Weekly Good Reads: 5-1-1

Jackson Hole Summary, Global Easing, Bonds vs. Cash, Global Debt, Closed-end Funds vs. ETFs

Welcome to Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

In this Weekly, I share insightful/essential readings, charts, and one term, incorporating some of my market observations and weekly change tables. I look beyond data and share something enlightening about life, health, technology, and the world around us 🌍!

Here’s the quote of the week:

Awareness is the greatest agent for change.~ Eckhart Tolle

Here’s my latest economic and travel piece you might have missed:

Feedback is important to me, so if you like the Weekly, please “heart” it, comment, share it, or subscribe! Thank you so much for your support🙏.

Weeklies archive | Investing | Ideas | Index of charts and terms

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

Market and Data Comments

The most popular market news headline this past week is likely what Powell said at Jackson Hole on Friday: “The time has come for policy to adjust”. This is followed by: “The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks”, and “We do not seek or welcome further cooling in labour market conditions”. These indicate the Fed’s focus has shifted from inflation to the weakening labour market. See Powell’s full remarks (a great read of the unusual impact of the Pandemic on the economy and where the lingering concerns are).

Powell expressed more confidence in a rate cut in the next FOMC meeting on September 17-18 although he did not give a direction after the September meeting—all depending on incoming data (see Econ/Invest #1).

All told, the healing from pandemic distortions, our efforts to moderate aggregate demand, and the anchoring of expectations have worked together to put inflation on what increasingly appears to be a sustainable path to our 2 percent objective. ~ Fed Chairman Powell

One data supports a bigger slowdown in the labour market than initially thought: the Bureau of Labour Statistics said on Wednesday that 818,000 fewer jobs (-28% or -70k/month) were created in the year leading to March 2024 than originally reported. Given the rhetoric of Powell and the Fed governors, we should still expect a gradual easing pace from the FED starting at 25bp in September, unless the unemployment rate jumps say another 0.2 per cent in the next jobs report.

As the real interest rate (nominal interest rate minus inflation or inflation expectation) has been held up too high for too long (FRED estimates 1-month real interest rate at 3.9%), the labour market can weaken much more than analysts expect later this year and early next year, when the Fed has to quicken its pace of interest rate cuts.

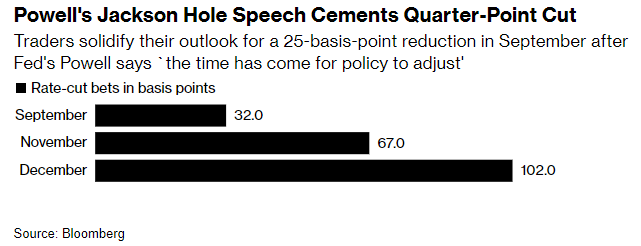

The market, as of August 23, has priced in a total of 102bp (1.02%) of interest rate reductions in the 3 remaining FOMC meetings this year in September, November, and December, implying there will be a 50bp cut later in the year.

The ECB and Bank of England were also open to further rate cuts as inflation concerns have lessened, while shorter-term growth risks are heightened, setting the path of a global “gradual” easing cycle despite the different extent of cuts in each country (except for Brazil and Japan—the latter has hiked rates and will face political leadership change which has implications for monetary policy.)

Global stock markets rallied 1.7% (MSCI All-Country World) and all US stock sectors rallied this week except Energy. US Treasuries and corporate bond papers are high in demand, with the US 10Y Government bond yield declining 8bp to 3.8%, the US 2Y-10Y yield curve steepening by 5bp, and the US dollar weakening by 1.7% this week. Here’s a great chart from UBS to show how US corporate bonds performed over the long term vs. US Treasuries, courtesy of

.

This coming week, the market will monitor the US July personal spending and core PCE, the Euro area July unemployment rate and the preliminary August inflation, all on Friday. Nvidia's earnings announcement on Wednesday will be closely watched if the momentum of AI capex spending by Big Tech is maintained.

Economy and Investments (Links):

Key Takeaways From the Fed’s Annual Jackson Hole Conference (Bloomberg or via Archive)

The Markets Safety Net May be Snagged, But It Held (FT or via Archive)

Generally speaking, without a recession, 10-year yields drop before rate-cutting cycles start, and then settle in to a range. If markets give up on the idea of a US recession (yes, again) then the 10-year yield could stretch back up to 4 per cent or higher, they wrote — a drop in price that would hurt and irritate in equal measure. “Bonds are not the free ride they used to be,” they said. That scepticism is reasonable. This safety net has holes in it. For now, though, the mere fact that it held is a big reason why stocks have been able to recover so swiftly from their summertime swoon.

