Weekly Good Reads: 5-1-1

US Inflation, Interest Rates Decisions, Power and Utilities, Housing Affordability, Trade Partners

Welcome to Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

In this Weekly, I share insightful/essential readings, charts, and one term, incorporating some of my market observations and weekly change tables. I look beyond data and share something enlightening about life, health, technology, and the world around us 🌍!

Here’s the quote of the week:

You may be in a tough time but that setback is simply a setup for a greater comeback.

~ Joel Osteen

Feedback is important to me, so if you like the Weekly, please “heart” it, comment, share it, or subscribe! Thank you so much for your support🙏.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

Market and Data Comments

The Fed Funds futures, as of September 13, 2024, predicted a coin toss (50-50) between a 25bp or 50bp rate cut by the Fed in the FOMC meeting on September 17-18, a rare happening which prompted Anna Wong, Bloomberg’s chief economist to suggest the Fed may signal its intention probably on Monday.

From a risk-management perspective, the economic cost of a pre-emptive jumbo cut is lower than the cost of waiting, then being forced into a big move later by further deterioration in the labor market. Powell and several other Fed officials have said it’s usually too late to cut by the time the evidence of labor-market deterioration is clear. If the labor market does stabilize later, the Fed can always skip a cut at a subsequent meeting. ~Anna Wong, Bloomberg

The Fed will update its September Summary of Economic Projections at the upcoming FOMC meeting, the last Fed meeting before the November US presidential election. A 50-bp interest cut will fit better with the faster-than-expected rise in the unemployment rate (now at 4.2%; the median June Fed Projection was 4.1% for the end of 2024) and the already restrictive impact on growth of the current 5.375% Fed Funds rate. Rather than the initial cut, the path of the Fed Funds rate is the most important question.

The August core CPI data accelerated to 0.3% m/m and 3.2% y/y with 3-month annualized at 2.1%, compared to 1.6% in July, due to the pickup in the shelter (+0.5% m/m) and airline costs while CPI grew 0.2% m/m and 2.5% y/y as expected.

The PCE price index, the Fed’s inflation gauge, does not put as much weight on shelter as CPI does. With the August PPI rising the least at 1.7% y/y since early 2024, core PCE (PCE draws on components of CPI and PPI) is expected to trend to 2.7% y/y in August (see chart below).

Market expectations of a 50bp rate cut sent global stocks up 3% and S&P500 and Nasdaq up 4% and 6% this past week respectively. Recent Nvidia’s CEO’s statement rekindled the AI and tech trades: “Demand is so great that delivery of our components, our technology, infrastructure, and software is really emotional for people.”

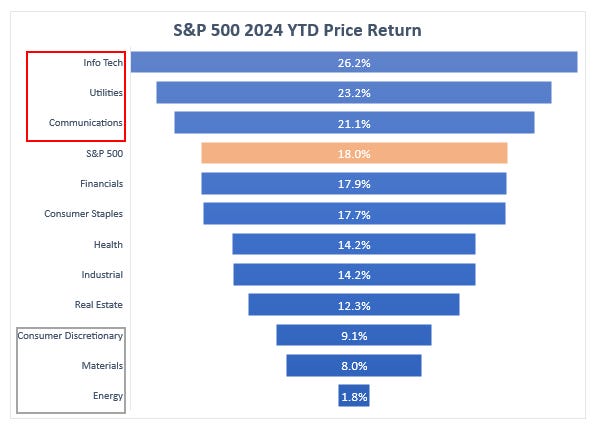

YTD, technology, and communications sectors are among the top three performers. Utilities/power occupies the second best, due to energy and power need for data centres related to AI, clean energy and infrastructure investments, and fair dividend yield (around 2.9%) vs. long bond yield (3.65%). Nuclear energy is also coming into the picture to solve the electricity problems.

In the recent Harris-Trump presidential debate, economic keywords were the most mentioned with housing shortage at the centre of the race. Still, there were few discussions about how the respective economic plans would be paid for, with severe implications for the public debt. The Wharton Budget Model projected that Harris's Campaign tax and spending proposals would increase primary deficits by up to $2 trillion while those of Trump would raise primary deficits by close to $6 trillion.

