Weekly Good Reads: 5-1-1

FOMC, Asset Performances After Rate Cut, Money and Happiness, Monetary Policy Transmission, Note-Taking

Welcome to Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

In this Weekly, I share insightful/essential readings, charts, and one term, incorporating some of my market observations and weekly change tables. I look beyond data and share something enlightening about life, health, technology, and the world around us 🌍!

Here’s the quote of the week:

Motivation is much less about external prodding or stimulation, and much more about what’s inside of you, and inside of your work.

~Clayton M. Christensen, How Will You Measure Your Life?

Feedback is important to me, so if you like the Weekly, please “heart” it, comment, share it, or subscribe! Thank you so much for your support🙏.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

Market and Data Comments

The Fed delivered a most anticipated rate cut on Wednesday (Sept 18) and kicked off with a jumbo 50bp cut. While some may be surprised by the 50bp, Fed chairman Powell called this a "re-calibration" to bring monetary policy to more neutral, as the risks to inflation and employment are now seen as balanced. Powell mentioned the weak August Beige Book (due to weakening manufacturing activity) and the downward revision of non-farm payrolls (-818k in the past year) prompted this rate cut.

Barclays found that when the unemployment rate rose by 50bp over the past 6 months (as in the US), developed countries’ central banks cut rates by an average of 50bp.

The September Summary of Economic Projections (SEP) median plots imply a further 50bp cut of interest rate for the rest of 2024 and another 1% in 2025 with the median long-run interest rate ending at 2.9% (see graph above). Except for the long-run interest rate, the year-end median Fed Funds rates in 2024, 2025, and 2026 were lower as compared to the June projections.

Year-end 2024-2026 median unemployment rates were all projected higher (vs. June projections) while median core inflation for 2024 and 2025 were projected lower (vs. June). Importantly, the Fed does not see a recession as real GDP for the end of 2024, 2025, and 2026 are all projected at 2% (median).

One important global driver of falling inflation is China, whose excess capacity (caused by weak consumption and investment) continues to export disinflationary pressure globally, especially to the developed market trading partners.

The US interest rate cut prompted other central banks (in emerging countries) to cut last week albeit the Bank of England and the Bank of Japan held their interest rates (largely expected). The above graph shows the prevalence of rate cuts around the world (except for Japan and Brazil).

Stock markets rose after the US rate cut this past week, led by the cyclical sectors, while the US 10-year government bond yield rose 10bp (+9bp last week) and the 2y-10y yield curve positively steepened to 15bp, i.e. 10y yield is now 15bp above 2y yield. The Dollar Index dropped 0.4% this past week while all major commodities (especially oil) rallied. Long-term fixed mortgage rates in the US inched towards 6%.

Naturally, the dominant investor’s question is what’s next to asset price performances and how to position their investments after the first US rate cut. Bloomberg using data since 1989 found the S&P 500, Treasuries, and gold have typically risen in the next year as the Fed starts lowering rates. Whether the S&P jumps post-cut depends on whether or not the US can avoid a recession (see One Chart You Should Not Miss below).

An interesting paper touted the superiority (in terms of risk-adjusted returns and the drawdowns) of a global market portfolio which consists of a mix of global equities (public + private), global bonds, broad commodities, and real estate versus its constituent asset classes, a case for extreme diversification.

The market also focuses on the recent dis-inversion of the 2y-10y US yield curve, i.e. 10Y minus 2Y yield has turned positive (or upward-sloping). Goldman Sachs found the US equity markets returned positively following yield curve dis-inversion if the US avoided a recession; at the same time, 10y government yield could continue to rise if there was no recession (so be careful if you consider moving into long-dated bonds).

This coming week, we will monitor the US August new home sales on Wednesday, August personal spending and core PCE price index on Friday, the September preliminary Composite PMI for the Euro area and the UK on Monday, China’s September 1-year medium-term lending facility rate on Wednesday and various central banks interest rate announcements by Australia, Brazil, Hungary, Mexico, Sweden and Switzerland throughout the week.

