Weekly Good Reads: 5-1-1

Deglobalization and Disruption, Consumers' Worry, Junk Bond Yield Spread, Falling US Treasury Yields, International Diversification, GDP Deflator

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work. I appreciate you for reading and taking the time!

Sharing the quote of the week:

Great things are done by a series of small things brought together.

~ Vincent Van Gogh

You will find some useful sections below.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

👉 Interested in building customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Please try our firm’s solution R4A. It’s free!

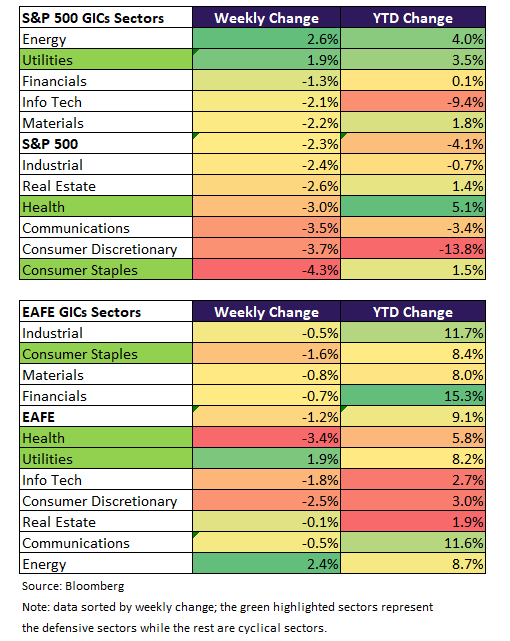

Market and Data Comments

While it is easy for investors to get caught in the poorer market sentiments and surging policy uncertainty emanating from Trump’s policy announcements and actions (S&P 500, Nasdaq, and Russell 2000 (small caps) have fallen -5.5%, -9.4%, and -23.7% respectively since the US election day on November 5, 2024 to today), Professor Aswath Damodaran reminded us of two macro forces—deglobalization and disruption—have taken place years before Trump 2.0 (see Econ/Invest #2). This necessitates baking politics and macro into investment analysis for developed markets, usually more a consideration in emerging markets.

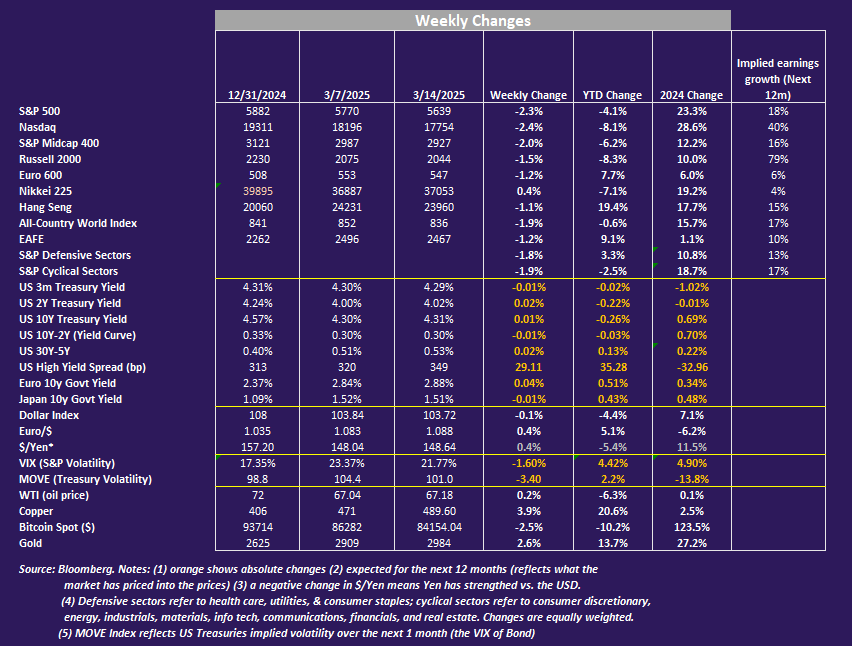

This past week, the US February CPI and core CPI rose 0.2% m/m (core CPI, 3.1% y/y), lower than expected. February PPI was flat m/m, but services including health care and financial services that feed into core PCE (Fed’s preferred inflation gauge) rose firmly. Bloomberg estimated core PCE deflator (due March 28) likely accelerated to 0.35% in February (0.28% prior) and raised the core PCE inflation at year-end by 0.1% to 2.8% y/y.

This will likely feed through the March FOMC summary of economic projections (FOMC on March 18-19) and raise the median dot plot for year-end 2025 inflation. The market currently is still pricing in 2 interest rate cuts in 2025.

Barclays pointed out there are three things investors are now more certain of: (1) Trump is willing to impose more tariffs than market initially expected and the “Trump put” is missing (2) there will no longer be a security blanket for Europe from the US, and (3) Trump’s international policies are moving away from a multilateral institutional framework to a more direct, transactional approach.

These changes are associated with companies pulling back capex plans, consumers more worried about losing their jobs (see top chart), rising long-term inflation expectations (latest 3.9%), slowing airline bookings, and weaker credit card data (Torsten Slok), which could bring about weaker hard data like more downside risk in the March non-farm payrolls report (to be released on April 4).

In addition, US High Yield Bond spread has now widened above the Pan-European High Yield Bond spread, which has fallen YTD (see chart below). This past week, the US junk bond spread widened 29bp and 35bp YTD, still relatively calm compared to the jump/levels in 2022 and 2023.

