Weekly Good Reads: 5-1-1

Fed's Pivot, Dot Plot, Elon Musk, Market Forecasting, Debt Ceiling, Healthy New Definition

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

The next version of Weekly will come on January 4, 2025.

Sharing the quote of the week:

He who has a 'why' to live for, can bear almost any 'how'.

~ Friedrich Nietzsche

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

👉 One more: I am inviting you to try our firm’s digital investment software for creating customized portfolios tailored just for your goals and risk profile (for free):

🙌 Thank you so much for reading and supporting my work, and I would like to wish you a wonderful and peaceful holiday season and the best of 2025 🤞!!

Market and Data Comments

The biggest economic news this past week was the FOMC announcement of a 25bp interest cut of the Fed Funds rate to 4.25%-4.5%, with the Fed’s dot plot showing a more gradual and shallower rate-cut path. For 2025, the median dot sees the Fed Funds rate ending at 3.9% (50bp cut), 3.4% (50bps cut), and 3.1% (25bp cut) respectively at the end of 2025, 2026, and 2027. The median dot for the longer-run neutral interest rate was raised slightly to 3.0% (vs. 2.9% prior).

This was accompanied by a higher projected core inflation rate vs. the September projection (2.8%, 2.5%, 2.2%) for 2024 to 2026, a lower unemployment rate (4.2% end of 2024, 4.4% prior), and a higher end-2024 GDP at 2.5% (2.0% prior). The projections of lower inflation and steady GDP growth did not incorporate sharp tariff increases or potential large cuts in government spending from the new Department of Government Efficiency (DOGE).

The bottom line: The Fed thinks it will take longer (not until 2027) to get back to the 2% inflation target (implying the potential inflationary non-transitory impact and uncertainty from Trump’s tariffs) and further rate cuts will depend on inflation’s further progress, i.e. the Fed has shifted its focus from employment back to inflation and baked in 2 instead of 4 rate cuts of 25bp in 2025.

The ‘Hawkish Cut” from the Fed, combined with “dovish than expected central bank signals from the BoE and the BoJ, and China's one-year bond yields dropping below 1% for the first time since 2009, the Fed's hawkishness drove USD stronger: with the Bloomberg DXY dollar index continuing to break out of the range where it has been trading over the past two years (Barclays).”

The S&P 500 dropped 3% on the day of the Fed’s announcement and the US 10-year jumped almost 12bp to 4.564% (but declined to 4.523% on Friday). Note that some view the 4.5% bond yield threshold presents headwinds for stocks.

However, the lower-than-expected November core PCE (0.11% vs. 0.26% prior), the Fed’s preferred inflation gauge, provided some relief to the market on Friday. The year-on-year rate at 2.82% rose slightly from October (2.79%).

For the week, the US S&P 500 and Nasdaq dropped about 2%, while the small-caps (Russell 2000) dropped 4.5%, and the US 10-year government bond yield rose 13bp. The high yield spread widened 20bp while the VIX moved up 4.55% to 18.36% and the MOVE index jumped 6 points to 91.8.

Apart from the Fed’s pivot, the market got hit by another unexpected uncertainty coming from the political wrangling and a storm of tweets from Elon Musk on the debt ceiling (see One Term to Know below). In the early hours of Saturday, the Senate passed the spending bill (approved earlier by the House) extending government funding to March 14, 2025, and averting a government shutdown in January. The issue (raised by Trump) of suspending or raising the debt ceiling was not included, kicking it to the next Congress.

