Weekly Good Reads: 5-1-1

FOMC Minutes, China Stimulus, 100 Most Powerful Women, Money Hate, Innovation Diffusion, NotebookLM

Welcome to a new issue of Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

In this Weekly, I share insightful/essential readings, charts, and one term, incorporating some of my market observations and weekly change tables. I look beyond data and share something enlightening about life, health, technology, and the world around us 🌍!

Sharing the quote of the week:

Like snowflakes, the human pattern is never cast twice. We are uncommonly and marvelously intricate in thought and action, our problems are most complex and, too often, silently borne.

~ Alice Childress, American Novelist

Feedback is important to me, so if you like the Weekly, please “heart” it, comment, share it, or subscribe! Thank you so much for your support🙏.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

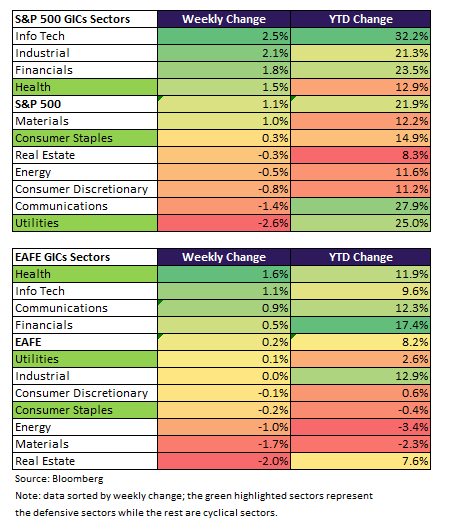

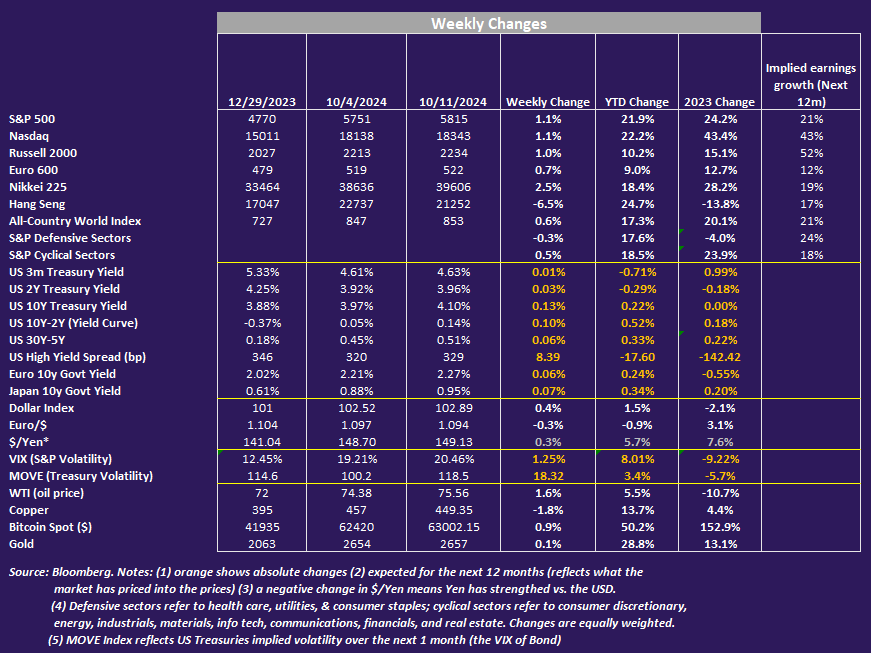

Market and Data Comments

US September CPI came in at 2.44% yoy (headline) and a higher-than-expected 3.31% yoy (core, 3.2% prior, with the 6m annualized declining to 2.6% (2.7% prior)). This came after a relatively strong September jobs report.

Bloomberg estimates September core PCE (considering both CPI and PPI announced) will likely be 2.6% yoy and 0.25% mom despite the slight uptick in CPI. The market is now barely discounting a 50bp rate cut by the end of the year (compared to the median Fed projection of 50bp of further rate decline), and the next Fed meeting on November 6-7 would be a close call (see Econ/Invest #1).

