Weekly Good Reads: 5-1-1

Deepseek Bullish Effect, Tariffs, FOMC, Trade and Geopolitics, Jevons Paradox

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work. I appreciate you for reading and taking the time!

Sharing the quote of the week:

Answers are closed rooms, and questions are open doors that invite us in.

~ Nancy Willard

You will find some useful sections below.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

👉 Interested in creating customized and diversified investment portfolios tailored just for your goals and risk profile in 5 easy steps? Please try our firm’s solution R4A. It’s free!

Market and Data Comments

[Last week my weekly change table reflected two-week changes, not a one-week change, so I corrected my mistake and updated the commentary. Thank you for your understanding.]

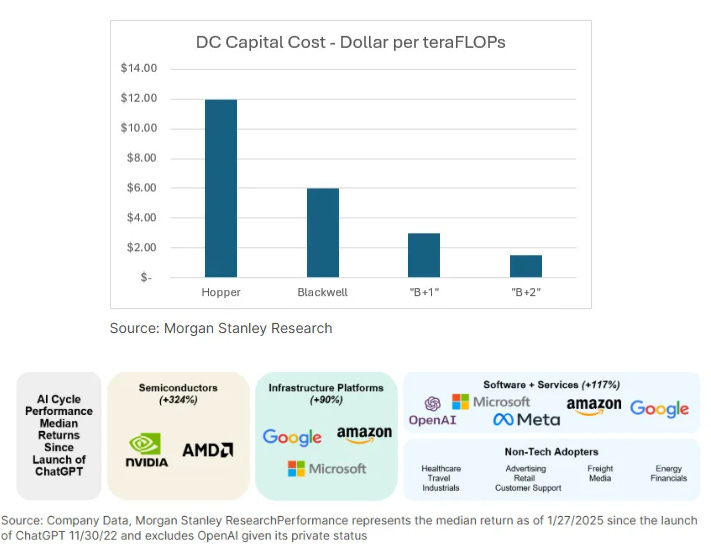

This week, the world has been awakened by the announcement by Deepseek that their “V3” and “R1” (reasoning) models are just as good as their American counterparts while their models have been produced at a fraction of their costs due to the underlying models’ efficiency innovations in the face of limited resources (chips).

While the US chipmakers’ and data centre providers’ stocks’ initial reactions were bad (Nasdaq fell over 3% last Monday), as the market questioned the previous assumptions from companies like OpenAI who said huge sums of money and computing power are needed to stay at the AI forefront, the market regained some footing as many realized AI innovations, available at a cheaper cost and with alternatives, will accelerate and widen the adoption of AI.

From a macro perspective, AI capex investments have not visibly shown up in the GDP accounts yet (thus limiting any real GDP impact) while the industry-wide adoption rate is still low at about 6% as of January 2025, indicating significant growth upside, according to Goldman Sachs.

As the “Jevons Paradox” strikes again (per Microsoft’s CEO and see “One Term to Know” for more explanation), a lower cost of compute in AI applications will lead to wider adoption by industries, companies, and research departments, hence this will boost and not hurt the growth and consumption of AI.

The S&P and Nasdaq ended up -1.0% and -1.6% but EAFE + 0.8% for the week while the dollar strengthened 0.9% and commodities largely declined except for gold. The US 10-year government bond yield rallied 8bp to 4.54%.

The market then returned to the macro data, seeing US growth continued to excel with real PCE growing 4.2% q/q saar as of Q4 2024, core inflation growing moderately at 0.16% m/m, and December personal spending growing handsomely at 0.7% m/m (likely accelerated by tariffs fear).

The Fed, as widely expected, held the Fed Funds rate at the range of 4.25-4.5%, with an overall hawkish tone as disinflation has slowed while the unemployment rate has stabilized, implying the Fed may also hold the interest rate in March. The macro outlook has become more uncertain, so to adjust its monetary stance, the Fed will take into account a wide range of information, including readings on labour market conditions, inflation pressures and inflation expectations, and financial and international developments.

The market as of now still expects a 50bp interest rate cut this year (in line with Fed’s December 2024 Summary of Economic Projections) although Bloomberg estimates 3 cuts in 2025 as it expects employment will weaken further.

Tariffs angst continue as Trump as of the time of writing has signed executive orders to impose a 10% tariff on Chinese imports and a 25% tariff on Mexican and Canadian imports, excluding Canadian energy imports which will carry a 10% tariff. While the exact implementation date and details are unknown, Canada will likely respond with their restrictions forcefully.

McKinsey’s comprehensive piece on “Geopolitics and Geometry of Global Trade” shows trade has already been reconfiguring toward geopolitically closer partners in the past 7 years (see charts below). The US has shifted away from China and towards Mexico and Vietnam, Europe away from Russia and more towards the US, while China now trades the most with developing countries. Tariffs are not likely to reverse this trend.

