policy shifts like raising interest rates rapidly, etc.

The S&P 500 Index flirted with a bear market during trading on April 7 and closed at -18.9% on April 8 from its recent peak on February 19, 2025. That was the second-fastest 20% drop since 1945 (the fastest was at the beginning of COVID) before the market reversed on April 9th upon Trump’s tariff pause and has not (so far) re-touched the bear-market territory.

This sell-off also followed the fourth shortest bull market since WWII (an annualized 24.3% gain from its start on October 12, 2022, to its peak on February 19, 2025).

Goldman Sachs, analyzing data since 1835, classifies bear markets into three categories:

“Structural” bear markets – triggered by structural imbalances and financial bubbles (on average lasted 42 months, with a drop of -57%, taking 111 months to recover)

“Cyclical” bear markets – typically triggered by rising interest rates, impending recessions and falls in profits (on average lasted 21 months, with a drop of -37%, taking 50 months to recover)

“Event-driven” bear markets – triggered by a one-off “shock” that either does not lead to a domestic recession or temporarily knocks a cycle off course. Cyclical bear markets are the most common (on average lasted 8 months, with a drop of -27%, taking 12 months to recover).

Since 1835, bear markets have lasted 25 months, and have fallen on average 36%, although since WWII, bear markets have lasted much shorter at 13 months with a recovery period back to the previous high in 22 months.

The bear market this time (if we are there) is likely an event-driven one. The risk is that it can morph into a cyclical one, with rising recession risk.

Bear market is more normal than we think, but over the long term, stocks rise significantly. Hartford Funds found that since 1929, about 42% of the S&P 500’s best days in the last 20 years occurred during a bear market. Another 36% of the market’s best days took place in the first two months of a bull market before it was clear a bull market had begun.

Goldman finds that since 1980, using the MSCI All-Country World Index (which captures large and mid-cap stocks in developed and emerging markets) as an example, bear market rallies on average last 44 days, bouncing between 10% to 15%. In the past 45 years, note that despite the average median calendar year drawdown was 15%, the MSCI All-Country World Index was positive 34 out of 45 years!

The above speaks to staying invested in the market — “time in the market” beats “timing the market”. Resist the temptation of chasing the mini rallies that likely occur during a bear market. Ask yourself this question when you review your asset allocation: Is this the exposure I would like to hold for the long term today?

One more: Where does the term “bear market” come from?

Anatoly Liberman, a linguist at the University of Minnesota, says the use of “bull” and “bear” to refer to financial optimists and pessimists, respectively, originated in Britain in the early 18th century. “Bull” evoked the bellowing of an eager buyer. “Bear” appears to have come from an early proverbial expression, “to sell the bear’s skin before one has caught the bear" [meaning people betting on a declining market and expecting to buy back when prices are lower]. (WSJ)

[🌻] Things I learned About AI/Productivity:

How Can We Work Smarter in An Era of Endless Productivity Tools? (Tech Brew)

Amid all this exhaustion, frustration, and dissatisfaction, workers are devising their own solutions and turning to their personal favorite apps to meet their professional needs.

“This causes a huge problem,” Paulman said. “This is one of the things that’s fueling the ROI crisis with AI, is that information is fragmented across hundreds of apps.”

Elevate Your AI Prompting Skills in Under 5 Minutes (

, )

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.