Rate cut uncertainty resulted in increased bond volatility this week (MOVE index up 18 points) while the major global stock markets (except Hong Kong and China) continued to climb with the S&P 500 reaching an all-time high.

As Q3 US earnings season has kicked off, investors expect the weakest profit growth (~4.3%) in four quarters albeit the S&P 493 stocks (i.e. excluding the Magnificent 7) will likely post profit growth again in Q3 (see chart below), supported by an economy that is not growing too fast or too slow (hear SF Fed Mary Daly’s discussion of the state of the economy in Econ/Invest #2) and monetary policy aligning with the reality of the economy (i.e. the need to reduce the too-high real interest rates).

Further proof of likely sector performance: Apollo pointed to the health care, financials, and consumer staples sectors doing the best in Fed rate-cutting cycles in non-recessionary periods.

US Q3 real GDP is looking solid in contrast to its Euro counterpart, which is likely in contraction (Germany expects its economic growth to contract by 0.2% this year); hence economists expect the ECB will have to cut interest rates by 25 bp back-to-back in future meetings.

Elsewhere, China’s Finance Minister was short on details on Saturday on the size of the fiscal stimulus and was weak on consumption support (key to reflating the economy). They did signal more funding solutions to help local governments resolve their debt problems and the issuance of more treasury and local bonds (expected RMB2 trillion). More sectors will be eligible to receive funding support from the issuance of sovereign bonds, a significant move to inject liquidity into the rest of the economy. More details on the fiscal stimulus are expected in late October from the National People’s Congress.

This coming week we will monitor the US September retail sales and industrial production on Thursday, the September housing starts on Friday, the ECB monetary policy meeting and press conference on Thursday, September U.K. inflation on Wednesday, Japan’s September CPI on Friday, and China’s September PPI and CPI on Sunday, September exports on Tuesday, Q3 GDP, September industrial production, retail sales, and YTD fixed asset investment on Friday.

Economy and Investments (Links):

Powell’s Half-Point Cut Is Hard to Repeat With FOMC in No Hurry (Bloomberg or via Archive)

Monetary Policy and Economic Outlook (President, Federal Reserve Bank of San Francisco, Live Recording) - I highly recommend hearing this clear explanation of the FOMC action and the state of the economy and workers. One problem she emphasized (without good solutions) is housing and the plunge in affordability (below 13% for first-time home buyers) as demand far exceeds supply.

Trump and Harris basically agree on: stronger borders and tougher immigration laws; a tougher stance against China; increasing domestic energy production including fracking; providing incentives for US manufacturing; supporting Israel and its wars; providing more child-care asistance to parents; protecting IVF treatment; opposing a national abortion ban; ignoring the deficit; proteting social securty and medicare; and no tax on tips.

The explanation: Trump's base is now the working class, and he's making inroads with union members and non-white voters. He's more open than ever to spending lots of government money on big government programs.

Harris' base includes more rich white people than ever, and she's making a concerted play for Never-Trump Republicans to win key swing states. So she's moderated her most liberal positions.

Hence, the surprising agreement.

Related: FAQ on the US Election (Capital Economics)

Finance/Wealth (Link):

How Can I Stop Hating Everything About Money? (Sherwood)

But if we create a process to approach money safely, we can decondition the intensity of the aversive response and give your brain and body the opportunity to repattern around feelings of competence, purpose, and self-trust…

A simple goal might be to make an updated list of your [investment] accounts and their current balances while staying present with your emotions throughout…

Establishing a time boundary reduces avoidance by telling our brain and body that the unpleasant task that we’re going to undertake is not going to last forever. When working on ingrained avoidant patterns, I recommend starting with regular, brief exposure sessions where there is a focused and concrete task. The goal is to practice opening the money box, doing the task, closing it, and putting it away…

Wellness/Idea (Link):

Americans are Chuffed as Chips at British English (The Economist or via Archive)

+ Gen Z, Millennial, Zillennial? Find Your Generation — and What It Means — By Year (USA Today)

According to a report in June by the Transamerica Center for Retirement Studies, nearly half of all workers across four generations from baby boomers to Gen Z either plan to retire past age 65 or not retire at all.

