Weekly Good Reads: 5-1-1

US Tariff Pause, Why Bond Yield Rose, Sell American, Swap Spreads, Combatting Market Chaos, AI is Mandatory

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work!

Sharing the quote of the week:

I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a . 400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.

~ James Carville

Weekly archives | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌).

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Please try our firm’s solution R4A. It’s free!

Market and Data Comment

(This week I talked a bit more on the technical conditions of the US bond markets—hope it is useful!)

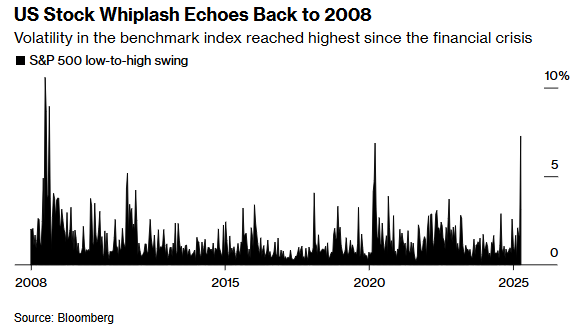

US stocks’ high-low swing reached that during the 2008-9 financial crisis recently when Trump announced “Liberation Day” tariffs on April 2nd and then changed course on April 9th, right after the “reciprocal tariffs” had started.

The broad “reciprocal tariffs” have been paused for 90 days until July 9th as trade negotiations continue, but a 10% minimum tariff has now been implemented for all countries (except for China), with smart phones, computers, and other electronics being quietly exempted from tariffs.

However, given the latest effective 145% tariff on Chinese goods, the effective tariff rate on US imports jumped from an average of 2.5% before Trump’s tariff announcements to 27% as of today, the worst level since 1903 (see Econ/Invest #1). Price impact will be 3% in the short run, a loss of $4,700 per household in 2024 dollars and a negative drag on long-run US real GDP level by 0.6% (Budget Lab).

While S&P 500 staged a 9.5% rally on April 9 and rose 5.7% for the week, avoiding the bear market for the moment, the real focus for the markets was on the US bond yield, where both the US 10-Year and 30-Year Treasury yield jumped 50bp this week (almost matching what happened at the beginning of the COVID lockdown), while the US dollar slipped 2.8%, a serious sign that capital were flowing out of the US (across assets) during this crisis (see charts below), unlike previously, when the US dollar and US Treasuries acted as safe havens as the economy cratered.

The warning signal from the bond (not the stock) markets likely caused Trump to pause the tariffs. As Larry McDonald pointed out, during stock market crashes in 2008, 2001, 1997 or 1987, bond prices rose, not fell.

The rise in bond yield took place when the US had a bunch of soft data - March CPI and core CPI rose 0.05% and 0.06% on the month (2.4% and 2.8% y/y respectively) while the University of Michigan flash April consumer sentiment plunged to 50.8 (the second lowest reading ever). However, short-term inflation expectations (UMich) have already jumped to 6.7%, while for the long term, 4.4%.

Explanations (FT and WSJ) on the rise of Treasury yield ranged from hedge funds and traders unwinding Treasury basis trade—hedge funds usually sell the more expensive Treasury futures and buy the cheaper equivalent Treasury bonds to hedge themselves, capturing a few basis points but using a lot of leverage (up to 50 times with outstanding estimated at around $800 billion).

Hedge funds borrow money in the ultra short-term repo market using (you guess it right) Treasury bonds as collateral to finance these trades, but as volatility of the cash Treasury bonds increase and the demand for cash increased like recently, Treasury yields jumped, making these trades untenable so hedge funds had to answer margin calls and unwind the trades by more selling of the cash Treasury bonds as hedge funds closed their positions (hence yield went up and prices went down further).

Another even more plausible explanation is that bankers and traders had been betting on the US swap spreads to widen. The swap spread is the difference between the fixed rate component of an interest rate swap and the yield on the Treasury bond with the same maturity, and the swap spread has been negative recently (see more on One Term to Know). Traders ran up their US Treasury holdings, anticipating a change in US banking regulation where the Trump administration will enable banks to hold more US Treasuries on their balance sheet, thus causing the negative swap spread to flip. But as the long bond sold off, the swap spread turned even more negative, raising margin calls and more positions to unwind.

Not to mention, Japan and China, the two biggest holders of US Treasury bonds, hold $1.8 trillion, and market fears they are selling.

Any rise in US Treasury yield defeated the US administration’s intention to reduce the rapidly rising federal debt interest expense ($9 trillion of debt to refinance this year). The flip-flop nature of US policy-making and uncertainty of the tariffs’ end game (usually seen in emerging markets) has eroded investors’ confidence in the deepest and most liquid US Treasury market, from which all other debt instruments (credit, loans, mortgages) are priced off.

Now, holders demand more term premiums to hold the otherwise safe Treasuries. Despite the US dollar's status as the largest reserve currency (60% of all currencies), the rest of the world will question whether the US is the right place to put their money in, at least in the short run (see Econ/Invest #2). This is more the case when dollar declines making alternative government bonds such as German bonds a preferred alternative as a safe haven (also helped by Euro rising).

As to why China could play the long game of this trade war, Bloomberg pointed out that US imports as a share of Chinese total imports is 17.2%, smaller than the share of Chinese imports as a share of US total imports, which is 18.5% (see chart below).

Zero in the black bars: the left-hand side bars are much bigger than the right-hand side bars. The US mainly imports consumer goods from China that they cannot quickly replace, while China mainly imports intermediate industrial inputs from the US, which they can source elsewhere. Moreover, Chinese President Xi has the best chance to rebalance China’s economy towards more consumption and fulfill his promise of consumption stimulus.

