Weekly Good Reads: 5-1-1

FOMC, Tariffs, Central Banks Reactions, 125 Years of Investment Returns, Interest in Chinese Equities, Stagflation

This week’s piece came late as I was vacationing with family in the hot spring and red rock mountainous area in Shaoguan, Northern Guangdong, China, and I hope I can write with a fresh perspective.

***

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work!

Sharing the quote of the week:

To understand others, watch what they reward.

To understand yourself, watch what you envy.

~ James Clear

You will find some useful sections below.

Weekly archives | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌).

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Please try our firm’s solution R4A. It’s free!

Market and Data Comments

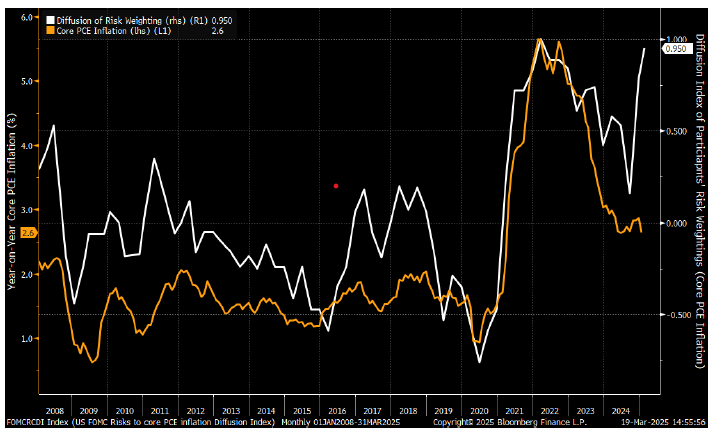

In last week’s FOMC, the Fed left the interest rate unchanged at 4.25% to 4.5%, and the median Fed Funds rate forecast is two 25bp cuts this year, another 50bp cut in 2026, and 25bp in 2027. The March Summary of Economic Projections (SEP) hinted at stagflation (see One Term to Know below)—median end-2025 real GDP growth will be 1.7% vs. 2.1% in December 2024’s SEP, the unemployment rate will be 0.4% higher (to 4.4%), and inflation at 2.7% at year-end vs. 2.5%.

While Chairman Powell described the inflation due to tariffs as having a “transitory” impact (see Econ/Invest #1), Powell also admitted, “I don't know anyone who has a lot of confidence in their forecast." While inflation and employment have been the main focus of the Fed, the core drivers of the economy are now shooting from other parts of the economy—Trump’s trade policy, immigration restrictionism, and deregulation (all amount to a negative supply shock to reduce economic growth and push up inflation—which the Fed’s policy cannot counteract both).

What is certain is that FOMC participants admitted inflation risk was to the upside (see the white line in the top chart showing the upside risks jumped relative to downside risks).

Markets continue to be whipsawed by Trump’s tariff announcements. Expectations of softened reciprocal tariffs prevented the S&P 500 from bleeding last week (up 0.5% for the week, -3.6% YTD) as the S&P went into a 10% correction by mid-March from its peak on February 19 this year.

Central banks have become followers rather than “frontmen” of their respective economies, as Trump’s tariffs could upend their economic plans. The Bank of Japan and the Bank of England left interest rates unchanged in their recent monetary policy meetings. While Japan is expected to increase interest rates in July due to wage hikes and depressed real interest rates, both Japan and the UK consider tariffs as a new economic risk, as tariffs can slow economic growth and raise inflation, thus adopting a wait-and-see attitude possibly until May when Trump’s tariff policy should become clearer.

