Weekly Good Reads: 5-1-1

Complacency, Soft-landing, Novo Nordisk CEO interview, Mental Health, Largest Stock Markets, Tightwads

Welcome to Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

In this Weekly, I share insightful/essential readings, charts, and one term, incorporating some of my market observations and weekly change tables. I look beyond data and share something enlightening about life, health, technology, and the world around us 🌍!

Here’s the quote of the week:

Peace is not the absence of conflict, but the ability to cope with it. ~ Dorothy Thomas

Feedback is important to me, so if you like the Weekly, please “heart” it, comment, share it, or subscribe! Thank you so much for your support🙏.

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

Market and Data Comments

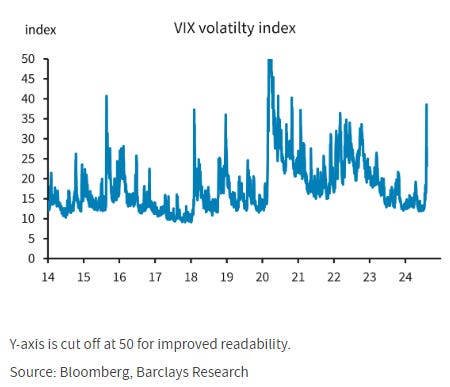

There have been various attempts to explain the multi-currents (fundamentals + overcrowded positions + technicals) behind the gregorious market sell-off and volatility index surge (to 65 intraday!) on Monday, August 5 (see Econ/Invest #1 for a comprehensive discussion.) Even MrsDowJones’s Instagram reel caught my eye!

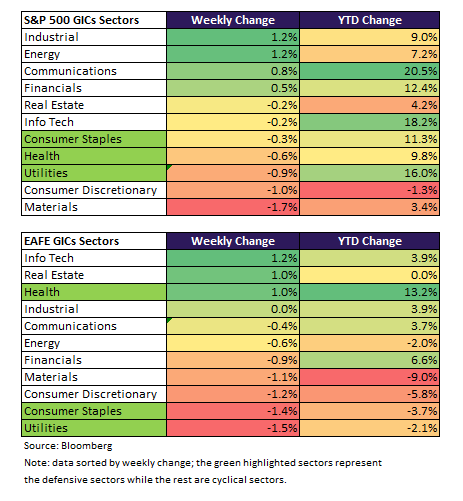

By the end of the week, global markets (MSCI ACWI) and the S&P 500 were flat (!), US 10-year government bond rose 15 bp to 3.94%, crude oil shot up 4.5%, VIX (stock volatility) dropped 3% to 20.37%, and MOVE (bond volatility) dropped 4 points to 108.8.

Small-cap stocks and bitcoin notably dropped 1.3% and 2.8% respectively this week.

As one fund manager in the FT article commented:

When funds that invest in momentum reverse course you can expect a “sharp reaction”, says Shep Perkins, the chief investment officer for equities for Putnam Investments, an asset manager owned by Franklin Templeton.

“There’s a saying: stability breeds fragility,” he adds. “The stability led to complacency and the market was testing folks to say, ‘hey do you know what you own?’

This week’s economic data on July Services ISM (grew at 51.4%), initial weekly claims (fell 17,000), and Q2 Senior Loan Officer Opinion Survey on Bank’s Lending Practices (showed less reporting tightening standards than in Q1) calmed the market’s nerves that soft-landing is still on track. Overall, the S&P companies (the other 493 than the Magnificent 7) have seen rising net income growth.

No doubt, US consumers are cutting back on spending, with inflation especially felt by the bottom 40% of the income distribution. A $50 meal is now a $75 meal making MacDonald’s “$5 Meal Deal” very popular.

Still, while US economic data is surprising on the downside, they do not normally incite the volatility experienced by the market on Monday (see the 2 graphs below).

Economist Robert Shiller in 1981 in his famous paper “Do Stock Prices Move Too Much To Be Justified by the Subsequent Changes in Dividends” discussed the excess volatility puzzle. While economic data plays a part, Barclays said the market moves have been far larger than justified by the macro fundamentals, and that can be explained by the simultaneous unwinding/ forced selling of crowded and long-held (one-way) positions after an unusually long period of low stock market volatility.