US junk bond usually sniffs out trouble ahead of equities. Its relative stability points to the fact that the US has no solvency issues, and the volatile stock market has been a negative reaction to the self-inflicted Trump tariffs rather than restrictive monetary conditions (as per Bloomberg). The high yield bond spread as well as any changes in company profitability are both worth watching, especially when the market is worried that the Trump administration is prioritizing “detoxing” the economy than focusing on pro-growth policies (see Econ/Invest #3).

This coming week, we will monitor US February retail sales on Monday, housing starts on Tuesday, and the FOMC rate decision and the Press Conference (and March Summary of Economic Projections) on Wednesday, Euro Area March preliminary consumer confidence on Friday, Bank of Japan’s rate decision on Wednesday, Bank of England’s monetary policy decision on Thursday, and China’s Jan-Feb fixed asset investment (YTD), retail sales, and industrial production on Monday.

Economy and Investments (Links):

How the US Economy Lost Its Aura of Invincibility (FT or via Archive)

The predicted slowdown is remarkable in that it is largely a self-inflicted wound driven by the administration’s own policies, economists say, rather than the consequence of external shocks such as energy price surges, war, pandemics or banking implosions. While Trump made it abundantly clear during his election campaign that he wanted to double down on the trade wars of his first term, his policies have proved far more wide-ranging and aggressive than most analysts expected…

Given the prospect of ongoing chaos, investors are betting that having offered a standout growth story in recent years, the US economy is now losing some of the lustre that so dazzled delegates at the WEF in January. “To me the Davos consensus is always wrong, but this year I’ve never seen the US people so much on drugs,” says Serra of Algebris. “It was surreal.”Investing Politics: Globalization Backlash and Government Disruption! (

by )While it is easy to blame market uncertainty on Trump, tariffs and trade wars for the moment, the truth is that the forces that have led us here have been building for years, both in our political and economic arenas. In short, even if the tariffs cease to be front page news, and the fears of an immediate trade war ease, the underlying forces of anti-globalization that gave rise to them will continue to play out in global commerce and markets. For investors, that will require a shift away from the large cap technology companies that have been the market leaders in the last two decades back to smaller cap companies with a more domestic focus. It will also require an acceptance of the reality that politics and macroeconomic factors will play a larger role in your company assessments, and create a bigger wild card on whether investments in these companies will pay off.

For Markets, Trump’s Tariff Threats Are Quantitative Easing in Reverse (Sherwood News)

What quantitative easing accomplishes is that it offers a signal to the market that monetary policy is locking in to a prolonged period of providing support for the economy and financial system. Simply, if the Federal Reserve is buying bonds, it’s a helluva long way from raising rates.

To compare this to tariffs, every minute US President Donald Trump spends musing about tariffs is a minute he isn’t talking about deregulation or tax cuts. It’s a revealed preference on where his priorities lie. It’s a signal that policy is not pointed in a pro-growth direction.

Finance/Wealth (Link):

Is International Diversification Finally Working? (A Wealth of Common Sense)

Changes in US foreign policies may finally be a catalyst for European governments like Germany to lift off their fiscal spending, with a positive impact on real economic growth.

Wellness/Idea (Link):

How to Find Your “Passion” (Gorick Ng)

Gorick talks about the surprising beginning of the famous chef, Ina Garten and how she developed her passion.

But what Ina Garten shows us is that, deep down, we all secretly know if we’re following our instincts—or suppressing our instincts. And, in Garten’s case, she decided to follow her instincts:

She tasted a foreign dish—and had the instinct that maybe there was an interest she had yet to explore: cooking.

She read a cookbook—and had the instinct that maybe there’s a skill she could hone: hosting dinner parties.

She found a fledgling business—and had the instinct that maybe there’s a career she could try: food retail.

She ran a business—and had the instinct that maybe there was still something missing: creativity.

She wrote a cookbook—and had the instinct that maybe there were other forms of media she had yet to try: television.

One Chart You Should Not Miss: Lower US Treasury Yields and Upside Economic Surprises

If history is any guide, a rally in US 10-year Treasury yield could lead to positive economic surprises by about 2 months. According to Morgan Stanley, their base-case S&P 500 target price remains 6,500, “though the path is likely to be volatile as the market continues to contemplate these growth risks, which could get worse before they get better. This fits with our long-standing view that policy would likely be sequenced in a more growth-negative way to start the year before lower deficits/rates, de-regulation and less crowding out of the private economy would benefit companies and the equity market later in the year. In the bear case where growth falls off more significantly and recession becomes likely, the S&P 500 is likely to trade toward our bear case target of 4,600. We are not there, but things can change quickly and so it's useful to know the downside in the bear case to manage one's risk.”

One Term to Know: GDP Deflator

The GDP Deflator, or implicit price deflator, measures changes in the prices of all new, domestically produced, final goods and services in an economy in a year.

It helps in understanding how inflation affects the country's GDP and provides insights into the overall price level changes over time.

How does GDP deflator differ from CPI?

The GDP price deflator is a more comprehensive inflation measure (understanding inflation’s impact on the entire economy) than the CPI, which measures the price changes in a fixed basket of goods for consumption.

[🌻] Things I Learn About AI/Productivity:

We Tested Two Deep Research Tools. One Was Unusable (Session)

Even though the user experience in Gemini was better and more organized, the win goes to ChatGPT.

Gemini’s lower quality research made the output unusable. And even though I preferred Gemini’s pre-research planning process and easily exportable outputs, ChatGPT’s output was good enough to overlook some of its annoying quirks.

Ultimately, even though Gemini claims to reference more sources, it seems like ChatGPT’s multimodal analysis yields better results. Ironic for an LLM run by a search engine!

So unless ease of use is more important to you in a project than high quality information, I don’t see an instance in which you would choose Gemini’s Deep Research feature over ChatGPT’s.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.