Economy and Investments (Links):

What the Fed Rate Cut Means (With Claudia Sahm) (Charles Schwab podcast)

And right now, the most troubling statistic in the U.S. labor market is the hiring rate. It has fallen back to levels that are close to 2014 when the unemployment rate was 6%…And yet we have layoff rates at almost all-time lows. And we have consumer spending—looks great, and this looks … that hiring rate being as low as it is, is going to continue to cause problems. We're going to keep seeing unemployment rate move up. We're going to keep seeing the payrolls slow down—not maybe dramatically, because we haven't big layoffs—but it's a real problem. ~ Claudia Sahm

Fed up with Fed Talk? Factchecking Central Banking Fairy Tales! -"The Fed (did not) do it" (

)

The Fed (and every other central bank) in my view is like Chanticleer, with investors endowing it with powers to set interest rates and drive stock prices, since the Fed's actions and market movements seem synchronized. As with Chanticleer, the truth is that the Fed is acting in response to changes in markets rather than driving those actions, and it is thus more follower than leader. That said, there is the very real possibility that the Fed may start to believe its own hype, and that hubristic central bankers may decide that they set rates and drive stock markets, rather than the other way around. That would be disastrous, since the power of the Fed comes from the perception that it has power, and an over reach can lay bare the truth.

No one could’ve predicted the rise of the Magnificent Seven and the subsequent dominance of US stocks back in 2010. On the contrary, back then, there was little reason to favor the American market.

The MSCI EAFE index’s track record stretches back to 1970, and during the next four decades, it returned an average 10.2% annually – slightly outperforming the S&P 500’s 9.9% yearly average. Over rolling ten-year periods, the EAFE Index outperformed 56% of the time.

The underlying fundamentals were also closely aligned. The MSCI EAFE and the S&P 500 both saw average earnings growth of 5.7% per year, from 1973 to 2009, according to the earliest data available for the EAFE index. Valuations for that index expanded by 0.9% annually over the period, compared to 0.5% for the S&P 500. And, remember, dividend yields in developed international stocks are generally higher than in the US – but not by a lot.

Finance/Wealth (Link):

Where to Put Your Money After the Fed Rate Cut (WSJ or via Archive)

Banks tend to change CD yields more quickly when rates are falling than when rates are rising, research has found. In periods when rates were decreasing between 1997 and 2011, banks left yields unchanged on 3-month CDs for a median of three weeks. When rates were increasing, they left yields unchanged for a median of six weeks, according to a 2022 paper published by the Fed.

+ Related: What Federal Reserve Rate Cuts Mean for Your Money (Bloomberg)

One financial advisor advised if you are behind in bills in this lower interest rate environment:

The best thing Americans can do to catch up on their bills now that interest rates are heading down is reduce their discretionary or non-essential spending and if possible, start saving. In fact, people who are behind on their bills should do this regardless of whether interest rates are going up or coming down. The fact that interest rates are heading down is not some kind of magic bullet. The best way to deal with your debt is by paying it, especially for those who are behind on credit-card bills. Being behind on credit-card bills most likely means that people are paying double-digit rates. If your rate is over 20%, what does a half a percentage point or quarter-percentage point decline in interest rates do to you? Nothing, really. Your best bet is to keep paying down the debt.

Wellness/Idea (Link):

A New Way to View Money and Happiness (Greater Good Science)

Smaller communities, bigger happiness - Previous studies have tended to focus on people in wealthier, Western, urbanized countries. This one looked at those living in small-scale, rural communities that depend on nature for livelihoods, with no or little cash income. Some are Indigenous; most are located in Africa, South America, and Asia. Their results yield new insights into the relationship between money and happiness.

+ Online/Offline (Scott Galloway)

If the cycle time of innovation keeps contracting, we may register even greater changes in the next 15 years. The net-net of a jump to lightspeed in innovation is a mix of unprecedented prosperity and danger, as godlike technology will collide with paleolithic instincts and medieval institutions.

One Chart You Should Not Miss: S&P 500 Returns (Index and Sector Returns) After Start of Interest Rate Cuts (Source: Morgan Stanley)

As the Fed has just started an easing cycle, investors are interested in understanding the relative performance of industry groups and equity factors around the Fed's first rate cut of the cycle (historically).

The first chart shows these performance dynamics in an equal-weighted context.

