Weekly Good Reads: 5-1-1

Core PCE, Election Uncertainty, Sector Rotation, Global Wealth Report, Eating Habits, Minsky's Moment

Welcome to Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

Each week I share insightful/essential readings, charts, and one term, incorporating some of my market observations and weekly change tables. I look beyond data and share something enlightening about life, health, technology, and the world around us 🌍!

Here’s the quote of the week:

Big ideas come from the unconscious. This is true in art, in science, and in advertising. But your unconscious has to be well informed, or your idea will be irrelevant. Stuff your conscious mind with information, then unhook your rational thought process.

~ David Ogilvy

Feedback is important to me, so if you like the Weekly, please “heart” it, comment, share it, or subscribe! Thank you so much for your support🙏.

Conversations with Female Investors and more (to inspire more females into finance and investment careers 🙌.)

Market and Data Comments

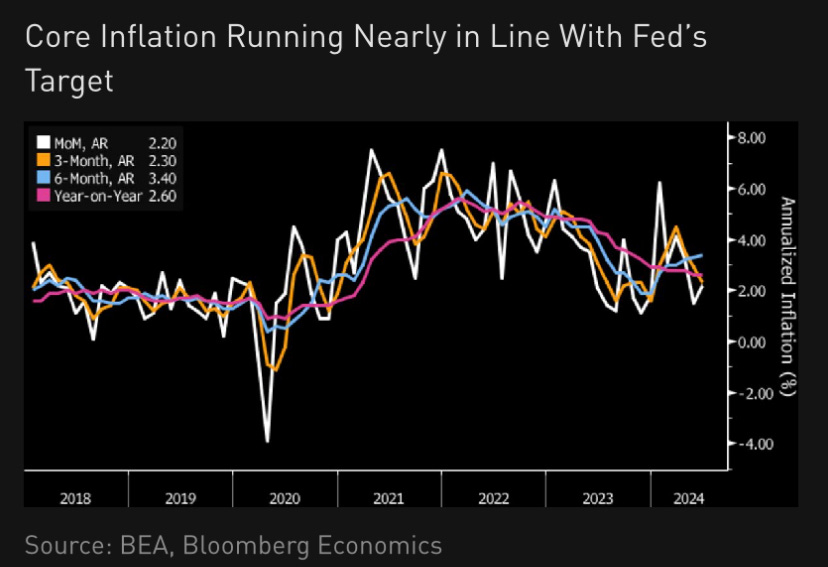

The core PCE price index rose 0.2% m/m in June (+2.3% 3m annualized and +2.6% y/y) while Powell’s preferred inflation gauge, the Supercore PCE inflation, rose 0.2% m/m with the 3-month annualized rate easing to 2.7% (from 3.6% prior). Personal spending increased 0.3% in June (inline) while personal income increased just 0.2% (from 0.4% prior, lower than expected.)

A Fed rate cut is likely within view (see Econ/Invest #1). This reflects three factors: “better news on inflation, signs that labor markets are cooling and a changing calculus of the dueling risks of allowing inflation to remain too high and of causing unnecessary economic weakness (WSJ).”

Recall that when the Fed first hiked the Fed Funds to its current level of 5.33% in August 2023, core PCE inflation was about 3.7%, it is now 2.6%, meaning financial conditions have tightened (see chart above). If the Fed cuts the rate when the labour market already falters, it will be hard to bring the labour market back on track.

The market is now comfortably pricing in two rate cuts starting in September.

The US also reported a stronger-than-expected Q2 real GDP at 2.8% annualized (vs. +1.5% in Q1), driven by robust consumer spending, increased government expenditures, and a notable inventory buildup. As recently concluded by Apollo’s Torsten Slok looking at higher frequency economic data: “there is nothing suggesting that the economy is currently in a recession or about to enter a recession.”

Coinciding with more election uncertainty in the US (as likely Democratic Presidential Nominee Harris reportedly has erased Trump leads (WSJ)), investors have been shedding technology and communications AI-themed stocks in favour of other beneficiaries of AI including utilities, energy infrastructure (transformers), clean energy, data centres (benefiting real estate REITs), and AI end-users such as industrials (Deere & Co.) and health care (pharmaceuticals in drug development) (see Econ/Invest No. 3).

