Weekly Good Reads: 5-1-1

Year of Monetary Easing, Average Stock vs Overall Index, Tail Risks, Adult Skills, Wellness Trends, AI and You

Welcome to a new Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

Sharing the quote of the week:

The universe is not outside of you. Look inside yourself; everything that you want, you already are. ~ Rumi

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

Here’s my latest investing post in case you have missed it:

👉 One more: I am inviting you to try our firm’s digital investment software for creating customized portfolios tailored just for your goals and risk profile (for free):

Market and Data Comments

The S&P 500 retreated by 0.6% while the Nasdaq continued to climb, rising 0.3% in the past week and briefly touching above 20,000 on Wednesday. The communications sector led the pack this week by jumping 2.4% and outperformed the rest of the sectors at 43.1% YTD.

According to S&P Global (see charts below) based on the Investment Manager Index Survey, “Risk appetite [is] highest since April 2021 as investors see US equities gaining value through 2025…Bullishness is led by financials and tech, while defensives, energy, and real estate suffer from investor disfavour. “

The below Macrobond chart shows how the market-cap-weighted sector performances differ (quite dramatically) from an equally weighted one. For example, the communications service sector shows a 45.8% (YTD to 12/11/24) versus the equally weighted at 24.6% YTD (almost halved). Financials, utilities, and industries on an equally weighted basis would have outperformed communications services, reflecting how a few mega-cap stocks in communications services, information technology, and consumer discretionary, largely fuelled by AI, have dominated the sector gain.

With the most crowded trades being the “Magnificent Seven”, Bank of America said they liked the average stock, which was rather inexpensive, but not the overall index, and would overweight financials, materials, utilities, and real estate in 2025.

While Apollo hailed the economic resilience of the US economy (see Econ/Invest. #3), an FT roundtable of fund managers pointed out tail risks such as the US fiscal sustainability. The US 10-year government bond yield bears watching, as it has already climbed over 50bp YTD to 4.4% currently. Note in the October 2024 Fiscal Monitor, the IMF projects global public debt will exceed $100 trillion by the end of 2024, with the global debt-to-GDP ratio expected to approach 100% by 2030.

On notable economic data, the November US core CPI jumped 0.3% m/m, led by a tick-up in core goods inflation while the November PPI rose higher than expected by 0.4% m/m. The graph at the top shows the 3-month annualized core CPI (now at 3.66%) has been rising since the trough in July 2024 and the disinflation in core prices has stalled (3.3% y/y).

But looking at CPI and PPI together, Bloomberg estimates the November core PCE deflation—the Fed’s preferred inflation gauge will increase at 0.13% m/m (0.27% prior), and with the weekly initial claims further rising, the Fed is expected to cut another 25bp in the December FOMC next week.

By the end of next week, 22 of the world’s central banks will have announced their monetary policy decisions (see Econ/Invest. #1), finishing off a year of (mainly) easing with other major central banks such as the UK and Japan to stay put, but China and the US to ease.

This past week, the ECB lowered the interest rate by 25bp with 2 more 25bp cuts expected in H1 2025 to bring the deposit rate to 2% by June. Canada and Switzerland both cut by 50bp justified by economic data.

This coming week, we will monitor the US November retail sales on Tuesday, the FOMC meeting and the Fed’s Press conference on Wednesday, and the November personal spending and core PCE on Friday, monetary policy decisions by the Bank of England and the Bank of Japan on Friday, and China’s November retail sales, industrial production, and YTD to November fixed asset investment on Monday.

Economy and Investments (Links):

The 24 Hours of Rate Cuts That End Year of Global Central-Bank Easing (Bloomberg or via Archive)

China Expanding Private Pension Scheme to Raise Pension Awareness: Industry Insider (Bastille Post)

on X called out this “institutionalization (and individualization) of the pensions of one of the largest economies with the most old people and the highest savings rate is the most important investment story that no one is talking about...”

+ What Do Investors Need to Look Out For in 2025? (FT or via Archive)

++ For professional and interested investors, here’s a link to the Outlooks for 2025 by Wall Street/investment firms I have saved for your enjoyment.