Elsewhere, the ECB cut rate 25bp to 2.75% as expected noting Eurozone Q4 GDP saw zero growth, lower than expected, while disinflation continues. ECB is expected to continue to cut 25bp in each meeting this year.

The Bank of England is also expected to cut interest rates to buffer the slow rate of GDP growth and on-track inflation performance. The March 2025 fiscal event (UK Office for Budget Responsibility’s updated fiscal and budget forecast) may likely prompt the Chancellor of the Exchequer to do more (cut spending) to meet the fiscal rule as the economy slows a bit more under the October 2024 tax raise.

This coming week we will monitor the US January ISM Manufacturing Index on Monday, JOLTS jobs opening on Tuesday, and January nonfarm payrolls, average hourly earnings, and unemployment rate on Friday, the Euro Area January inflation on Monday, and January composite PMI on Wednesday, the Bank of England rate decision on Thursday, and China’s January Caixin manufacturing PMI on Monday.

Economy and Investments (Links):

AI Has Rocked the Stock Market, But What Will It Do for the Economy? (Bloomberg)

The inventor’s ‘eureka’ moment takes time to diffuse through the economy. In the end, though, the gap has to be closed.

There are three ways that could happen. Optimists see AI as a driver of rising prosperity: investors win and so do workers. Pessimists worry that chatbots are more parlor trick than paradigm shift, and the billions sunk into training models won’t ever generate a return. There’s also a dystopian view, with AI making the algorithm-elite rich beyond imagining, and everyone else unemployed…

For now, all three camps are patiently waiting to be proven right. They might have to wait a while. Technology is a major driver of productivity growth, but gains are not always quick to arrive.

Your Complete Guide to Tariffs: How Much You’ll Pay, and When (CNN)

But Trump at an address to House Republicans on Monday spelled out specific items that his administration would tariff — rather than across-the-board tariffs — including pharmaceuticals, microchips and steel…

[Commerce Secretary, Howard Lutnick] suggested that the initial tariffs, coming as soon as [February 1], are “action-oriented” tariffs aimed at reducing fentanyl and illegal immigrants coming over the US border.

After DeepSeek, Tech Stocks Still Win. Here’s How AI Is Getting Reset (Barron’s or via Archive)

DeepSeek could be a catalyst for the type of shift that came to traditional computing beginning in the 1990s. Until then, the benefits of IT spending went to the makers of personal computers and servers. But over time, computing became abundant, hardware margins thinned, and the benefits began to shift to makers of software. But this shift may be more sudden because of new techniques from DeepSeek. After a brief pause following ChatGPT’s release, we may be returning to a “software eating the world” environment.

Finance/Wealth (Link):

and )Wellness/Idea (Link):

How to Make and Eat Smørrebrød (

)Smørrebrød {open-faced sandwiches from Denmark] are served across all strata of society, from extremely fancy restaurants to working-class lunch counters, where they often come accompanied by a fist-size meatball or a fried fish cake. You can experiment and take some liberties in creating your own open-faced sandwiches. For instance, if you have a fantastic ripe avocado, go ahead and slice it to add on top, even though that is not a traditional Scandinavian garnish. However, there are some rules to be followed if you want this to count as an authentic smørrebrød experience rather than a plate of avocado toast.