Trump and Harris both read polls about inflation. To that end, Donald Trump’s general approach is to argue that cost is driven by government regulations, limits on oil drilling, and high corporate taxes, whereas Harris sees the issue in terms of big business having too much power to set prices. In other words, both articulate a frustration with centralized power, though Trump points only at government, while Harris points at both large corporations and government.

+ How Wonky US Payroll Revisions Became Controversial (BNN Bloomberg)

Finance/Wealth (Link):

Why There is Still Time to Move from Cash into Bonds (JP Morgan)

Looking at data back to the mid-1980s, extending duration one month before the first Fed rate cut instead of one month after has resulted in up to 5% greater returns over the subsequent year.1

It may be tempting to remain in cash and briefly pick up about an additional 50 bps of yield compared, say, to a strategy that tracks the Bloomberg U.S. Aggregate Bond Index, a broad bond market index with a 6.2-year duration position. However, there is a risk of missing out on potential greater returns following the first rate cut.

+ The Three Most Important Concepts in Investing (Darius Dale, 42 Macro)

Wellness/Idea (Link):

Who Prioritizes Work-Life Balance? (LinkedIn)

Two-thirds of U.S. employees say they are working to live as opposed to living for work, according to the latest findings of LinkedIn’s Workforce Confidence survey. Amid fears that more workers are burning out on the job, these findings suggest a majority of employees value their time spent outside of work and don’t necessarily consider work their top priority day-to-day.

Maintaining that work-life balance may be particularly important for younger workers; 72% of Gen Zers, 71% of millennials and 68% of Gen Xers agreed that they work to live. Baby boomers were least likely to agree — only 63% said they work to live.

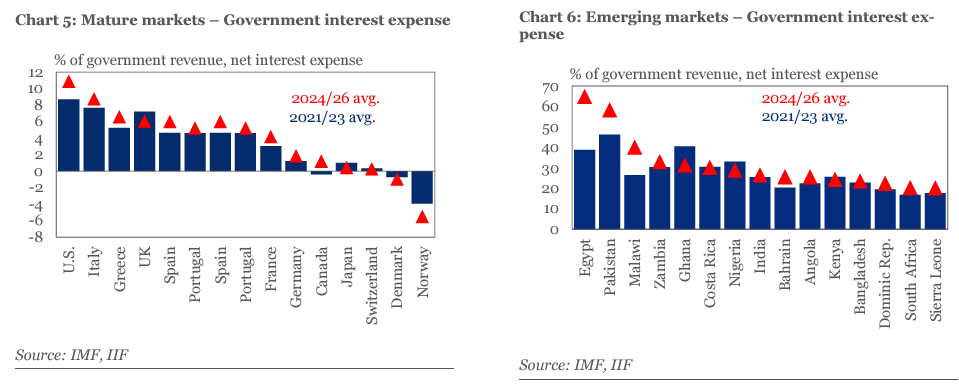

One Chart You Should Not Miss: Global Debt Reaches $315 T and 333% of GDP

Based on the recent Institute of International Finance (IIF) report, global debt reached $315 trillion as of Q1 2024 2024 from 320% in 2016. Total global debt has risen 21% since 2020.

While the U.S. and Japan were the largest contributors across developed countries, China, India, and Mexico drove the largest share in emerging markets.

More concerning is the rise of net interest expense (debt servicing costs) as a percentage of government revenue in the developed countries (led by the jump in the US).

One Term to Know: ETFs vs. Closed-End Funds

Exchange-traded funds (ETFs) are mostly passively managed (can also be actively managed), tracking an underlying basket of securities (like the stocks in the S&P 500 index). They are listed on the stock exchange and traded all day. ETFs are open-end funds, meaning their assets under management (AUM) can grow and the number of shares can increase as the number of investors increases.

A closed-end fund (CEF) is a type of mutual fund that can trade all day but unlike ETFs has a fixed number of shares after the initial IPO. Their AUM does not grow so investors trade in and out the shares of a closed-end fund in the secondary market.

CEFs usually have a higher expense ratio than ETFs as they are actively managed. CEFs have a distinct feature — the price of the CEF can be below (discount) or above (premium) its net asset value depending on the supply and demand of investors. ETFs typically trade close to their net asset value unless there are huge market disruptions.

