Weekly Good Reads: 5-1-1

Stocks Rally, What Now, FOMC, Rainwater and AI, Tariffs and Inflation

Welcome to a new issue of Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

In this Weekly, I share insightful/essential readings, charts, and one term, incorporating some of my market observations and weekly change tables. I look beyond data and share something enlightening about life, health, technology, and the world around us 🌍!

Sharing the quote of the week:

If you remember me, then I don't care if everybody else forgets.

— Haruki Murakami, “Kafka on the Shore” (via

)

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

Market and Data Comments

We got Trump 2.0 and likely a “red sweep” (Republicans have won the Senate and will likely win the House).

The Fed cut the target range of the Fed Funds rate by 25bp to a band of 4.5% to 4.75% but revealed nothing on the rate path going forward. The Fed is in no hurry to get back to the neutral rate, the level at which the economy is operating in equilibrium (albeit Powell signalled more cuts to come). Powell also mentioned there is no need for the labour market to slow down more to get inflation back to 2%.

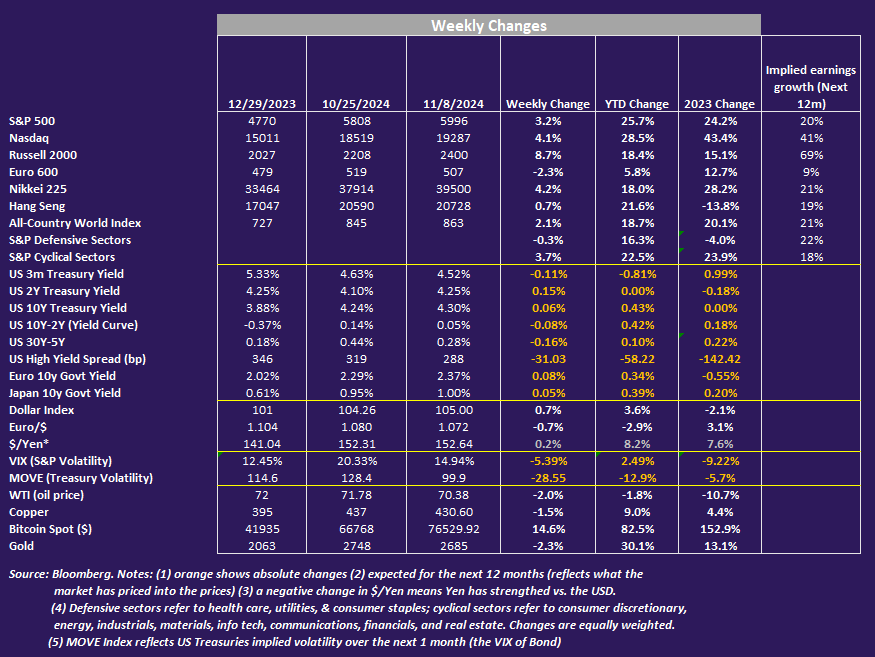

The S&P surged 4.66% in the past week, rising the most since the week ending on 11/3/23 (when the Fed became dovish). US cyclicals including consumer discretionary, financials and communications rallied above 5% while utilities suffered. US 10Y bond yield rose 15bp, but high yield bond spread tightened by 31bp and the dollar jumped 0.7% while both stock and bond volatility collapsed.

Bitcoin outperformed everything else surging almost 15% while gold and oil both dropped around 2% this week.

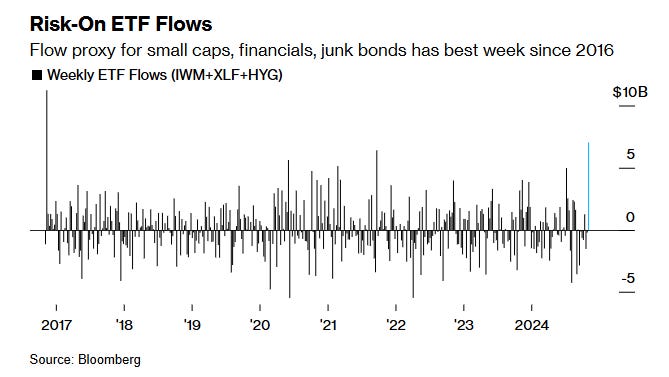

Bloomberg tracked risk-on ETFs flows (small caps, financials, junk bonds), and the past week was the best since 2016 (see top chart).

Euro 600 (main equity index) fell 2.3% while Japan Nikkei and the China A Shares both jumped over 4%.

The timing and extent of the implementation of the four main policies under Trump 2.0 (see Econ/Invest #1)—tax cuts, deregulation (financials, energy, bitcoin), immigration deportation, and tariffs (a maximum of 60% on China and 20% on the rest of the world)—will determine the final impact on US growth (slowing) and inflation (rising). Trump will also continue Biden’s active industrial policies.

The market rallied despite the likely negative impact on growth and inflation as it assumes a transactional approach by Trump with policy implementation taking time. One key indicator to watch is the US 10-year Treasury bond yield, which signals how the economy will be impacted by Trump’s policies.

I should preface no one knows the size, timing, and path of implementation and the net impact on the economy. We do know the economy is starting from a relatively strong place. Here are some extreme scenarios:

With Trump’s tax cut plans costing $11 trillion and no plan to plug the fiscal gap, the debt to GDP could rise to 150% at the worst (Bloomberg). The US 10Y treasury has already been pushed to 4.3% from a low of 3.62% in September - higher term premium and an expected slower pace of Fed rate cut (now -80bp implied in the next 12 months due to higher inflation rate in 2025/2026) would mean Trump’s tax plans will be difficult to implement fully.

