Weekly Good Reads: 5-1-1

US Core Inflation, Spending and Debt, Bank Earnings, Trump's "Day 1", US Immigrants, Clean Energy, Money and Happiness

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you for supporting my work. I appreciate you for reading and taking the time!

Sharing the quote of the week:

I love it when things don’t work; it leaves room for something else that’s going to happen next. ~ Amy Sherald (Artist)

You will find some useful sections below.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

My most recent post in case you miss it:

👉 One more: May I invite you to try our firm’s digital investment software for creating customized portfolios tailored just for your goals and risk profile (for free)?

Market and Data Comments

US assets have been rallying this past week except for the US dollar, which fell 0.3% for the week. The S&P 500 rebounded 2.9% last week, the best week since the US election, with VIX falling almost 4% to 16% as of last Friday, all helped by a rally in the US 10-year government bond yield, falling 13bp to 4.63% for the week.

A better-than-expected December US core CPI data (0.23% m/m and 3.2% y/y, 3.3% y/y prior) have buoyed all assets (US Dec CPI at 2.9% y/y). US financials earnings from JP Morgan, Goldman, Morgan Stanley, Citibank, Wells Fargo, to BlackRock jumped from a year ago, reflecting more buoyant investment banking activities and a steepening yield curve (long rates rising faster than short rates) (see Econ/Invest #2).

Another reason for the stock market optimism is the continuous spending of Americans. According to the Bank of America Institute, US consumers finished 2024 strong, with December card spending per household up 2.2% y/y and all income levels of households spending more. 2024 was a solid year for consumers, with December card spending per household up 2.2% y/y - see graph below.

At the same time, faster asset and income level growth relative to debt level has brought US household debt to asset level to a 50-year low (around 11%).

The IMF kept its 2025 economic growth for the world at 3.3% but revised up both the US and China's real GDP growth for this year. Inflation should be down to 3.5% next year, drawing a close to the disruption from the Pandemic to the Russian-Ukraine war. Amongst the major economies, the US is operating above its economic potential while Europe and China are below (Europe is facing structural problems and higher levels of gas prices while China may be in a debt-deflationary trap) (see Econ/Invest #1).

Still, inflationary pressures resulting from strong domestic demand helped by fiscal spending but restricted supply (due to imminent change in immigration and trade policies) would prevent the Fed from cutting rates meaningfully this year, while the US dollar and growth could pull further away from the rest of the world.

At the same time, the US (public) debt to GDP has already exceeded that in World War II (now at 98%) and could proceed to 132% of GDP by 2034 (worst case at 145% and best case at 125%), according to Bloomberg. Given US structural challenges—interest costs (rising as a portion of spending), entitlement spending, and an ageing population — the US fiscal path remains unsustainable.

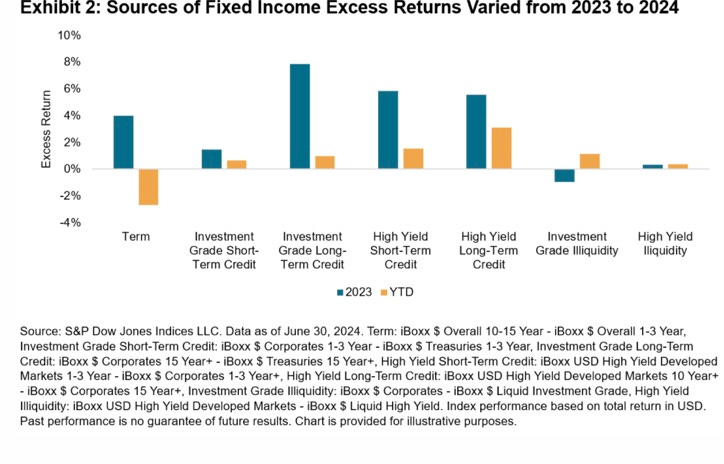

This leads us back to the US 10-year government bond yield, the current barometer for all global assets. S&P Global looked at the excess returns over the benchmarks of active bond managers, and for the first half of 2024, taking on more US interest rate risk, i.e., moving from short-term to longer-term bonds, a traditional source of excess returns, has clearly hurt active managers (see the “Term” bars) this year. Moving down the credit spectrum, another source of potential excess returns has continued, but the high yield spread is at a historically tight level.

The uncertainty and rising term premium in bonds may mean investors either hold more cash or push into equities, especially in the US, where the return on investments, fuelled by innovation and productivity gains, outperforms relative to the rest of the world. The US, especially large-cap, remains the main investment focus.

In this coming week, we will monitor President Trump’s inauguration on Monday (and his “Day 1” policy announcements, see a table below from Barclays what Trump has said) and ongoing Q4 US company earnings announcements, the World Economic Forum at Davos this week, the December CPI in Japan on Thursday, and the Bank of Japan monetary policy meeting on Friday.

Economy and Investments (Links):

Some divergence between large economies has been cyclical, with the US economy operating above its potential while Europe and China are below. Under current policies, this cyclical divergence will dissipate. But the divergence between the US and Europe is more due to structural factors, and the disconnect will linger if these are left unaddressed. It reflects persistently stronger US productivity growth, particularly but not exclusively in the technology sector, linked to a more favorable business environment and deeper capital markets. Over time, this translates into higher returns on US investment, increased inbound capital flows, a stronger dollar and US living standards pulling away from those of other advanced economies. For China, it is notable that potential growth is now more like that of other emerging market economies.

The Big Takeaway From Bank Earnings (Barron’s or via Archive)

Big firms’ investment banking businesses and trading desks are humming. That’s thanks to a strong economy that has already boosted earnings, interest rates that are lower than a year ago, and a jolt of post-election investor enthusiasm.

