Weekly Good Reads: 5-1-1

Bondfire, Rate Cut Expectation, On Bubbles, Crypto, Biggest of S&P 500, Sovereign Debt, Local LLM

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner sharing something interesting and topical in investing, the economy, wellness, and AI/productivity.

Thank you to my dear readers for supporting my work. I appreciate you for reading and taking the time!

Sharing the quote of the week:

When you have exhausted all possibilities, remember this: you haven't.

~ Thomas Edison

You will find some useful sections below.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

My most recent post in case you miss it:

👉 One more: I am inviting you to try our firm’s digital investment software for creating customized portfolios tailored just for your goals and risk profile (for free):

Market and Data Comments

If this Weekly reads like a “Bond special”, it is!

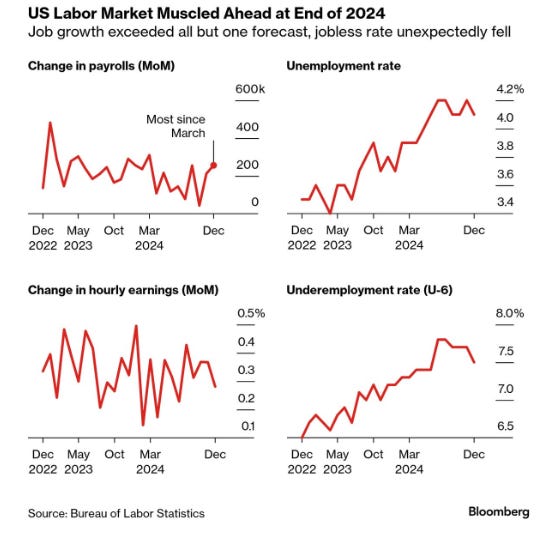

Before the shock from the US payroll data last Friday, there were already surprising upsides to the ISM PMI services data and the December FOMC minutes showing inflationary risks have risen (as governors incorporate the impact of Trump’s likely economic policy) while unemployment risk has fallen. All around rise in commodity prices such as oil, copper, and gold also reflect strong economic growth and inflationary pressure.

December US payrolls rose 256k (consensus was 165k), with private payrolls up 223k and with little revision to prior months. The unemployment rate fell to 4.1% while payroll earnings rose at a 5.9% q/q saar clip in 4Q. The Fed’s focus will be back to inflation. The market now prices the next 25bp of Fed cut in September 2025 instead of June.

With average past 5Y inflation at 4.2%, inflation getting stickier, rising consumer inflation expectations, the stock market priced almost for perfection, stocks have become more vulnerable to the jolt from higher bond yields, resulting in a drawdown in S&P 500 of almost 2% last week and -0.9% YTD (see Econ/Invest #1.)

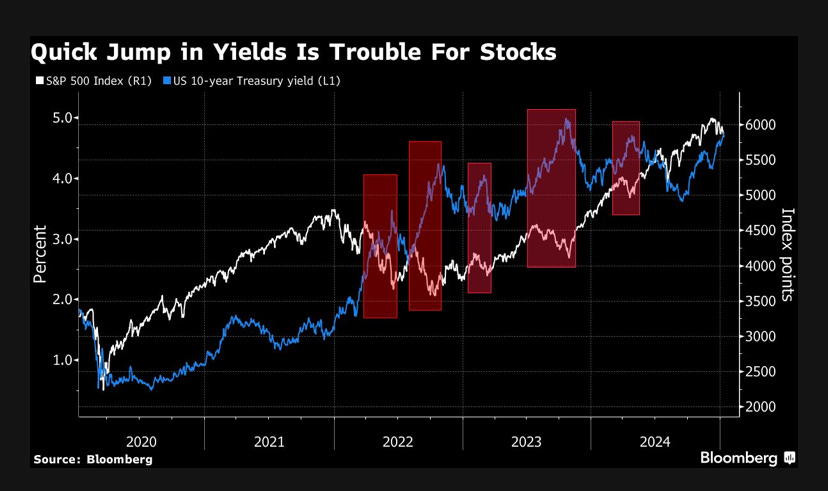

The US 10Y government bond yield jumped 16bp to 4.76% (relatively faster than the 2Y yield which rose 10bp to 4.38%), showing a bear steepening of the yield curve.