ETFs provide beta returns (tracking the market) but CEFs can provide alpha (excess returns over the market).

[🌻] Things I Learn About AI/Productivity:

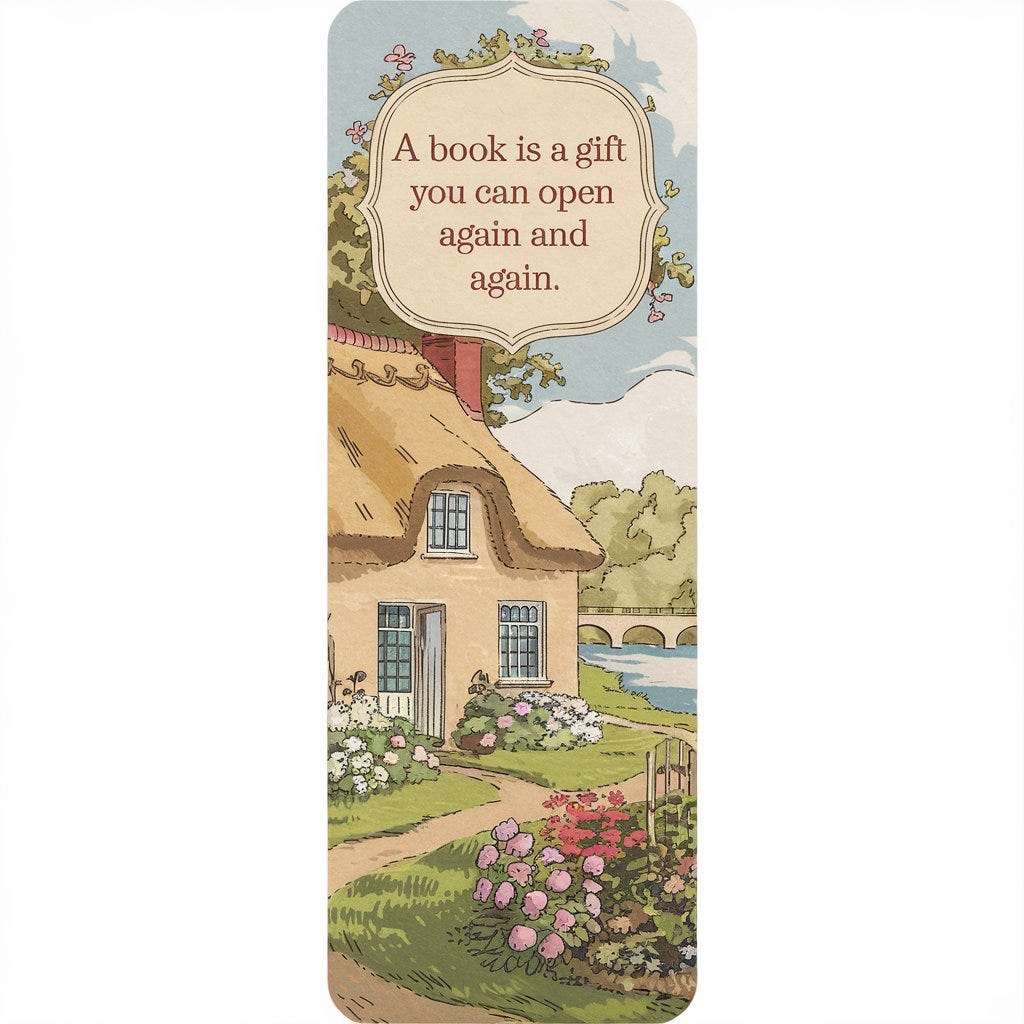

Often we want to create a design to showcase our brand image for a company logo, a T-shirt, an announcement, a book cover, etc. Ideogram.ai comes in handy to express what we want to see.

It is easy to use. Type in what you need (text-to-image) in Ideogram. In my case, I want to design a bookmark in a Jane Austen cottage and garden background with the words “A book is a gift you can open again and again.”

Keep the “Magin Prompt” on and hit “Generate”.

My Prompt: A bookmark with a Jane Austen-style cottage and garden in the background with words saying "A book is a gift you can open again and again".

Magic Prompt: A bookmark with an illustration of a Jane Austen-style cottage with a thatched roof and a garden with flowers. In the background, there is a river and a bridge. There is a quote on the bookmark that says, "A book is a gift you can open again and again." The overall design is in a vintage style.

To remix, you can adjust the colour palette and the image weight. The free plan provides 10 slow credits/day for up to 40 images.

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.