Finance/Wealth (Link):

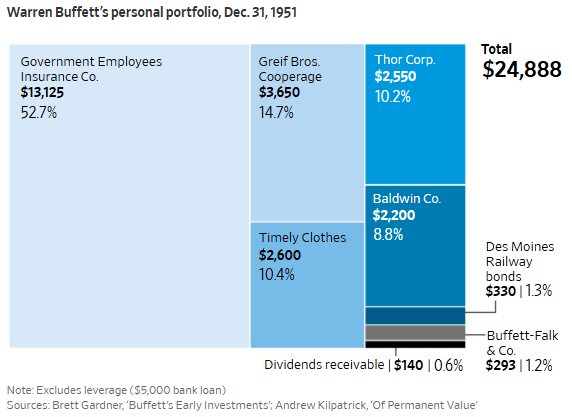

What You Can Learn from Young Warren Buffett (WSJ)

But Wall Street is more obsessed than ever with mindlessly chasing whatever’s most popular. As young Buffett’s track record shows, you can make good money by noticing where all the fishing boats are—and taking your rod and reel elsewhere.

+ Prof. Damodaran Reveals His Magnificent Seven Investment Approach (The Meb Faber Show)

You can't miss one of the sharpest minds in valuation and finance, especially when he discusses valuation in a hot sector.

Wellness/Idea (Link):

2025 Wellness Trends (well+good)

Nature time, solo time, financial wellness as a priority, unplugging vs. more gadgets, personalized beauty products, and travel for true restoration.

(N.B. I have no affiliation with well+good)

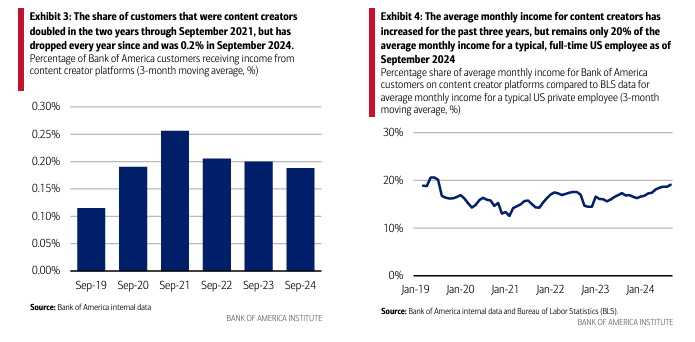

One Chart You Should Not Miss: Content Creator's Share of Average Monthly Income

Despite the rise of content creators (and their monthly income) in the past few years, data shows the average monthly income remains only 20% of that of a typical full-time employee (Bank of America).

One Term to Know: Adult Skills

The recently released OECD Survey of Adult Skills, which is published once every decade, directly assesses adults’ literacy, numeracy, and adaptive problem-solving skills, which are relevant in this age of rapid technological change and adoption.

A basic command of these skills is thought to be necessary for fully integrating and participating in the labour market, education and training, and social and civic life. Results from the first cycle of the survey show that adults with more advanced mastery of these skills also benefit from greater earnings, well-being, agency and prestige (OECD, 2013). Literacy, numeracy and adaptive problem-solving skills are domain-general and highly transferable, and relevant to many social contexts and work situations; they can also be learned and are therefore subject to the influence of policy. Understanding the level and distribution of these skills among adult populations in participating countries is thus important for policy makers in a range of social and economic policy areas.

Some notable conclusions: While Finland, Japan, the Netherlands, Norway and Sweden are the best-performing countries in all three domains, on average, across participating OECD countries, nearly 20% of adults are considered low performers.

On average across the OECD, about 23% of workers are over-qualified for their current job. In comparison, 9% are under-qualified—the U.K. (37%), Japan (35%) and Israel (34%) have the highest rates of over-qualification, while the Flemish Region (Belgium) (14%), Singapore (14%) and Poland (14%) have the lowest. About 26% of workers consider themselves to have higher skills than their job requires, while 10% report underskilling. There are relatively more workers reporting overskilling than underskilling in Estonia, Finland, Japan, and Norway.

There are significant economic and social costs associated with being overqualified for one's job: in particular, a 12% reduction in wages and a 4 percentage points reduction in the likelihood of reporting high life satisfaction. About one-third of workers across OECD countries are mismatched to their jobs, whether in terms of their qualifications, skills or fields of study.

[🌻] Things I Learn About AI/Productivity:

Series: What AI Knows About You (Axios)

Year in Search 2024 (Google Trends)

The Best AI Stocks: These 40 Companies Are Benefiting From the Boom (Capital.de, courtesy of The Big Picture)

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.