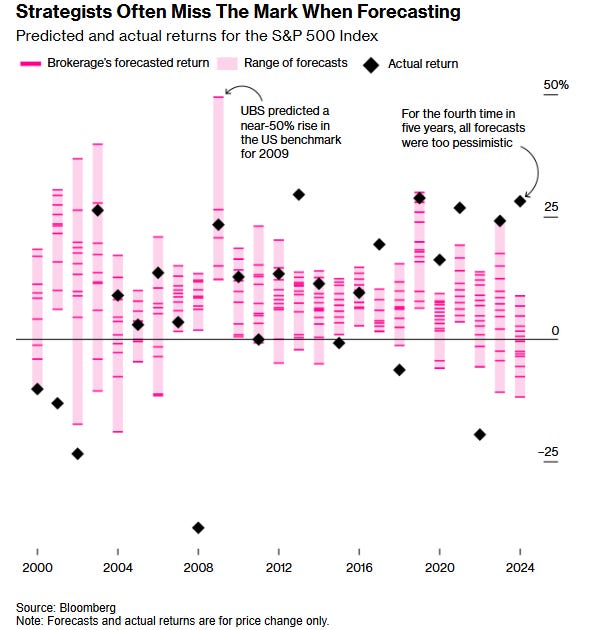

On another note, as the Wall Street stock prediction for 2025 has been out (averaging +9%), Bloomberg noted that since 2000, 53% of the analysts have predicted a gain of 0 to 10%.

In reality, the analysts have missed the mark by more than 15 percentage points since 2000. So take these predictions as “entertainment” like sports-watching.

Weak economic data (see below) from China and officials’ signalling may mean more monetary and fiscal easing is forthcoming (e.g. a cut in reserve ratio requirement may be announced in the coming weeks and more support for consumption may come before the Chinese Lunar New Year (end of January)).

In the coming 2 weeks, we will monitor the US November ISM Manufacturing Index on Jan 3, the UK and Euro area Manufacturing PMI on Jan 2, Japan’s December Tokyo inflation and November industrial production on December 26, and China’s December NBS Manufacturing PMI on Jan 31, and Caixin Manufacturing PMI on Jan 2.

Economy and Investments (Links):

In developing new projections, "some people did take a very preliminary step and start to incorporate highly conditional estimates of economic effects of policies into their forecasts at this meeting," Powell said of an outlook in which U.S. central bankers anticipated a higher inflation outlook and fewer rate cuts next year.

An index of policymakers' sense of risk around their projections also shifted sharply higher for inflation, with a separate measure of uncertainty increasing as well in an abrupt change from the outlook issued in September, before the Nov. 5 U.S. presidential election.

The events demonstrated that while Musk has the power to destroy carefully negotiated plans, it remains unclear if he can push Republican lawmakers toward passing new measures.

3. The Book of Genesis: Wall Street Edition (The Big Picture)

The Eternal Market:

The Trader declared, “As long as the bells ring on the Exchange, there will be Bulls and Bears, Boom and Bust, Greed and Fear. But those who trust in Fundamentals and manage their Risk shall inherit lasting wealth.”

And thus, the Market continued to evolve, guided by the invisible hand of the Trader, forever balancing the forces of creation and correction.

Finance/Wealth (Link):

One of the Most Infamous Trades on Wall Street Is Roaring Back (Bloomberg or via Archive)

[One of the most-read stories in 2024 at Bloomberg]

Known as short-volatility bets, they were a key factor in the stock plunge of early 2018 when they wiped out in epic fashion. Now they’re back in a different guise — and at a much, much bigger scale.

Their new form largely takes the shape of ETFs that sell options on stocks or indexes in order to juice returns. Assets in such products have almost quadrupled in two years to a record $64 billion, data compiled by Global X ETFs show. Their 2018 short-vol counterparts — a small group of funds making direct bets on expected volatility — had only about $2.1 billion before they imploded.

Wellness/Idea (Link):

The FDA Just Redefined “Healthy”—But How? (10almonds)

To bear the “healthy” claim, a food product needs to:

Contain a certain amount of food (food group equivalent) from at least one of the food groups or subgroups (such as fruits, vegetables, fat-free and low-fat dairy etc.) recommended by the Dietary Guidelines.

Adhere to specified limits for the following nutrients: saturated fat, sodium, and added sugars.