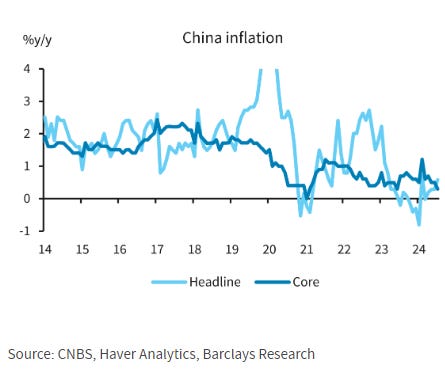

Looking to China, while no one there cheered about the near deflation CPI data (bad signs) and slowing exports data, the central bank is “struggling” to cut interest rates further this year to buffer the weakening economy. Why struggling? The central bank has been worried about the bond bubble. The strong dollar and the Fed holding interest rates have exacerbated the Chinese Yuan weakness (dropping 2% before the big rally on August 2 and 5 as the “Yuan carry trade” was unwound) so cutting rates further would further weaken the Yuan. Chinese bond yield has rallied by 36bp YTD to 2.11% as Chinese banks and investors continued to chase Chinese bonds as the economy falters.

With the US Treasury yield rallying, the Chinese and US 10-year government bond yield differential narrowed towards -1.5% from an April low of -2.5%, giving China more room to cut interest rates to buffer their economic weakness.

In Japan, the Bank of Japan turned dovish saying as long as markets are unstable (YTD the USD return is almost flat from +14% as of March 2024), they will not hike interest rates further. While they need to gradually move real interest rates to 1% from too low a level currently to normalize monetary conditions according to the underlying inflation, they are unlikely to hike rates further this year.

This coming week we will monitor the US July PPI on Tuesday, CPI on Wednesday, retail sales on Thursday, housing starts on Friday, the UK July CPI June weekly earnings and unemployment rate on Tuesday, July CPI on Wednesday, and China’s August 1Y MLF rate, July industrial production, retail sales, and YTD fixed asset investments on Thursday.

Economy and Investments (Links):

The Meaning of the Market Sell-off (FT or via Archive)

The Great Sell-Off and Why the Japanese Market Trades Like a Penny Stock (FT or via Archive)

Will America’s Economy Swing the Election? (The Economist or via Archive)

Finance/Wealth (Link):

Leaders With Lacqua: Novo Nordisk CEO Lars Fruergaard Jørgensen (Bloomberg Interview)

As many might know, Novo Nordisk is the most valuable European company with a current market capitalization of about $540 billion, 33% larger than the Danish economy, where it is based.

The CEO, highly strategic, disciplined, and unassuming, mentioned many gems with authenticity in this brief interview including these:

Most products are priced based on the value they bring, and I feel very good about the value of our medicines to our individual patients and the health care system……80% of health care system is linked to chronic care…and we have a portfolio of medicines addressing diabetes, obesity, and their comobilities…by 2035, cost burden to society will be estimated at $4 tillion of the people living with obesity, costs largely taken up by the health care system…we value our medicines in terms of costs and value of preventing people out of the hostpial.

I am not a specialist in anything…I am borne with a big nose and big ears. I use attributes each and everyday to collect opinions from the company, and it is my role to combine those into an opinion together with my team to make sure we make the right choice.

My best piece of advice: give people a fair chance to succeed…trust people and give them what they need to succeed.

+ T Rowe Price Retirement Income Calculator with Inflation Adjustment (Investopedia calls it one of the best online (free) retirement income calculators out there)

Wellness/Idea (Link):

+ Olympic Athletes Struggle with Mental Health too. Here's How to Talk to Your Kids About it (National Geographic)

