Weekly Good Reads: 5-1-1

Economic Risks, Equity Factors, 2025 Surprises and ETF Trends, Investing Tenets, Cancer and Alcohol, Selling Options

Happy New Year ✨✨✨!!

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

Thank you to my dear readers for supporting my work. I appreciate you for reading and taking the time!!

Sharing the quote of the week:

With the new day comes new strength and new thoughts.

~ Eleanor Roosevelt

You will find some useful sections below.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

👉 One more: I am inviting you to try our firm’s digital investment software for creating customized portfolios tailored just for your goals and risk profile (for free):

Market and Data Comments

December 2024 was a month most stock participants would rather forget, with the S&P 500 dropping 2.5%, sectors including utilities, industrials, energy, materials and real estate falling over 8%, and only info tech, consumer discretionary, and communication services having gains.

With market liquidity normalizing next week and relatively little significant economic data, investors are re-evaluating market risks and allocation as the US will have a new government, stocks have had two consecutive years of 20%+ gains, the Fed signalling fewer rate cuts (two in 2025), and last-mile inflation stalling at a higher level (November core PCE at 2.8% yoy).

US stock exceptionalism is a term often heard in 2024, marked by surprising consumer strength, continued AI optimism and spending by Big Tech broadening to traditional industries, cashflow generation, productivity gain, continuing Fed interest rate cuts, and expectation of Trump’s tax cuts and deregulation. As Bridgewater mentioned, $1 invested in the S&P 500 in 2010 is now worth $6.

Momentum and quality equity factors (see chart above), concentrated in the U.S., beat the S&P Index in 2024. The S&P 500 performance has been driven mainly by a step-up in earnings growth (red line) and a steady multiple expansion (green bars) (see graph below), all the while the US bond yield has been rising (now at 4.6% despite the Fed easing) and consumption momentum is expected to slow as the unemployment rate creeps higher and if stock prices reverse.

The US 10-year government bond rose 69bp while the Treasury bill (1-3m) dropped over 1% and the 2-year yield hardly changed in 2024 (see Weekly Change Table below).

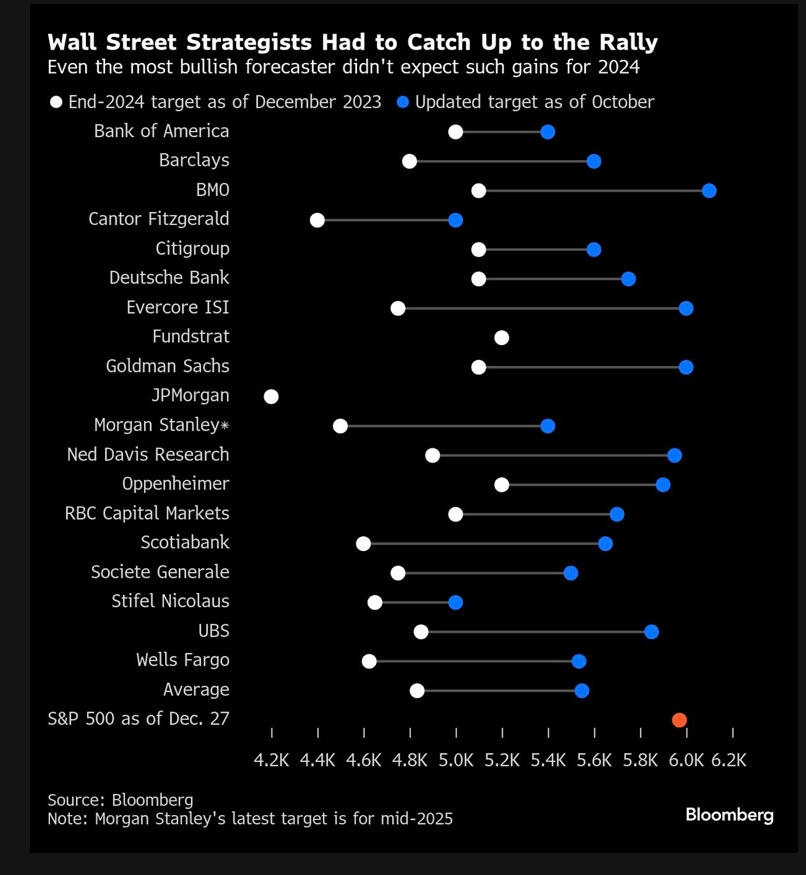

Look at the chart below: Wall Street strategists had to catch up to the S&P rally, and no analysts foresaw the gains in 2024.

As various organizations release their 2025 forecast including FT, Washington Post, Pensions and Investments, Axios (here and here (from the readers)), or The Economist (on industry trends), the common theme is growth will be impacted, stocks and bond yield volatilities will rise as Trump balances his election promises in important economic areas including trade, fiscal, and immigration against economic reality and reactions from trading partners. This time, policy uncertainty is on everyone’s mind. Axios summarizes it well:

The global economy is already showing cracks that Trump threatens to widen. Ripple effects from the incoming administration's policy could hit financial markets, warp global trade patterns and reignite inflation that policymakers worked to crush.

While the US has the tailwind of strong economic momentum, its trading partners are facing slower growth and potentially higher inflation (US/Europe) or deflation (China), making the investing environment more treacherous. Understanding what you are investing and their valuation and watching the bond yield and credit spread are crucial.