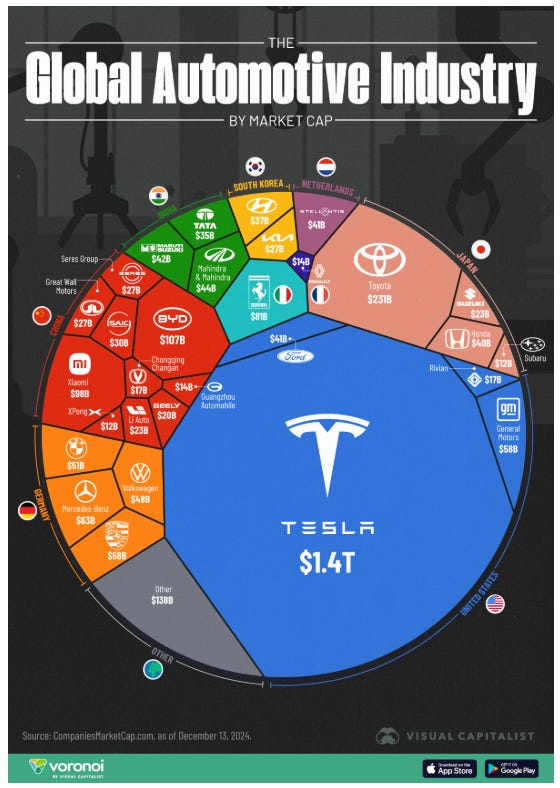

One Chart You Should Not Miss: Global Automotive Industry by Market Cap

Tesla’s prowess reflects not only Elon Musk’s rising power in the Trump government but also Tesla’s Robotaxi and full self-driving technology and future tax cuts that benefit US manufacturers including Tesla. Despite Tesla’s market cap being 48% of the global automotive industry market cap, its production (1.8 million in 2023) trailed by a mile Toyota's No. 2 market cap at 11.2 million.

One Term to Know: US Debt Ceiling

The debt limit is a cap on US government borrowing that affects only its ability to pay existing bills (such as Federal workers’ wages, social security, Treasury bond interests, etc.) and not to approve more spending.

There are extraordinary measures the Treasury Secretary can take to keep paying the debt obligations for a limited time (when the debt limit is approaching) such as delaying contributions to the Federal Employee retirement funds.

The debt limit was created in 1917 as a general borrowing limit (as opposed to a limit on specific bond issues) to allow the Treasury Secretary to figure out the best mix of securities to issue without as much congressional oversight as before. By 1939, on the eve of WWII, Congress eliminated all specific limits on all types of bonds and established an aggregate debt limit.

The debt limit had always been raised without controversy until in 1953 the Senate sidetracked the House's request to raise the debt limit “where the ceiling was viewed as an instrument for forcing economy on the executive branch of the government.”

The debt ceiling became the centre of a political vote and caused government shutdowns (in 1995/1996), consumer confidence to plummet, and credit agency S&P to downgrade US debt rating (in 2011).

Recently, President-elect Trump wanted to eliminate the debt ceiling as this would raise a political fight when he needed to extend the personal tax cuts he enacted in 2017 which would expire at the end of 2025.

[🌻] Things I Learn About AI/Productivity:

I Called 1-800-ChatGPT, and Talked to the AI Chatbot. It Might Be the Smartest Idea I’ve Seen Yet (Inc.)

Paul Couvert’s discussion on the latest Gemini Advanced version that can do “Deep Research” is fascinating. This refers to an AI powerhouse capable of planning, reasoning, and searching the internet – all within a single prompt.

This is a game-changer: it's the first reasoning model with internet access, and it's going to transform how we gather and synthesize information.

Why is this a game-changer? He explained:

Efficiency: Automate complex research tasks, saving you hours of manual effort.

Comprehensiveness: Get a holistic view of a topic with insights from multiple sources.

Structure: Receive well-organized reports that are easy to understand and navigate.

Accessibility: Access the power of AI-driven research within the familiar Gemini interface.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

The short volatility trade is very interesting. Another well curated issue of what truly matters. Thank you for your hard work and consistency in keeping your readers informed.

Thanks so much @marketlab for restacking and much appreciate your support! Have a wonderful holiday season!!