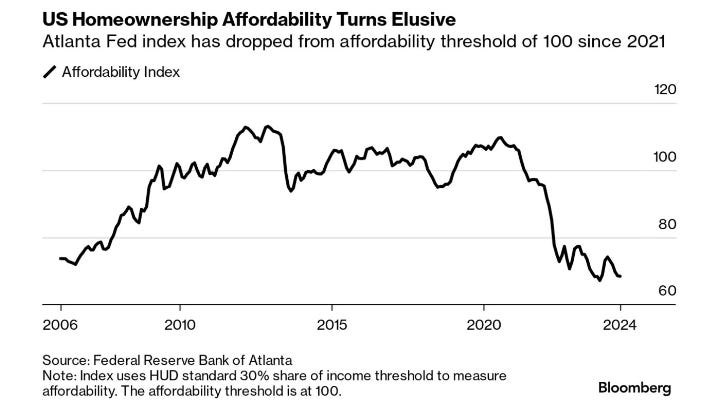

Homeownership affordability reached its lowest since October 2006 (see discussion in One Term to Know below) due to rising and high interest rates but more importantly, a severe supply shortage since the 2008-2009 housing crisis.

The ECB cut interest rates for the second time by 25bp this past week while revising downward its growth forecasts due to more subdue consumption and weaker-than-expected manufacturing in Germany (see Econ/Invest #2 on former ECB president Draghi’s plan to revive Europe).

The Bank of England, based on its cautious easing tone in the last meeting), is expected to hold interest this week before cutting again in November. Bank of Japan will stand pat on interest rates amid its LDP presidential election. Brazil is expected to hike due to increasing inflationary pressure and worsening inflation expectations.

Newly released data for China on retail sales, industrial production, fixed asset investment, and unemployment were all worse than expected, calling for the government to step up fiscal support and not just gradual monetary easing.

This week we will monitor the US August retail sales and industrial production on Tuesday, the FOMC decision, and Powell’s press conference on Wednesday, the Bank of England rate decision on Wednesday, Japan’s August CPI and Bank of Japan’s monetary policy decision on Thursday.

Economy and Investments (Links):

What Have Biden and Harris Accomplished? Look at These 10 Metrics (Bloomberg or via Archive)

Great Powers Index 2024: The Most Important Facts and Charts (Ray Dalio on LinkedIn and the full report)

Can Anything Spark Europe’s Economy Back to Life? (The Economist or via Archive)

The {Mario Draghi’s, former ECB President and Italian prime minister] report follows another, published in April, by Enrico Letta, another former Italian prime minister, which looked at the single market. Both focus on how to make Europe more competitive. The authors want to boost innovation, increase funding for riskier ventures (commercial, financial or scientific) and exploit Europe’s scale by bringing together hitherto fragmented markets. In short, they want to make Europe a bit more European, which in these areas at least is smart. The questions are as follows: Will countries be willing to see integration in sensitive sectors such as defence? Will they be able to overcome the narcissism of small differences? And will they be willing to spend as required?

Finance/Wealth (Link):

Learn to Read a Balance Sheet, Income Statement, and Cash Flow Statement, Visually (Brian Feroldi & Brian Stofffl)

Wellness/Idea (Link):

The Friendship Paradox (The Atlantic or via Archive)

Maintaining friendships in this atomized new world might require ratcheting down expectations. For parents with young kids, a weekly brunch with friends may well be impossible. Instead, Goldfarb suggests getting closer to your friends by taking an interest in things they care about, and asking to hang out for small, specific amounts of time. If you’re friends with a new parent, that is, don’t invite them to a bar 30 minutes away. Ask if you can bring over fresh fruit and chat for 20 minutes. “We need our friends to see us,” Goldfarb said. “We need our friends to take all our roles into account.