Part of what is buoying confident investors’ thesis in the banking industry—and for a pickup in mergers and acquisition activity in particular—are lofty hopes of lighter antitrust regulation to come. Bankers hadn’t been doing much for a period as higher rates and perceptions of more stringent regulation dampened companies’ willingness to carry out big deals.

I remain highly uncertain both about what Trump will do and about how it will be received. But I would argue that the fact that he inherits an economy in such good shape is actually a problem for his agenda.

Finance/Wealth (Link):

How Much Money Buys You Happiness in Retirement? (FT or via Archive)

My conclusion is two-fold. First, money can buy you some happiness, but less than you might think. There is plenty of scope to give it a leg up by other means: yoga, fly-fishing, relationships, whatever. Second, if you want to make yourself pointlessly anxious, anchor your retirement aspirations firmly to what you earn as a full-time toiler.

Behavioural researchers at data company Morningstar therefore encourage private investors and their advisers to follow a different approach. The first step is to understand that numeric savings targets are a means to an end, not an end in themselves. The next stage is to define broad goals, such as buying a holiday home that kids and grandkids can use. The final task is to identify core emotional needs, for example: “connection to loved ones”.

+ Related: What Most People Get Wrong About Money (Graham Weaver)

A very sensible read.

…the age-old question: can money buy you happiness? Yes, I believe it can. But the real magic of wealth, and what will truly make you happy, is the peace of mind, freedom, and reduced friction that money can provide.

Wellness/Idea (Link):

What Homeowners and Renters Need to Know After a Wildfire (Vox)

We think disaster will only happen to others, and it’s not true. I experienced an apartment fire on my floor a few years ago without any renter’s insurance but luckily our apartment management helped me out. It is good to be prepared. My heart goes to the LA people living through this 💖.

Whether you’ve been impacted by a fire or flood, the advice is the same: Document the damage and contact your insurance company as soon as possible, Hooker says…

For those without homeowners or renters insurance [also with home insurance], you can apply for relief through FEMA. Fill out the application at DisasterAssistance.gov, on the FEMA app, or by phone at 1-800-621-3362.

…[check] if your state or city is offering disaster relief. Aid organizations like the American Red Cross and the Salvation Army operate shelters and service sites offering access to caseworkers to help with financial assistance. These disaster assistance centers are where you can talk to case managers to determine what forms of aid you’re eligible for.

To find immediate shelter housing, DisasterAssistance.gov has an emergency shelter page with resources for housing. The California Office of Emergency Services also has a list of available shelters. You can learn about other disaster assistance programs and housing and rental assistance information at a Disaster Recovery Center. To find one near you, enter your address in FEMA’s DRC locator.

One Chart You Should Not Miss: Immigrants in the US

In California, Texas, Florida and New York, immigrants account for about one in five residents [in general immigrants account for 1 in 5 of US workers). Within those states, they tend to favor big cities. Immigrants make up more than half of Miami’s population and about 38% of New York City’s population.

A 2024 Bloomberg News analysis of immigration court data found that the 1.8 million asylum seekers and refugees who landed in the US in 2023 overwhelmingly chose to settle in Democratic-leaning counties. Much like in previous generations, migrants seem to be favoring places with growing local economies, bolstering the labor force in places that are already thriving.

From Bloomberg’s research, immigrants have an insignificant long-term impact on wages in the US, in general, help local governments raise more tax revenue than costs, and are responsible for more than a third of the new patents in the US in the past three decades, according to the NBER economists. Federal Reserve chairman Powell said that labour supply from immigrants has helped the labour market to do better than expected. Most economists agree a mass deportation of illegal immigrants (estimated at 11 million) could cost over $150 billion and no or lower economic growth in the next 4 years.

One Term to Know: Clean Energy (and the difference from Renewable Energy)

According to Iberdrola (a global leader in renewable energy operating across Europe, Latin America, and Japan), clean energy comes from generation systems that do not produce any kind of pollution, notably greenhouse gases like CO2, which cause climate change.

While clean energy is often lumped together with renewable energy, they are not the same as renewable energy can cause pollution, for example, biogas and biodiesel are renewable sources of energy that emit greenhouse gases on combustion, while clean energies do not pollute.

Most clean energy is also renewable. Common types of clean energy include solar, wind, hydro, geothermal, marine, and tidal. The advantages of clean energy are, apart from being a solution towards climate change as clean energy does not emit carbon (but from natural sources), job-creating, does not rely on volatile fossil fuel imports or affected by geopolitics, and is cost-effective.

Look at the dramatic decline of the price of electricity from renewable sources of energy:

[🌻] Things I Learn About AI/Productivity:

The End of Tutorials? This Free AI Changes How You Learn Software Forever | Google AI Studio (Kevin Stratvert)

After trying Google AI Studio and interacting with AI to clarify my Excel formulae, I believe building an Excel formula is much easier.

Go to Google AI Studio. log in to your Google account. Choose the Gemini option and then click on “Stream Realtime”.

In this example, AI Studio helps me to build a formula to extract “IBM” from [IBM Equity] assuming these words are in cell A2. The AI, when asked to spell out the formula including the brackets, told me the exact formula to write and then explained the concept behind it: LEFT(A2,FIND(" ",A2)-1). I often use Len and Right or Left functions together, but this AI immediately told me using the “Find” function is much more effective. The AI adds a “-1” at the end of the formula to ensure I have no space after the first string of words 👍. Try it, it’s free!

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.