Value tends to outperform going into the interest rate cut and underperform growth post-cut. Defensive sectors tend to outperform cyclical sectors pre and post-cut, as do large caps outperforming small caps. This led Morgan Stanley to favour the defensive sectors and large-cap stocks as Fed cuts often come in a later-cycle environment.

At the index level, while the S&P 500 was generally up after the first rate cut, the performances were extremely mixed. When the cuts happened as a response to a deepening recession as in 1973-4, 1981, 2001, and 2007, stocks did badly. For the moment, the US appears to be in a soft-landing scenario.

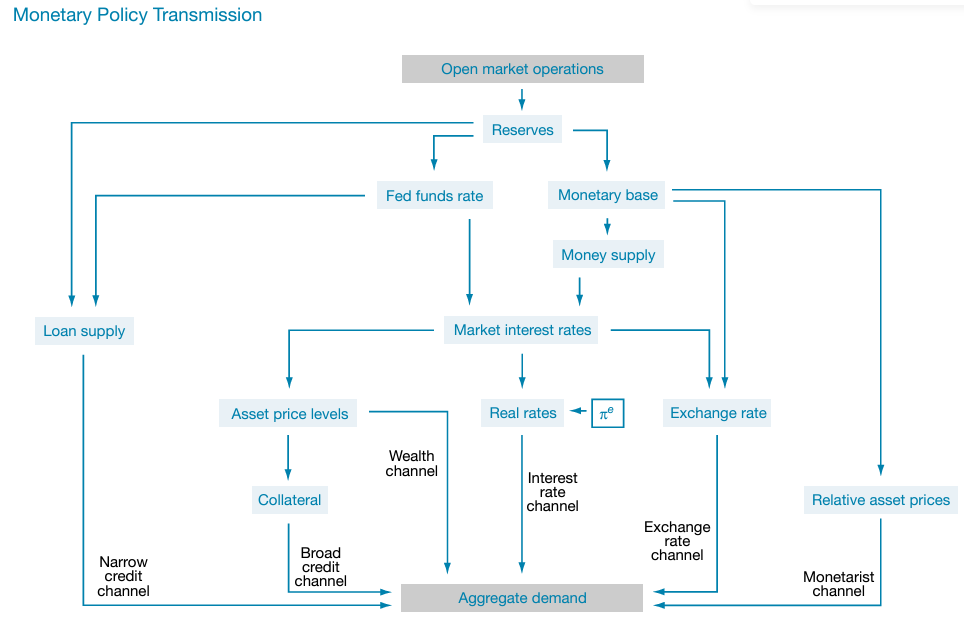

One Term to Know: Monetary Policy Transmission Mechanism and its Impact on the Real Economy

To implement monetary policy changes, the Fed can change the federal funds rate and/or change the amount of government securities holdings on its balance sheet.

The Fed Funds is the rate at which banks lend reserves to each other overnight. The change in the Fed funds rate affects the supply of bank reserves via the Fed’s open market operations through the Fed’s buying and selling of government securities. The Fed also guides the Fed funds rate by changing the interest on excess reserves and overnight reverse repurchase agreements.

The Fed can only directly change the Fed Funds rate which influences the banks’ lending/saving rates and therefore the investment and saving decisions of consumers and businesses with widespread implications on economic activity. Longer-term bond yields, loans, and mortgage rates adjust (indirectly) as a result.

Monetary policy transmission works through multiple channels including savings and investments, consumer spending, exchange rate, relative asset prices, and inflation/economic expectations. The timing and interactions of these channels are not straightforward. In addition, monetary policy operates with a 1 to 2-year lag on the economy, while financial innovations such as securitization, shifts between sources of financing for residential investment, or changes in the strength of wealth effects could cause the monetary policy to have less of an impact on the real economy.

[🌻] Things I Learn About AI/Productivity:

I am contrasting two different ways of note-taking and summarization of information:

Upgraded Google NotebookLM as a Learning Tool (

)My friend

summarized the all-in-one NotebookLM functions well, and I have started recommending this tool to my friends, especially if they want to be productive using their own data.Tips for Effective Note-Taking by Hand (Archer and Olive)

This is still my preferred way of taking notes, and I have not seen a more elegant and comprehensive way to take notes! I especially love the idea of a space created upfront for the main takeaways and the QR code.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.