Weekly Good Reads: 5-1-1

Slowing PCE Inflation, Election Jitters, Active Funds Underperformance, Green Bonds, Brain Health, 100 School

Welcome to Weekly Good Reads 5-1-1 by Marianne, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

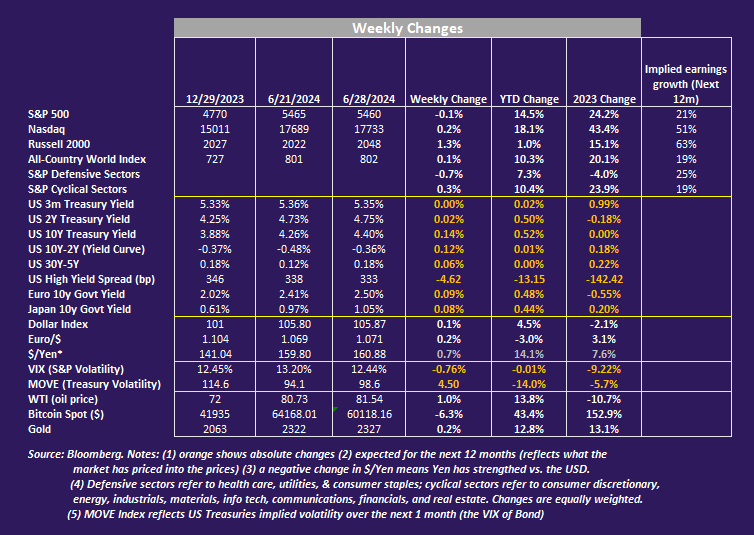

Each week I share insightful/essential readings, charts, and one term, incorporating some of my market observations. You can find the weekly changes of the major indices or indicators in the Weekly Change charts. But I look beyond data and share something enlightening about life, health, technology, and the world around us 🌍!

Here’s the quote of the week:

[On productivity]: Direct your energy toward figuring out how to start what you want to do rather than thinking about how to shorten what you don't want to do. ~ James Clear

I archived my Weeklies here and the index of charts and terms here. Check out my conversations with Female Investors and more, which I hope will inspire more females into finance and investment careers 🙌. Easily subscribe to my newsletter by clicking below.

Feedback is important to me, so if you like the Weekly, please “heart” it, comment or share it with your contacts. Thank you so much for your support🙏.

Market and Data Comments

The economic focus this week is inflation (again!) May PCE inflation was 0.0% m/m (0.3% prior), core PCE (Fed’s preferred measure) was 0.08% m/m (0.3% prior), and supercore PCE (Powell’s preferred measure) was 0.1% m/m (0.3% prior). Core PCE was at 2.6% y/y, the lowest level since March 2021, helped by lower gasoline and durable goods inflation.

Bloomberg however was sceptical about the persistent disinflation as core services inflation still looks sticky. One of the problems is the methodology for calculating CPI vs. PCE where the imprecise measure of housing rents (owner equivalent rent or OER) are included in both, with more weights in CPI and fewer in PCE.

OER lags market rents, and the gap between CPI and PCE has widened (see Econ/Invest #1 and graph). Bosten Fed economists estimated CPI would be 1.6% higher between June 2024 and June 2025 had the gap not existed. The higher number, in addition to the sticky health care costs, could impact monetary policy direction, higher for longer.

In May, income growth jumped 0.6% m/m while personal spending grew lower than expected at 0.2% (0.1% prior) - the Americans’ summer travel plan concurs on slowing spending. In addition, May US housing starts (1.277 million units), a leading indicator, was -5.5% from a year ago.

The Big Picture has an interesting chart about how inflation is visible to consumers but wage growth is not, showing cumulative wage growth has exceeded that of cumulative CPI inflation since February 2020 (the start of the Pandemic) (read Econ/Invest #1 - Related).

Elsewhere, the market has been focusing on the dollar action (up 4.5% YTD) which stays strong vs. all major currencies. The view was reinforced after the first US Presidential debate on Thursday night (bets leaning even more toward a Trump victory, but really “we all lost” as the Washington Post article posited.)