Whenever yields rise rapidly, stocks tend to drop, and the 10Y yield is rapidly approaching 5% and the 30Y yield also breached 5% last Friday. This is unusual: government bond yields are usually flat or modestly higher in the months after the Fed started a string of rate cuts. US bond yield has sold off for 53 months, the longest period since 1983 (see below 3 charts).

Rising US yield has pushed the US dollar higher (see below RHS chart.)

Surging bond yields are not confined to the U.S. due to the macro backdrop of rising inflationary pressures and debt burden and the uncertain Trump policies (China, in contrast, has seen declining bond yields as deflation threatens). Rising inflation concerns and fiscal trouble in the UK pushed the 10Y Gilt yield up 25bp and the UK stock market down over 4% last week.

So far, US high-yield and high-grade corporate bond spreads are relatively steady but they are historically tight.

While the Magnificent 7 stocks, the area that has produced strong profits and cash flow and a direct beneficiary of AI optimism pushing their S&P 500 index weight to a high of 33% currently, a 5% bond yield makes stocks super sensitive to any earnings disappointment. There is no better time to focus on the quality of stock selection, diversification, and valuation. If you have been concerned about market bubbles, please read Econ/Invest #3 and Finance #2.

In this coming week, we will monitor the US Q4 stock earnings reports (starting with the large banks on Wednesday), US December PPI on Tuesday, CPI on Wednesday, retail sales on Thursday, housing starts on Friday, UK December CPI on Wednesday, Euro Area December CPI on Friday, China’s December exports on Monday, and Q4 GDP, December retail sales, industrial production, and 2024 fixed asset investment on Friday.

Economy and Investments (Links):

In the U.S., higher yields present a tough hurdle for equities. The S&P 500 index trades at 22 times expected forward earnings, wrote Jason De Sena Trennert, head of Strategas Research. That heady valuation also presumes another year of double-digit earnings growth on top of yet-to-be-reported final 2024 numbers.

Further, it’s difficult to justify P/E expansion without a meaningful decline in long-term interest rates and another period of “irrational exuberance” as seen in the 1990s. Trennert adds that odds of the latter might be greater than presumed given the incoming administration’s anticipated deregulation and more pro-business stance. (It should be noted he has said he is open to accepting a position in the Trump administration.) But given the struggles stocks have shown when the 10-year Treasury tops 4.50%, “discretion may be the better part of valor in 2025,” he concludes.

In 2025, countries will still be facing the legacy of high borrowing during Covid, and would need to carry out fiscal consolidation to put public debt “on a more sustainable path”, she said. “It has proven very difficult for fiscal policy to act promptly, given public sentiments, and that takes us to what is our main challenge at the fund — and it is tackling this low growth, high debt conundrum,” she said.

On Bubble Watch (Howard Marks)

In the last two years, it’s happened for the fifth time. The S&P 500 was up 26% in 2023 and 25% in 2024, for the best two-year stretch since 1997-98. That brings us to 2025. What lies ahead? The cautionary signs today include these:

the optimism that has prevailed in the markets since late 2022,

the above average valuation on the S&P 500, and the fact that its stocks in most industrial groups sell at higher multiples than stocks in those industries in the rest of the world,

the enthusiasm that is being applied to the new thing of AI, and perhaps the extension of that positive psychology to other high-tech areas,

the implicit presumption that the top seven companies will continue to be successful, &

the possibility that some of the appreciation of the S&P has stemmed from automated buying of these stocks by index investors, without regard for their intrinsic value.

+ California Fires Expose a $1 Trillion Hole in US Home Insurance (Bloomberg or via Archive)

The glut of homes in increasingly fire-prone places has created an insurance crisis in California, with many big insurers pulling out of the state to avoid more losses. Nearly 500,000 Californians have turned to the state’s insurer of last resort, the FAIR Plan, which has doubled in size over the past five years. The state is now exposed to nearly $458 billion in potential damage, a figure that has nearly tripled since 2020…

Private insurance plans will be more adequate, meaning they will cover more damage, than the FAIR Plan. They are typically “replacement cost value” plans, compared with FAIR’s “actual cash value” plans. But even private insurance plans aren’t always enough to fully reimburse a homeowner, given rising rebuilding costs, especially after a widespread disaster. Klein has suggested 80% of Americans don’t have enough home insurance.