If all of Trump’s tariffs are implemented (the market is assuming unlikely), average tariffs on goods will be 26% from 2.6% currently (Bloomberg), dampening growth and raising inflation (see more about tariffs in “One Term to Know”.)

Internationally, Trump’s tariff policies will likely slow investment and growth further in Europe, leading to around 0.7% growth in 2025, even weaker than the projected 0.8% growth in 2024 while fiscal loosening in the UK helps buffer trade uncertainty thus the growth forecast is maintained at around 1.2% in 2025 (Barclays). ECB is likely to ease policy continuously by 25bp in each meeting until the end of 2025.

China’s export outlook has weakened with the Trump tariff, but the authorities have so far announced a CNY 10 trillion for debt relief for the local governments and no announcement about supporting consumption or more Treasury bond issuance. However, the government is keeping its powder dry; with deflationary forces remaining strong (October CPI at 0.3% y/y while PPI at -2.9% y/y), the government will have more room to ease next year.

In the coming week, we will monitor the US October CPI on Wednesday, PPI on Thursday, retail sales and industrial production on Friday, the October German inflation on Tuesday, the Euro area Q3 GDP on Thursday, Japan’s Q3 GDP on Thursday, and China’s October retail sales, industrial production, and YTD fixed asset investment on Friday as well as its October total social financing announcement during the week.

Economy and Investments (Links):

Your Guide to Trump’s Day One Agenda (Bloomberg)

As global policymakers shape their strategies for the years ahead, they may wish to weight even more heavily the pain — and political upheaval — that result if they can't achieve stable prices.

- In particular, the incoming Trump administration may want to tread carefully in implementing elements of his agenda — particularly tariffs and mass deportations — that economists believe would fuel higher prices.

WEEKLY, NOV 9 - So it begins (@Noelle Acheson, Crypto is Macro Now)

This is a great summary as Bitcoin and cryptocurrencies are getting their moments under likely favourable Trump policy.

Around the world, investors are going to focusing on 1) hedging currency debasement and 2) the Trump market play. Both point to BTC.

Gold is the traditional currency debasement hedge, and is much easier for mainstream retail and institutional investors to understand. But it has arguably already had a strong run, and BTC has underperformed due to (now removed) regulatory uncertainty.

Looking at the ratio of BTC to gold, we can see the downward trend (gold outperforming) since March is turning.

Finance/Wealth (Link):

What to Buy If the Election Has You Worrying About Inflation (WSJ)

I think many investors may have gotten confused about the differences between owning TIPS directly and owning them in the form of a mutual fund or ETF. The differences are subtle but real. A TIPS fund spares you the travail of buying the securities one at a time, offering diversification in one convenient package, often at very low cost…You could avoid paying any annual expenses (other than some trading costs) by buying TIPS yourself.

If you buy TIPS directly and hold them to maturity, your future rate of return after inflation is certain, as is the return of your principal. Most TIPS funds, on the other hand, don’t have a maturity date, so you can’t know their future rate of return with the same certainty.

+ Dear Mr. President-Elect: Here’s How to Keep the Economy Strong (Barron’s)

Wellness/Idea (Link):

Ten Ways to Make Your Time Matter (Greater Good Magazine)

+ The Podcast Election (Scott Galloway)

One Chart You Should Not Miss: 10-Year Expected Returns (Nominal)

Morgan Stanley recently put out its 10Y nominal expected returns across global asset classes. Except for US Stocks and US High Yield Bonds, all other asset classes look cheaper compared to the past 20Y average return.

One Term to Know: Tariffs and Inflation

Countries use tariffs to raise the price of imported goods relative to domestic products. Tariffs are essentially taxes or duties on imports, which are ultimately passed on to consumers although firms may initially absorb part of the costs.

Tariffs are protectionist measures aiming to benefit domestic producers and generate revenue for the government.

They are inflationary primarily because they directly increase the prices of imported goods by imposing taxes on them. Product inflation results when these taxes are directly passed on to consumers. Also, many domestic manufacturers rely on imported components or raw materials, and the higher production costs contribute to price increases for finished goods.

Lower competition caused by tariffs also boosts inflationary pressures. By making foreign goods more costly, tariffs allow domestic producers to raise their prices without fear of losing market share. This can lower consumer’s purchasing power and lead to demands for higher wages.

Tariffs can disrupt established supply chains, creating inefficiencies that increase costs. They can also distort currency exchange rates and prompt central banks to adjust monetary policy in response to rising inflation.

Overall, the combination of direct price increases, reduced competition, increased market efficiencies, and other macroeconomic effects makes tariffs a significant driver of inflation.

[🌻] Things I Learn About AI/Productivity:

Rainwater Could Help Satisfy AI’s Water Demands (Scientific American)

Some industry leaders are beginning to see the potential. A Google data center in South Carolina is using rainwater retention ponds for harvesting rainwater. A Microsoft data center has implemented rainwater harvesting in Sweden, reducing reliance on local water sources. Amazon Web Services highlights the potential of rainwater harvesting in its water positive strategy.

This US Election Hub, which provides information about the US federal election based on user location and utilizing Associated Press data, has attracted attention and love (is Perplexity now a media company - something new the CEO may be focusing on…)

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

Much appreciate Enrique for restacking this post!!