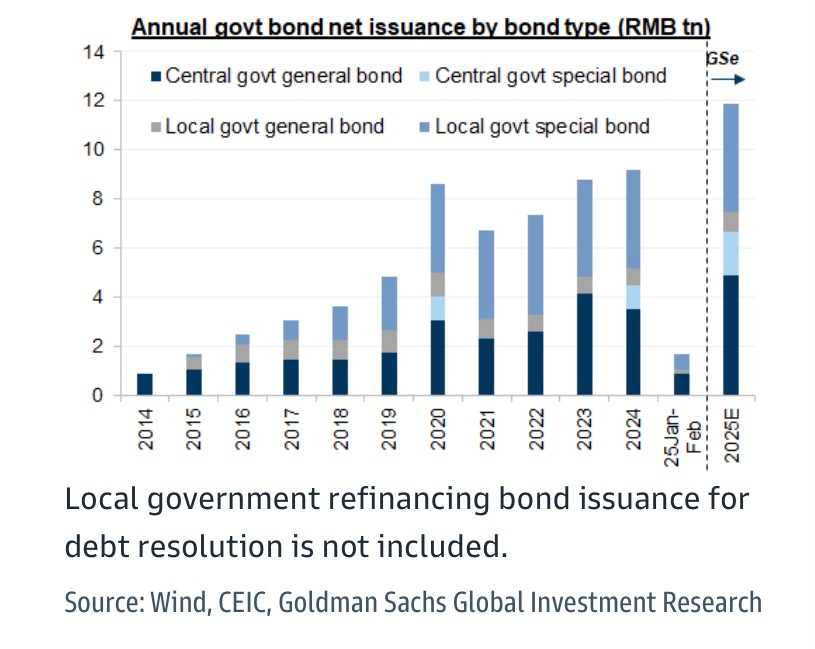

As to China, it is expected to step up its fiscal spending, announced recently at the National People’s Congress to aid the economy and counteract the impact of Trump’s tariffs. Recent government bond issuance (mainly directed to the local government to relieve their local debt burden) has been running twice the year-earlier amount (see charts below).

Goldman Sachs estimated below the net bond issuance by central and local governments this year (even without that for debt resolution), as a large fiscal quota has been planned.

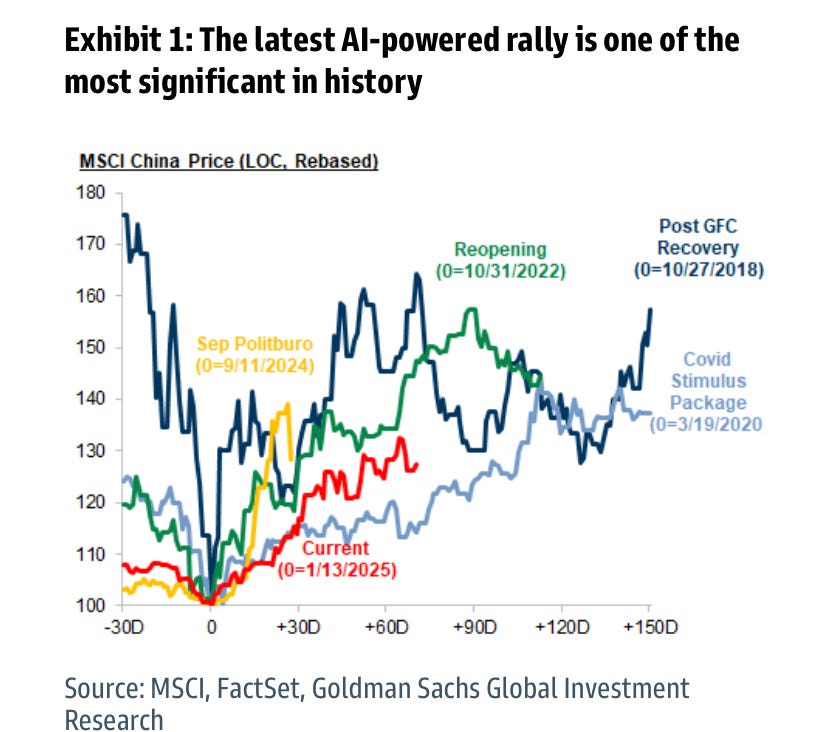

With AI leading the rally in Chinese stocks and their outperformance against the US counterparts and the better ability for the Chinese government to withstand impact from tariffs in Trump 2.0 (due to reduced US exports exposure and better product competitiveness) as well as green shoots appearing in the economy in terms of more stable property demand, rising escavator sales (proxy for infrastructure spend), and higher demand for construction materials, China is back in fund managers’ radar screen from hedge funds, quant funds, traders, to long-only funds (see One Chart You Should Not Miss below).