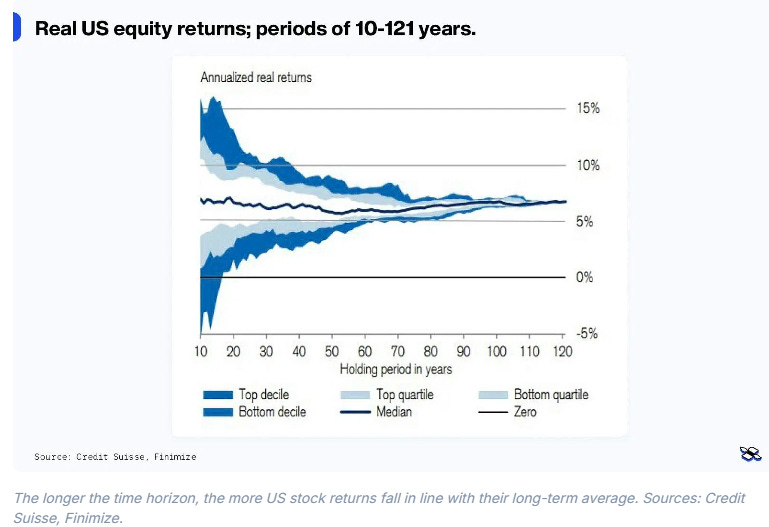

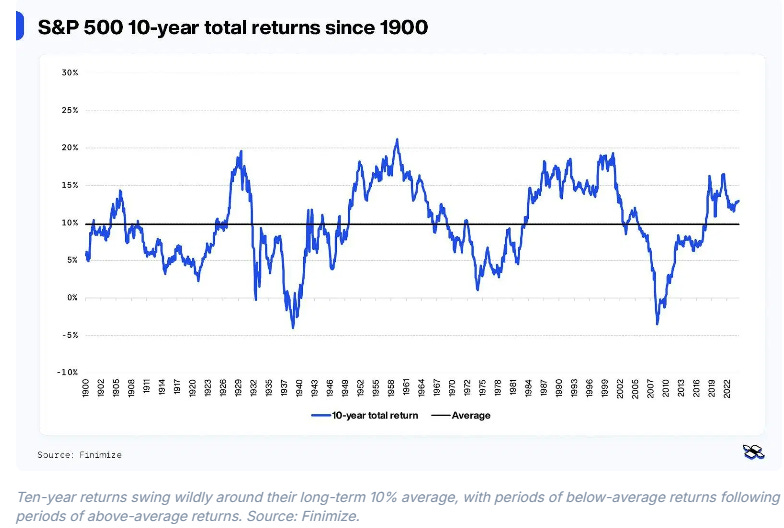

One Chart You Should Not Miss: Expected S&P 500 Returns in the Next Decade

The lesson here is: If you can hold the stocks over a very long term (think 70 years), then US stocks’ real return falls in line with their average at about 6% (after inflation). Over ten years, returns of stocks can vary a lot from their average, from -5% per year in real terms to +15%. Stocks are currently starting at a high valuation and record profit margins, which can set investors up for disappointment. Stay diversified across regions, sectors, styles, and asset classes.

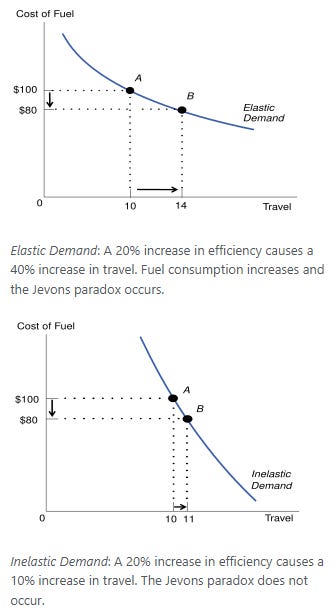

One Term to Know: Jevons Paradox

Jevons Paradox has become the new phrase and table stakes for anyone wading into the DeepSeek discourse, with traffic to its Wikipedia page jumping 200x to 122k this past week, according to Sherwood/Chartr.

Satya Nadella, Chairman and CEO at Microsoft in his recent LinkedIn post said:

Jevons paradox strikes again! As AI gets more efficient and accessible, we will see its use skyrocket, turning it into a commodity we just can't get enough of.

The term originated in 1865 by English economist William Stanley Jevons: greater efficiency in the use of any given resource can result in increased demand for that resource.

His example was coal and the Watt steam engine. When the steam engine, which burned much less coal than its predecessors, was invented, coal demand jumped, as the steam engines were used in a wide range of applications.

In the AI case, a lower cost of compute in AI applications can lead to a wider adoption by industries, companies, and research departments, hence this will boost and not hurt the growth and consumption of AI.

The two graphs below illustrate the much bigger effect on demand (X-axis) when the demand curve is elastic vs. inelastic.

[🌻] Things I Learn About AI/Productivity:

The Generalist’s Productivity Stack (

)I particularly like tip #7: Make Unbroken Time Sacred

If you have autonomy over your schedule, set aside three hours daily for deep, focused work. Treat this time as sacred—only to be broken in the rarest, most unforeseeable circumstances.

In my experience, it takes at least 30 minutes for your brain to sink into true focus. Simply knowing you have an appointment within an hour can stop you from reaching this place of deep thought, and, of course, even once you’ve reached it, you can be shaken from it in an instant.

Why DeepSeek Is Bullish for the World (John Mauldin)

This is not about China. I applaud the creativity of the DeepSeek developers and especially their ability to drive down costs. I am amazed they made it truly open-source and revealed everything.

I and others have maintained that eventually AI will be a commodity. And just like the world would be massively better if some scientist figured out how to make $10 oil from garbage, even though it would devastate energy stocks, the world would be better off with cheap artificial intelligence, especially if it used only 10% of the power. To think that the US could maintain control over AI is like thinking we could maintain control over energy because we found oil in Pennsylvania. AI will be everywhere and cheap.

Combined with the other new technologies that will change the way we manufacture chips and power AI, what DeepSeek just did is massively bullish for humanity.

ChatGPT vs. Claude vs. DeepSeek: The Battle to Be My AI Work Assistant (WSJ or via Archive)

The author’s take: So for those keeping track: Claude is my go-to for project planning, clear office and document tasks and it’s got a great personality. ChatGPT picks up the slack with real-time web knowledge, a friendly voice and more. DeepSeek is smart but, so far, lacks the features to get ahead at the office.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.