Finance/Wealth (Link):

Crypto is for Criming (Krugman Wonks Out)

There Are Idiots: Seven Pillars of Market Bubbles (Arcadian Asset Management on Bitcoin)

1 THERE ARE IDIOTS. Look around.

2 Everybody ought to be rich.

3 Nobody knows anything.

4 A fanatic is someone who can’t change his mind and won’t change the subject.

5 The more confusion, the better.

6 Number go up.

7 This time is different.

All these can apply to Bitcoin, no?

Wellness/Idea (Link):

The Unusually Strong Force Driving Apocalyptic Los Angeles Wildfires (Atlas Obscura) - My heart goes out to our LA friends going through this ( ˘͈ ᵕ ˘͈♡)

This was an exceptionally well-predicted event from a meteorological and fire-predictive services perspective,” Daniel Swain, a climate scientist at the University of California Los Angeles, said Wednesday during a livestream.

The winter months are typically when Southern California quenches its thirst with rainfall, but the past few weeks have been unusually dry, and little snowfall has accumulated in the surrounding mountains. The NIFC also noted that temperatures were “an impressive two to six degrees [Fahrenheit] above normal in most areas” in December, allowing vegetation like grasses and chaparral to readily dry out and serve as fuel.

+ 33 Ways To Improve Your Life, Japanese Style (Mr. Porter)

#21. Revel in being cheap

Cheap is not a dirty word in Japan – and it’s not a byword for bad quality either. “There’s a word in Japanese called puchipura, which means cheap cosmetics that are still high quality,” Miyake says. “It’s about adjusting your lifestyle to your budget, but still enjoying luxuries when you can.”

One Chart You Should Not Miss: Useful Decomposition Data of S&P 500

The largest companies in the S&P 500 by:

Market Cap (Apple)

Net Income (Berkshire Hathaway)

Revenue (Walmart)

# of Employees (Walmart)

One more: HighestAmount of Debt (Ford)

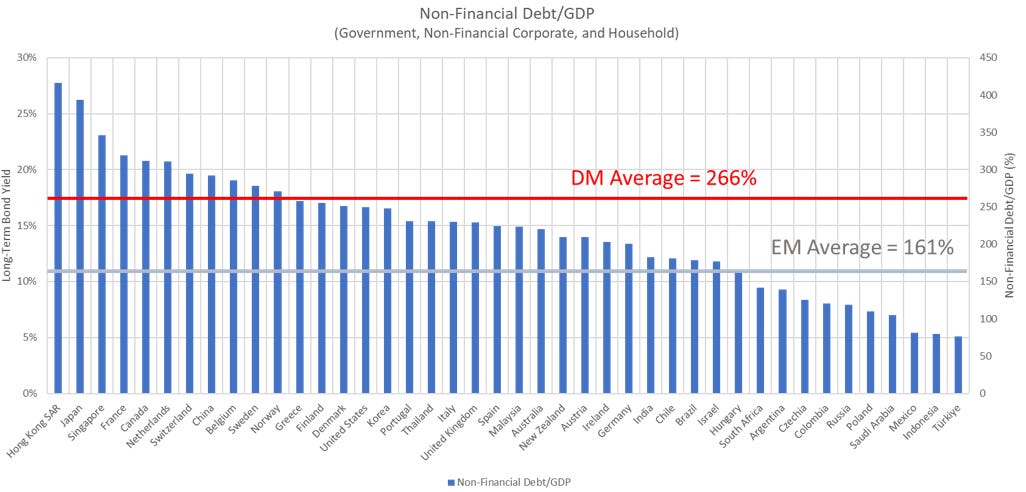

One Term to Know: Non-Financial Debt (by BIS)

The non-financial debt is the total amount of debt owed by the non-financial sector of a country. It includes the government sector and the private non-financial sector, which is further broken down into households and non-financial corporations. The data include debt securities, loans, currency, and deposits.

The Bank for International Settlements (BIS) has a data set with over 40 countries’ debt series, updated quarterly.

From the above chart, one developing country, China, has exceeded the DM average (which includes the data for banking centres such as Hong Kong, Singapore, and the Netherlands). U.S. is sharply approaching the DM average. EM average is still substantially below that of the DM.

This is one of the most comprehensive data sources of total debt for countries that I frequently refer to.

[🌻] Things I Learn About AI/Productivity:

- )

Run a Cutting-edge AI Model on Your Laptop (Paul Couvert)

This is a game-changer as you can maintain privacy as you interact with your own machine, receive access to cutting-edge AI technology, and run the Phi-4 model offline and efficiently, any time of the day.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.