Morgan Stanley’s “Top Ten Surprises for 2025” is always refreshing to read about what could happen instead—less US fiscal deficit but more in Germany and China, lower US growth, lower rates and therefore weaker dollar, more US disinflation, less cuts in the U.K., etc. Also, could the Trump era lower the temperature of geopolitics as in his first term?

For business trends, a couple of important areas to watch are energy consumption and infrastructure building (data centres, green energy) which can result in more demand for copper, steel, and gold while those metals for EVs may be more uncertain as EV sales do not meet expectations.

This coming week we will monitor the FOMC meeting minutes on Wednesday, the December nonfarm payrolls, the unemployment rate, and average hourly earnings in the US, the Euro Area Composite PMI on Monday, and the December CPI and unemployment rate on Tuesday, and China’s CPI, PPI, money supply, and aggregate financing on Wednesday.

Economy and Investments (Links):

So for the first time in many years, investors have what they call “two-way risk” in the Fed policy that drives the bond market and underpins global asset prices. The central bank might be able to keep on cutting — the hunch is that this would be Trump’s preference. But it’s not outlandish to suggest it might start raising rates again instead. This could get lively…

“We need to be humble and say, ‘I don’t know where this is going to break’,” said Peter Fitzgerald, chief investment officer for macro and multi-asset at Aviva Investors in London. “The key is, don’t get overconfident.”

The momentum strategy, an approach widely used by quantitative traders and backed by academic research, captures the tendency for market trends to persist for a while, whether it’s because more investors are jumping in or are late to absorb new information. It reallocates into recent winners in every rebalance, helping it capture medium- to long-term trends.

That has happened this year. In addition to betting big on tech, momentum managed to break out of its summer doldrums by adding more cyclical names that ended up profiting from Donald Trump’s victory, says Bruno Taillardat, head of smart beta at Amundi.

The strategy’s whopping gains have intensified worries that momentum has now become self-fulfilling in stocks, especially with the growing dominance of passive funds.

Finance/Wealth (Link):

Active ETFs, Dual Share Classes and the ‘Holy Grail’ of Wrapping Private Assets in Focus for 2025 (Pension and Investments)

Efforts to wrap private assets into ETFs likely “will be one of the most closely followed stories in the industry next year,” Geraci said, adding that “issuers are working overtime” trying to figure out how to wrap private assets — such as private credit, private equity and private real estate investment trusts — into an ETF.

“I think this will be the next frontier of ETF innovation,” he said.

Balchunas also cited private assets as an area to watch.

“This is like the Holy Grail,” he said during the ETFs in Depth event. “Can you put something illiquid into something liquid? Well junk bonds kind of did it, but this is (an) earthquake filing from State Street and Apollo.”

Wellness/Idea (Link):

Alcohol and Cancer Risk (US Department of Health and Human Services)

+ Related: Surgeon General's Suggestion to Put a Cancer Warning on Alcohol is Long Overdue, Doctors Say (NBC)

One Chart (Letter) You Should Not Miss: Ten Investing Tenets

Courtesy of “The Big Picture” - the below letter was Authur Zeikel sharing his [evergreen] investing insights with his daughter in 1994:

Arthur Zeikel was a founding principal of Standard & Poor’s/InterCapital, Inc., and served as Chairman of the Board. He eventually became president of Merrill Lynch Asset Management, leading the division with a value-oriented approach and a focus on long-term fundamentals. He was an adjunct professor at NYU STern School of Business. He co-authored Investment Analysis and Portfolio Management, now in its fifth edition.

One Term to Know: Selling Options/ Volatility

Options, calls and puts, are derivatives allowing the purchaser the right (but not the obligation) to buy or sell an underlying asset at a predetermined price (strike or exercise price) within a set time frame. The volatility of the asset, time to maturity, and the asset’s current prices all affect the value of the option.

While the maximum losses when buying calls and puts are limited to the option premium paid, selling options incur different benefits and risks.

Covered calls or cash-secured puts are popular income-generation trading strategies. Naked calls and puts (with no underlying asset or cash) are more risky and are for more sophisticated traders.

In the case of covered calls, the investor will purchase a stock and sell calls on a share-for-share basis.

Losses occur in covered calls if the stock price drops below the breakeven point. If the stock price rises above the effective selling price of the covered call, then potential gains are given up.

Assuming the purchase price is $39.30, the call premium received is $0.9 with the strike price at $40.

Covered calls work best in a stable and slightly bullish market, especially when the stock price does not rise significantly above your strike price, which means you get to keep the stock (which is still rising) and pocket the premium you received as extra income.

Covered calls can also reduce losses in a slightly bearish market when your stock prices fall slightly (but you are still happy to own) but the call premium helps to offset some of the losses.

Options sellers should be prepared to sell their underlying position when the call is exercised, thus giving up potential gains. If your outlook on the stocks is very positive, covered calls are not appropriate.

Knowing the advantages and disadvantages of covered option strategies and your maximum profit and losses and breakeven points are important considerations before deploying any option strategies.

[🌻] Things I Learn About AI/Productivity:

What Just Happened? (One Useful Thing by

)2024 AI Tools Report (There is an AI for that)

15 Tech Trends to Watch Closely in 2025 (CB Insights)

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

Thank you for another insight-packed issue! Wrapping private assets into ETFs is one of the most talked about topics (with tons of different opinions) among fund industry participants these days.