Looking at YTD performance (Weekly Changes table below), the S&P 500 returned 14.5%, similar to the Nasdaq’s at 15.6%. In comparison, the equally-weighted S&P defensive sectors rose by a very similar amount as the equally-weighted S&P cyclical sectors (+10.5% vs. +10.8%) reflecting the market rally has broadened. The small-caps stocks have also caught up, rising 11.5% YTD.

From Morgan Stanley and Factset, we can see the market is expecting a rebound in Q2 earnings growth (~ 9%) and has high expectations for Q4 and Q125. Looking towards 2025, EPS growth expectation is the strongest for Info Tech, Health Care, and Materials (vs. Consumer Services, Info Tech, and Financials in 2024) and the lowest for Utilities, Consumer Staples, and REITs (REITs, Materials, and Energy in 2024).

Central bank actions will be in focus next week. The Fed is expected to stay put while there is a 50:50 chance the Bank of England will start cutting interest rates by 25bp next week as inflation continues to cool, while the Bank of Japan may hike as wage pressure increases and the weakness of the Japanese Yen poses a risk to the inflation outlook.

China has already surprised the market with an interest cut this past week following an 11-month pause: the 7-day OMO rate was lowered 10bp to 1.7% and the 1y MLF rate was lowered 20bp likely to buffer the weak economy and deflationary pressures. Nevertheless, President Xi is seen to prioritize security rather than growth in the face of the tough stance of the US and Europe towards China, leading to China’s securing its own supply chain and focusing on growth in innovations including electric vehicles and AI.

This coming week we will monitor the US FOMC rate decision and the Fed’s press conference on Wednesday, the July ISM manufacturing index on Thursday, July non-farm payrolls, unemployment rate, and average hourly earnings on Friday, the Bank of England rate decision on Thursday, the Bank of Japan monetary policy meeting on Wednesday, the Euro Area Q2 real GDP on Tuesday, and more US earnings reports.

Economy and Investments (Links):

A Fed Rate Cut Is Finally Within View (WSJ or via Archive)

The Next 100 Days (The Atlantic Daily or via Archive)

Great Rotation Trade Sees Investors Dump AI Giants for Less Obvious Stocks (Bloomberg or via Archive)

Investors are selling AI giants to snap up smaller stocks and defensives that had lagged behind. That rotation coincides with the AI theme’s expansion to areas beyond chips and software, including the vast amounts of power and land the technology requires as well as what industries may eventually benefit from its implementation.

Finance/Wealth (Link):

Understand Customer Mindsets to Make Every Holiday and Peak Sale Connection Count (Think with Google)

Shoppers fluidly move through different mindsets — deliberate, deal-seeking, determined, and devoted — as they approach seasonal moments. While people usually exhibit a combination of the four behaviors, some are more prominent as shoppers move closer to a specific sales day or cultural moment. By aligning your brand strategy to these mindsets, you can strengthen your customer connections and drive greater results at each crucial stage.

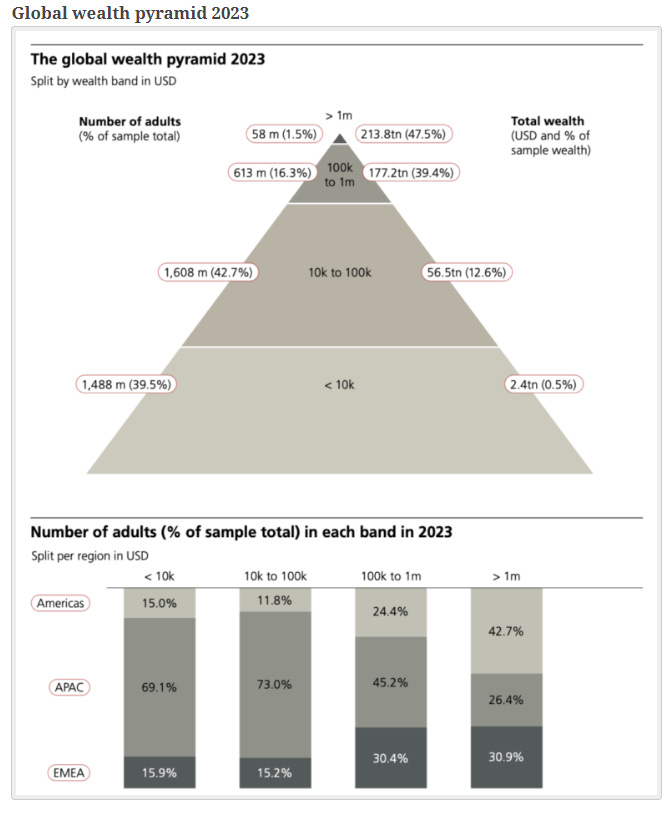

+ UBS Global Wealth Report 2024 (UBS via Ben Carlson)