At the least, the government is firmly putting a floor to China’s economic growth, allowing investment banks to upgrade their GDP growth forecasts for China closer to 5% this year.

Deepseek has awakened other Big Tech Chinese names offering low-cost AI services (at least 10 products announced), and this is the beginning.

Separately, based on my ride-sharing experience using “DiDi” in China, many people have purchased EVs and become “DiDi” drivers (switching from being passengers before!). Considering the monthly costs of electricity, insurance, and maintenance charges, I estimate a “DiDi” EV driver can make up to RMB5,000-6,000 a month. The EV cost/km is around one-tenth of the ICE cars. I believe the auto components and consumer sectors as well as technology are interesting sectors to gain exposure.

[You can use my referral link to try “DiDi”, the global platform to save money 🥳].

This coming week, we will be monitoring the US March preliminary S&P Global Comoposite PMI and the Euro Area March preliminary composite PMI on Monday, US February new home sales on Tuesday, personal spending and core PCE price index on Friday, UK’s February CPI on Wednesday and Japan’s March Tokyo CPI on Thursday.

Economy and Investments (Links):

Powell Downplays Growing Risks, Sees Tariff Impact as Transitory (Bloomberg or via Archive)

Speaking to reporters following a two-day meeting of policymakers, Powell downplayed mounting growth concerns and the price hits that could be on the way from President Donald Trump’s aggressive trade war. He even revived a once-abandoned term to say the inflationary impact of tariffs is likely to be transitory…

“As I’ve mentioned, it can be the case that it’s appropriate sometimes to look through inflation if it’s going to go away quickly without action by us, if it’s transitory,” Powell said.

Is This the Start of a Period of European Exceptionalism in Markets? (FT or via Archive)

[O]ne can see how the tide is turning. The adversarial stance of Trump has galvanised the region into action. Fiscal policy is being loosened, and not only in the area of defence. Germany’s €500bn infrastructure package alone is a boost of 1 per cent of the country’s GDP annually over the next decade. Monetary policy is also easing. It looks likely that real interest rates will soon be back close to zero in the Eurozone and the UK. This is already spurring loan growth. And, finally, regulatory stipulations are easing in areas such as climate change policy.

Here’s Where to Look for Early Signs of a Recession (WSJ)

Major economic data hasn’t yet begun to fully capture Trump’s time in office. The Wall Street Journal is looking at a host of other indicators to try to figure out whether the U.S. might skirt a recession, or fall into one. Here are some to watch, with a focus on companies, consumers and workers.

+ White House Narrows April 2 Tariffs (WSJ or via Archive)

Trump’s comments came hours after he said the U.S. would impose a 25% tariff on any country that buys oil or gas from Venezuela. Trump said that the 25% tariff would augment existing duties, including the 20% tariff he levied on China this year. That would mean 45% tariffs on the U.S.’s third-largest trading partner. According to an executive order that was signed later Monday, those tariffs will take effect “on or after” April 2.

Finance/Wealth (Link):

Global Investment Returns Yearbook 2025 – what 125 years of history tells us about the future (UBS) - Here are some of their observations:

Markets have changed dramatically. Of the US firms listed in 1900, ~80% of their value was in industries that are small or extinct today; the UK figure is 65%.

The long-run outperformance of stocks has been striking. Equities have outperformed bonds, bills and inflation in every country. An initial investment of USD 1 in US equities in 1900 grew to USD 107,409 in nominal terms by end-2024.