Elections in the US, France, and the UK seemingly are driving economic outlook rather than the other way around as the incumbent party/president is losing ahead of the respective elections.

In China, the market awaits the Third Plenum which will happen on July 15 to 18, a 6-month delay. While investors are awaiting more demand-side stimulus and better distribution of national income, President Xi seems more open to optimizing the growth for private enterprises, awakened to the fact foreign investment flows into China declined last year for the first time.

Here’s a quick summary of how major assets/markets have done in 1H this year - the large and small-cap stocks’ performances have significantly diverged.

This coming week we will monitor elections in France on Sunday (first round) and the UK (General Election) on Thursday, the June US ISM manufacturing index on Monday, the FOMC minutes on Wednesday, and the June nonfarm payrolls, unemployment rate, and average hourly earnings on Friday, the Euro area June manufacturing PMI, and China June NBS manufacturing PMI on Sunday and Caixin manufacturing PMI on Monday.

Economy and Investments (Links):

+ Related: Inflation is Obvious But Wage Gains Seem Invisible (The Big Picture)

It’s an AI Market Now (FT or via Archive)

The other 484 companies [in S&P 500] in the index have risen in value by 20 per cent. They are having a big rally, too, just not as huge as when the AI mob is included…

All of the gains in the market [since March 28, 2024]— and more — are from companies touched by AI. The S&P 500 as a whole is up more than 4 per cent. The non-AI 484 is down 2 per cent.

Finance/Wealth (Link):

The Nocebo Effect: Why You Must Eradicate Negative Expectations (Darius Foroux)

Nocebo simply refers to your self-talk. Particularly when you want to do hard things, don’t make everything worse in your mind by talking negatively about it…

Watch out for negative thinking patterns. It can truly hurt your health, mindset, work, relationships, and financial decisions.

Wellness/Idea (Link)

I’m a Neurologist. Here’s the One Thing I Do Every Day for My Long-Term Brain Health (Self)

Consistently training your brain will help boost your cognitive processes over time, because the myelin sheath—the layer of protein that coats your nerves—thickens. A plumper myelin sheath helps your brain transmit and process information more efficiently.

+ The Gifts of 40 (@The Looking Glass by

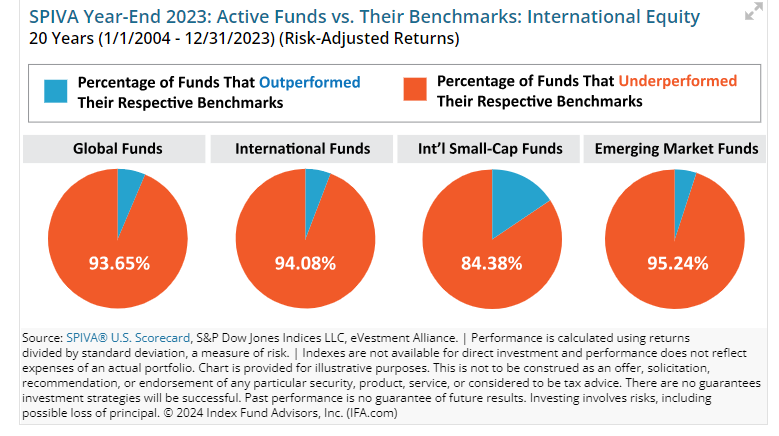

) - This is seriously good with so much wisdom - a must-read!One Chart You Should Not Miss: US Equity Funds Underforming Their Benchmarks (SPIVA)

The S&P Global SPIVA US Scorecard year after year lays down the argument that most active equity managers cannot beat their respective benchmarks (going back to 2002).

SPIVA found that "across all categories, underperformance rates typically rose as time horizons lengthened." This is true whether in good times or bad times—it is hard to pick star managers and impossible to time the market.

The first chart shows the comparisons based on absolute returns while the second chart shows the comparison based on risk-adjusted returns (returns dividend by historical volatility.)

For global equity funds (third chart), same conclusion. As of the end of 2023, passive fund assets exceeded those of active funds after years of getting into the turf of the active counterparts.

In investing, pay attention to after-fee returns.