Wealth is steadily growing throughout the world – albeit at different speeds – with very few exceptions. The proportion of people in the world with the lowest wealth (under USD 10,000) has nearly halved since 2000, while the proportion of people in every other wealth bracket has grown.

Wellness/Idea (Link):

8 Eating Habits That Actually Improve Your Sleep (Time)

“We need tryptophan in combination with carbohydrate-rich foods,” says Arman Arab, a postdoctoral fellow at Harvard Medical School who specializes in nutrition.

The Mediterranean diet is one regimen loaded with both tryptophan and healthy carbs—those with plenty of fiber. Like carbs, nutrients such as zinc, B vitamins, and magnesium play key roles in converting tryptophan into melatonin for better sleep, and the Mediterranean diet delivers each of these components. Spinach, barley, and whole wheat are great mates for tryptophan-rich foods. Arab recently found that people who follow the Mediterranean diet have better sleep quality and less insomnia. St-Onge has researched similar associations.”

One Chart You Should Not Miss: Inequality from Temperature-Related Deaths

From Our World in Data research sourced from Human Climate Horizons (2024), heat mortality reveals deep inequalities between those driving climate change and those suffering the most from the consequences.

While few people across Europe and North America will die from climate change, deaths in poorer countries will likely increase.

By plotting the projected change in death rates in 2050 against the current gross domestic product (GDP) per person, we can see death rates are projected to increase in many of the poorest countries (to the left) and decrease in most rich countries (right)

One Term to Know: Minsky’s Moment

The Economist defines the Minsky’s Moment as “a sudden collapse in market sentiment.” This was named after the economist Hyman Minsky, who grew up during the Depression and developed his “financial-instability hypothesis”. The theory examines how long stretches of prosperity sow the seeds of the next crisis, an important lens for understanding the causes of the Great Recession in 2007-2009. Economic stability (prosperity) breeds instability.

As asset prices rise, investors become more and more confident and leverage up to finance their positions, regardless of valuations. At some point, debt levels reach a breaking point and asset prices start to plunge across the board as investors need to sell to repay their debts (exiting all at the same time), leading prices to plunge even further.

For fund managers, the “Minsky’s Moment” is synonymous with a financial crisis.

Minsky’s theory attacked the prevalent efficient market theory which states that markets tend towards equilibrium as people digest all information so financial system structure is almost ignored. However, Minsky believed deep-seated forces in financial systems propel them towards trouble with stability a fleeting illusion. His theory is most relevant for advanced capitalist societies with deep and sophisticated markets and is not meant for all economies.

While his theory has been criticised as not quantified into elegant models as Minsky tried to explain debt and the dangers of financial innovation according to experience, central bankers including Janet Yellen (US) and Mervyn King (UK) praised and cited his work.

“Minsky’s Moment” does peter out. But as banks and investors become complacent again and take unnecessary risks, a financial crisis is more likely than not to happen again.

[🌻] Things I Learn About AI/Productivity:

5 Ways SearchGPT is Very Different Than Google Search (Tom’s Guide)

Perhaps the most underrated difference between SearchGPT and Google Search is that OpenAI promises that it's working with publishers and reporters to keep journalism at the forefront of its efforts. "We are committed to a thriving ecosystem of publishers and creators. We hope to help users discover publisher sites and experiences, while bringing more choice to search," said the company.

JPMorgan Pitches In-House Chatbot as AI-based Research Analyst (FT)

JPM has announced the launch of its own version of the ChatGPT product, which can allegedly do the work of a research analyst.

The US bank has given employees of its asset and wealth management division access to a large language model platform which the bank is calling LLM Suite, according to an internal memo seen by the Financial Times. Executives told staff LLM Suite can help them with writing, idea generation and summarising documents through access to third-party models.

When things line up unexpectedly but magically at the Paris Olympics - full moon behind the ring (Source: @Gregmartin11)

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more.

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.