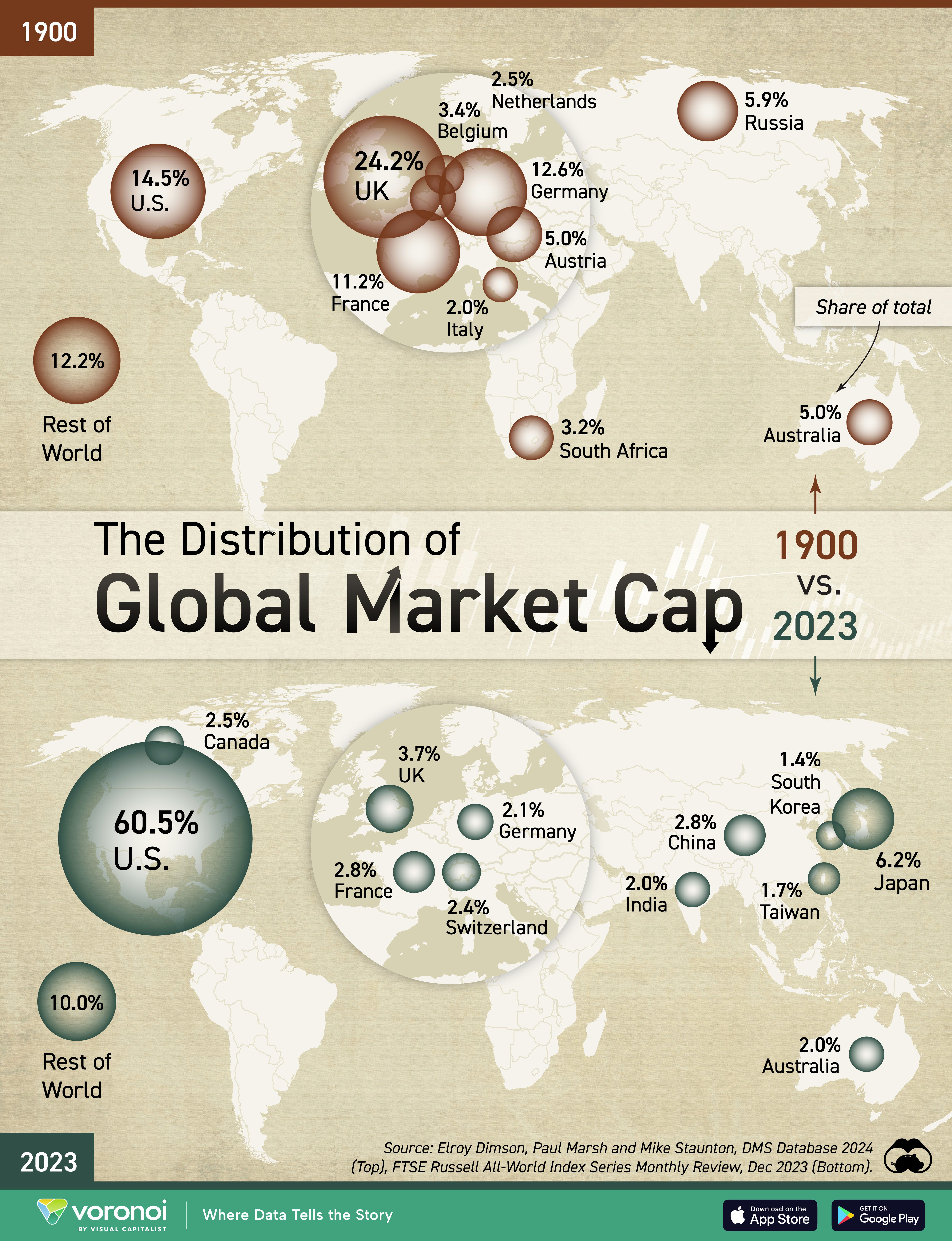

One Chart You Should Not Miss: World’s Largest Stock Markets (1900 vs. 2023)

In 1900, the wealth centres were in the UK and Europe. Now, it is the US (with 6 of the world’s trillion-dollar companies), followed by APAC. In 100 years, what may it be? Surely, the US cannot be 100% of the global market cap. I believe APAC will approach 2x the market cap of Western Europe.

One Term to Know: Tightwads

The Cambridge Dictionary defines a tightwad as “a person who is not willing to spend money” (守財奴 in Chinese, agarrado in Spanish, pão-duro in Portugal…)

The word originated around c1805 and comes “from the idea that a man (or woman) holds their “wad” of money (either a roll or folded amount of paper money) tightly in their hand, thereby refusing to part with it, either by force or desire.

In this Atlantic article (Archive), which quoted Scott Rick, a marketing professor at the University of Michigan:

“Rick has found that tightwads do not scrimp because they lack money. They are not any poorer than spendthrifts (people who overspend); tightwads actually have better credit scores and more money in savings. (Perhaps because they never spend it.) Instead, they’re afraid to spend money that they do have. Tightwads’ issues reveal how our financial choices can be more psychological than economic. If you feel anxiety about your finances, it might not be relieved by making more money.”

Tightwads’ behaviour is influenced by personal values, past experiences (e.g. a bad laid-off, growing up during the Great Recession), watching their immigrant parents who saved up everything for the sake of the children’s education, future, etc.

I believe weighing the opportunity costs of buying something (while giving up on another) is a healthy habit, but if panic overrules you in making spending decisions when you have more than enough means, the behaviour indicates something much deeper in your psychology, and it is important to ask yourself deeper questions “what is my belief, and is that true?”

[🌻] Things I Learn About AI/Productivity:

Edit Photos with AI: Magic Editor, Magic Eraser & Unblur (Google)

I am enjoying this new Google Photos capability from my iPhone - blur background for a portrait, unblur faces, erase objects, remove distractions, enhance lighting, and turn photos into 3D videos/ movies (if you pay for Google One). Don’t think I need any more other photo apps!

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.