Concentration is a growing issue. Despite a relatively balanced global equity market in 1900, the US now accounts for 64% of world capitalization, largely due to the outperformance of major technology stocks.

Diversification has helped manage volatility. While globalization has increased the extent to which markets move together, the potential risk reduction benefits from international diversification [especially emerging markets] remain large.

Inflation is an important consideration in long-term returns. Asset returns have been lower during periods of rising interest rates and higher during easing cycles. Real returns have also been lower during periods of high inflation and higher during periods of lower inflation. Gold and commodities stand out among the few inflation hedges.

Wellness/Idea (Link):

The Three Styles of Curiosity (Greater Good Science Centre)

One Chart You Should Not Miss: China is Back on Investor’s Radar Screen

According to Goldman’s field trip across institutional investors and fund managers globally, investors’ interest and engagement levels in Chinese equities are at their highest since their historical peak in early 2021.

Reasons:

The AI-led (Deepseek) rally (MSCI China +16% and Hang Seng Tech +23% YTD) have significantly outperformed the DM and EM counterparts (1% and 6%), leading to more growth optimism driven by a bottom-up, innovation-powered investment thesis.

President Xi’s meeting with private business leaders indicates that domestic regulatory pressures are easing.

Global funds are seeking alternatives outside of US stocks; given China’s liquidity, valuations, and low correlation with the US, China is receiving renewed investor interest.

One Term to Know: Stagflation and What’s the Fed Going to Do This Time

Stagflation is defined as persistent high inflation combined with high unemployment and stagnant demand.

It was what happened in the 1970s. The US government engaged in fiscal expansion (escalated US involvement in the Vietnam War from 1965 to 1973, collapse of the managed currency rates), stimulating aggregate demand to arrest the economy from recessions. In 1973, the Arab oil embargo, wage-price spiral, and across-the-board inflation caused inflation to surge past 12% (core CPI). Ultimately, Fed Chairman Paul Volcker stepped in and raised interest rates to 21% to curb uncontrollable money supply growth and clamped down the inflationary spiral, but this brought negative economic growth in 1979 (-0.2%) and 1982 (-2% real GDP).

While the Fed has the dual mandates of maintaining stability in prices and employment level, the Fed Fund tools cannot be used to control both, as in the case of stagflation.

So far, there has not been any surging inflation or distress signals like in the 1970s, but due to the unexpected tariff policies under Trump, the Fed may have to pause any interest rate cuts to allow inflation to increase (temporarily) until long-term unemployment also rises, which should cause inflation to decline and the Fed to then cut interest rates.

While tariff policies change quickly, the Fed monetary policy works with a “long and variable lag”. Managing the two goals of the Fed is especially tricky, thus rendering a wait-and-see attitude for the Fed.

[🌻] Things I learned About AI/Productivity:

A New Generation of AIs: Claude 3.7 and Grok 3 (

)Finally, and perhaps most importantly, we need to rethink how we measure and value AI contributions. The traditional metrics of time saved or costs reduced may miss the more transformative impacts of these systems - their ability to generate novel insights, synthesize complex information, and enable new forms of problem-solving. Moving too quickly to concrete KPIs, and leaving behind exploration, will blind companies to what is possible. Worse, they encourage companies to think of AI as a replacement for human labor, rather than exploring ways in which human work can be boosted by AI.

2. Adobe and Zoom Deploy AI Agents (Tech Brew)

Experience AI: Adobe’s agents are mostly centered on helping marketers craft messages, steer them toward the right people, and improve the various ways companies appear online. For instance, the site optimization agent might continuously scan a company’s website for broken backlinks, something that Adobe said its customers don’t often have the time to do…

Zoom in: Zoom’s agentic approach is part of a broader effort to widen its role in the office from a video call interface to a hub for all things meetings. Its agentic tools will help participants settle on a time to meet, easily create clips, and assist in drafting documents.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.