In 2023, Gen Alpha was the most racially and ethnically diverse generation, with whites making up less than half of the population of people born in the Gen Alpha birth years (2013 to present) {Annie E. Casey Foundation].

One Chart You Should Not Miss: 100 Most Powerful Women (Fortune)

We are not going to wait to be disrupted.

~ General Motors CEO, Mary Barra

The top three sectors for women leaders are financials (26%), information technology (17%), and consumer discretionary (15%) while the biggest country concentration is in the U.S. (54%), U.K. (8%), and Spain (2%).

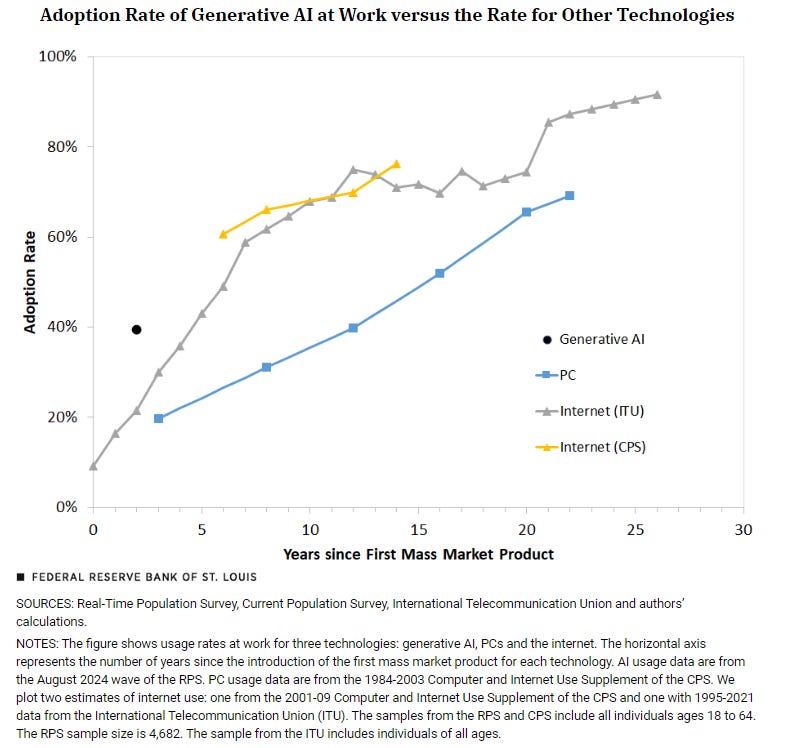

One Term to Know: Diffusion of Innovations

Everett Rogers famously modelled how people react, adopt, and accept new ideas and technologies and named 5 types of adopters: innovators (2.5% of the total), early adopters (13.5%), early majority (34%), late majority (34%), and laggards (16%)—the diffusion of technology model where innovations are communicated through multiple channels over time amongst the different participants in a social system. For the innovation to self-sustain, it must be widely adopted. The point at which a critical mass of adoption appears is at the boundary between the early adopters and the early majority.

A recent St. Louis Fed research compared the adoption rate of Gen AI at work versus those for other technologies and found generative AI use is widespread across gender, age, education, industries and occupations.

Generative AI [at 39.4%] has been adopted at a faster pace than PCs or the internet. Adoption of the PC three years after its mass introduction was only at 20%, about the same value as for adoption of the internet after two years.

The researcher estimated generative AI could probably raise labour productivity by between 0.1% and 0.9% at the current levels of usage.

[🌻] Things I Learn About AI/Productivity:

The Week that Artificial Intelligence Swept the Nobel Prizes (FT and via Archive)

Have you tried NotebookLM by Google, which allows you to upload a document or use a URL and turn it into a note, brief, summary, table of contents, timeline, or podcast (with male-female voices for a deep dive)? It is a fun, handy, and efficient productivity tool with caveats. Listen to the AI audio summary of India Deep Dive by

.

Having used it myself to interpret the why, what, and how of a service we provide at my firm, I would say the material only goes 60% of the way there in terms of information density. In my case, the podcast story Gen AI created took off on its own with irrelevant commentaries, fillers, and questioning without understanding the underlying topic. So humans are necessary in the loop to make this a helpful assistant.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.