One more thing to consider, not to suggest it will, this article argues that the Smoot-Hawley Tariff Act of 1930 didn’t trigger or worsen the Great Depression but probably triggered World War II, as international economic relations like trade wars can become a good excuse for extreme nationalists to fulfill their goals.

This coming week, we will monitor US March retail sales, industrial production, and housing starts on Wednesday, the Euro area inflation on Wednesday, the ECB interest rate decision on Thursday, China’s March exports on Monday, Q1 real GDP, March retail sales, industrial production and YTD fixed asset investment on Wednesday, as well as Canada’s interest rate decision on Wednesday.

Economy and Investments (Links):

Despite the Pause, America’s Tariffs are the Worst Ever Trade Shock (Economist or Archive)

The announcement excludes China, leaves in place all earlier tariffs and implements the universal 10% minimum portion of the reciprocal tariff. America’s “effective tariff rate”—total tariffs paid as a share of total imports—may still rise by 15-20 percentage points. Even after the about-face, the incoming levies represent the most disruptive policy in the history of global trade.

Treasuries Suddenly Trade Like Risky Assets in Warning to Trump (Bloomberg or Archive)

Even if this dynamic was to fade as swings in stocks eventually normalize, as most analysts expect, a message has been delivered to policymakers in Washington: Investor confidence in US bonds can no longer be taken for granted — not after a years-long borrowing binge that swelled its debt load and not with a president in the White House hell-bent on rewriting the rules at home and abroad and antagonizing, in the process, many of the country’s biggest creditors…Treasuries and the dollar get their strength from “the world’s perception of the competence of American fiscal and monetary management and the solidity of American political and financial institutions,” said Jim Grant, founder of Grant’s Interest Rate Observer, a widely followed financial newsletter. “Possibly, the world is reconsidering.”

From Apple to Samsung, Trump's Tariffs Force Supply Chains to Adapt -- Fast (Nikked Asia or Archive)

Many U.S. electronics makers, including Dell, HP and Apple, are highly exposed to their home market. Analysts worry that tariffs will hit these companies and their suppliers harder and push up retail prices for key consumer electronics. This, in turn, will weigh on the overall market outlook.

Apple, for example, earns about 40% of its revenue in North America, Bernstein Research estimates, but over 80% of production of its flagship iPhones occurs in China. The iPhone production shift to India is ongoing but cannot yet meet all the consumer demand.

"The reciprocal tariffs will significantly impact all major tech hardware manufacturing hubs," Alex Wong, an analyst with Bernstein Research, said in a research note.

Nikkei Asia

Finance/Wealth (Link):

Four Questions You Should Ask to Combat the Market Chaos (WSJ)

*What exposures do you have, and why do you own them?

*Why do you own stocks?

*What has changed?

*If you don’t already own this asset, would you buy it now?

+ Why Value Investors Are Looking at Japan, Korea, and Brazil (Institutional Investors)

Wellness/Idea (Link):

How Reading 25-30 Minutes a Day Transforms Your Brain (Medium)

According to research by the University of Sussex, stress levels can drop by up to 68% within 6 minutes of reading.

That’s faster than going for a walk, drinking tea, or listening to music.

After particularly rough days, my 30-minute reading window felt like hitting a mental reset button.

One Chart You Should Not Miss: China’s Global Trade Dominance

One Term to Know: Swap Spreads

A swap spread is the difference between the fixed interest rate in an interest rate swap (swap rate) and the yield on a government bond (like a U.S. Treasury) of the same maturity.

Interest rate swaps are derivative contracts to exchange fixed interest payments for floating rate payments linked to a benchmark rate. The side that receives the fixed rate makes money when interest rate falls while losing money when interest rate rises.

A positive swap spread, as normally is the case, reflects a higher credit risk than holding US Treasury bonds. Rising swap spreads can indicate a rising risk aversion in the market. Thus, swap spreads reflect the market's collective sentiment in risk management, cost of protection, and trading liquidity.

Negative US swap spreads have been more prevalent since 2015. Recently, traders have been waging on a change in bank regulations, which may allow more US Treasury bonds to be held on the banks’ balance sheets, thus increasing demand for Treasuries, lowering their yield, and increasing the swap spread.

However, due to chaos and economic fear from Trump’s tariff announcements, traders and banks have been selling Treasury bonds to raise cash to meet client’s liquidity demand while maintaining long exposure on the interest rate swap fixed rate, thus making the negative swap spread go even more negative.

[🌻] Things I learned About AI/Productivity:

Canva Create Uncharted - Introducing Visual Suite 2.0: Productivity, Meet Creativity (Canva)

@TheAIAndy summarized 6 big features, including Canva AI (text or voice), Canva Code, Magic Charts (dynamic and scrollable), Canva Sheets (Excel), Photo Editor (AI), and Visual Suite in One Design.

Viral Shopify CEO Manifesto Says AI Now Mandatory For All Employees (Forbes)

This isn’t bravado, attention-seeking or trying to be the “cool kid” in the industry. It’s realism. For organizations in the crucible of generative AI disruption — media, retail, finance, logistics — awareness and experimentation are no longer enough. Adaptation is the new mandate and must start at the top.

OpenAI Updates ChatGPT to Reference your Past Chats (Techcrunch)

The company says the feature, which appears in ChatGPT’s settings as “reference saved memories,” aims to make conversations with ChatGPT more relevant to users. The update will add conversational context to ChatGPT’s text, voice, and image-generation features, the company added.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.