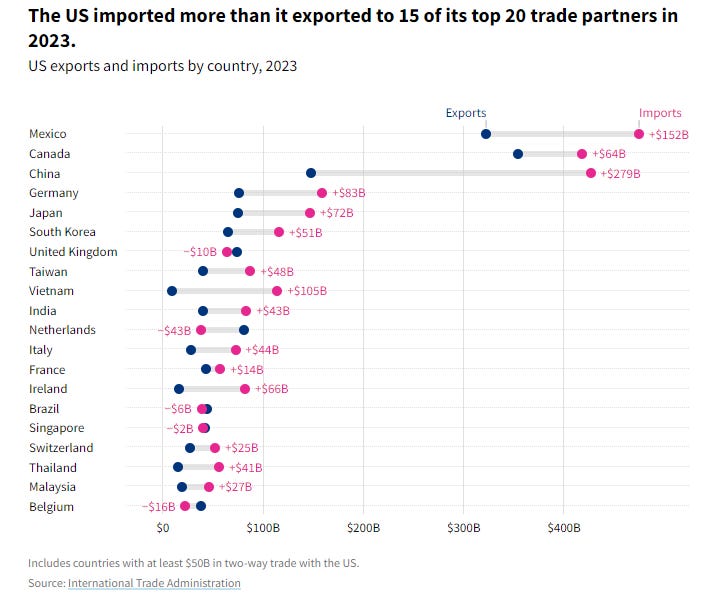

One Chart You Should Not Miss: Who Does the US Trade With?

In 2023, combining imports and exports, the United States’s top trade partner in 2023 was Mexico ($798 billion in goods and services), Canada ($773 billion), and China ($575 billion).

These 3 countries are also top US import and export partners.

The US ran the highest trade deficits with China ($279 billion), Mexico ($152 billion), and Vietnam ($105 billion). The US has been running a trade deficit of $1 trillion or more for 6 consecutive years.

One Term to Know: Housing Affordability

The affordable housing threshold is commonly defined as no more than 30 per cent of monthly household income to be spent on housing costs (rent and utilities). Spending above 30 per cent, the family will be considered cost-burdened.

The above chart shows the Bloomberg Housing Affordability Composite Index, sourced from the US National Association of Realtors.

When the index measures 100, a family earning the median income has exactly the amount needed to purchase a median-price resale home using conventional financing. An increase in the home affordability index means that a family is more likely to be able to afford the median-priced house.

Underbuilding and surging housing prices since the 2008-2009 financial crisis coupled with the recent high mortgage rates have created affordability and housing worst crises, pushing the local majors and presidential candidates to put housing policy right and centre.

In the swing states (battleground states) which include Arizona, Georgia, Michigan, Pennsylvania, Wisconsin, North Carolina and Nevada, the median monthly payment for homebuyers has grown by two times since 2020 to a record $2,161. No wonder housing costs is the most important issue for the voters in these swing states.

[🌻] Things I Learn About AI/Productivity:

The most important AI news is last week’s OpenAI’s announcement of its latest artificial intelligence model known internally as “Strawberry” or OpenAI o1, which can perform some human-like reasoning tasks that can solve multi-step problems including complicated maths and coding problems. See OpenAI Releases New Model With Reasoning Capabilities (Bloomberg or via Archive)

The experience of using OpenAI’s updated AI system will differ somewhat from what people have come to expect with ChatGPT, the company’s chatbot. Before responding to a user’s prompt, the new software will pause for a matter of seconds while, behind the scenes and invisible to the user, it considers a number of related prompts and then summarizes what appears to be the best response. This technique is sometimes referred to as “chain of thought” prompting.

Here’s a summary of what OpenAI research scientist Noam Brown said about model 01.

An interesting use case of AI is to generate cartoons to explain the more complex financial jargon or investing fallacies. Animation or satire can be used to simplify financial concepts or phenomena and engage the audience with good visuals and entertainment.

AI image generated by the author on Microsoft Co-Pilot — almost 80% of investors are put into a moderate risk bucket by their financial advisors (thus holding a 60% stocks/40% bonds type of portfolio). (Do clients need a financial advisor?)

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.