One Term to Know: Green Bonds

Green bonds are debt instruments issued by governments or corporations and work like regular bonds except the money raised from investors is used exclusively to finance projects having a positive environmental impact, such as renewable energy, low carbon transportation, green buildings, wastewater management, etc.

Green bonds are backed by the issuer’s entire balance sheet. Some examples of green bonds are revenue bonds, green project bonds, and green securitised bonds.

The first Green Bond was issued by the European Investment Bank (lending arm of the EU) in 2007, followed by the World Bank.

Between 2014 and 2023, the US has been the largest issuer of Green Bonds ($454 bn), followed by China and Germany.

Issuance of green, social, sustainable, and sustainability-linked bonds hit a record high in Q1 2024 with the accumulated outstanding amounting to $4.7 trillion (Climate Bonds Initiative), still a fraction of the global bond markets at $130 tn.

The premium for Green Bonds has gradually disappeared as green bond issuance has grown rapidly, meaning investors now enjoy similar yields of Green Bonds as regular bonds, making this an attractive alternative to bonds, especially when major governments prioritize sustainability.

[🌻] Things I Learn About AI/Productivity:

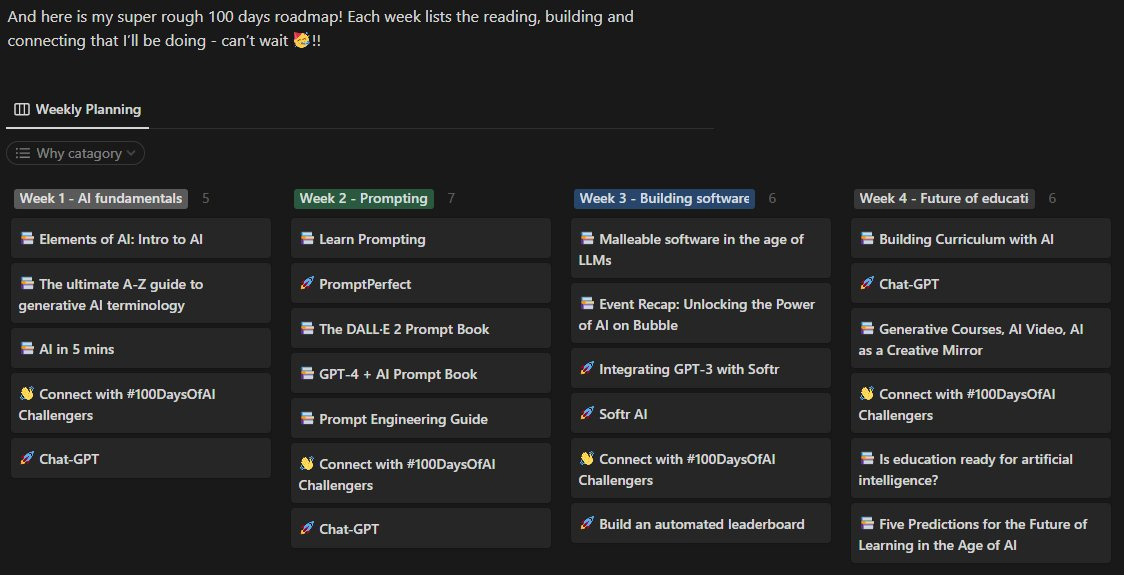

100 School: Learn AI skills in 100 days with daily bite-sized lessons - @100daysai (starting July 1)

100 School: Learn No-Code in 100 days with daily bite-sized lessons - @100daysnocode (starting July 1)

I have signed up for #100daysai. From what I can tell, users’ feedback on Twitter has been positive for both challenges launched previously. The founder of 100 Day School is Max Haining.

Weekly planning from the last cohort:

+ ‘How does ChatGPT ‘think’? Psychology and Neuroscience Crack Open AI Large Language Models (Nature)

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more. Stay tuned for next week’s insightful conversation with an Indian Female Fund Manager.

Also, if you miss my latest post about investing, please read it here:

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

Great write up as usual! The stats about travel surprised me a bit. 39% said they can’t afford it, yet the airports are busier than ever. I see it with my own eyes, and the stats from TSA over recent months seem to confirm it.