Weekly Good Reads: 5-1-1

FOMC, French Election, Dollar Dominance, Apple Intelligence, Ultra-Wealthy, Market Timing

Welcome to Weekly Good Reads 5-1-1! It’s Marianne here, a 25-year investment practitioner writing about investing, economy, wellness, and something new I learned in AI/productivity.

Each week I share insightful/essential readings, charts, and one term, incorporating some of my market observations. You can find the weekly changes of the major indices or indicators in the 2 Weekly Change charts. But I look beyond data and share something enlightening about life, health, technology, and the world around us 🌍!

Here’s the quote of the week:

Move toward the next thing, not away from the last thing. Same direction. Completely different energy. ~ James Clear

I archived my Weeklies here and the index of charts and terms here. Check out my conversations with Female Investors and more, which I hope will inspire more females into finance and investment careers 🙌. Easily subscribe to my newsletter by clicking below.

Feedback is important to me, so if you like the Weekly, please “heart” it, comment or share it with your contacts. Thank you so much for your support🙏.

Market and Data Comments

The US stock and bond markets cheered two softer-than-expected inflation numbers this week. The May core CPI was +0.2% m/m (0.3% prior) and +3.4% y/y (3.6% prior) while the May core PPI was +0% m/m (0.5% prior) and 3.2% y/y (3.2% prior). Bloomberg estimated the upcoming May core PCE deflator may be ~ 2.6% y/y (2.8% prior), the lowest number since March 21.

From the chart above, Robin Brooks (Brookings) compared the monthly core CPI in 2023 and 2024, saying how similar the 2 paths were. The higher Q1 inflation was due to price resets in both years.

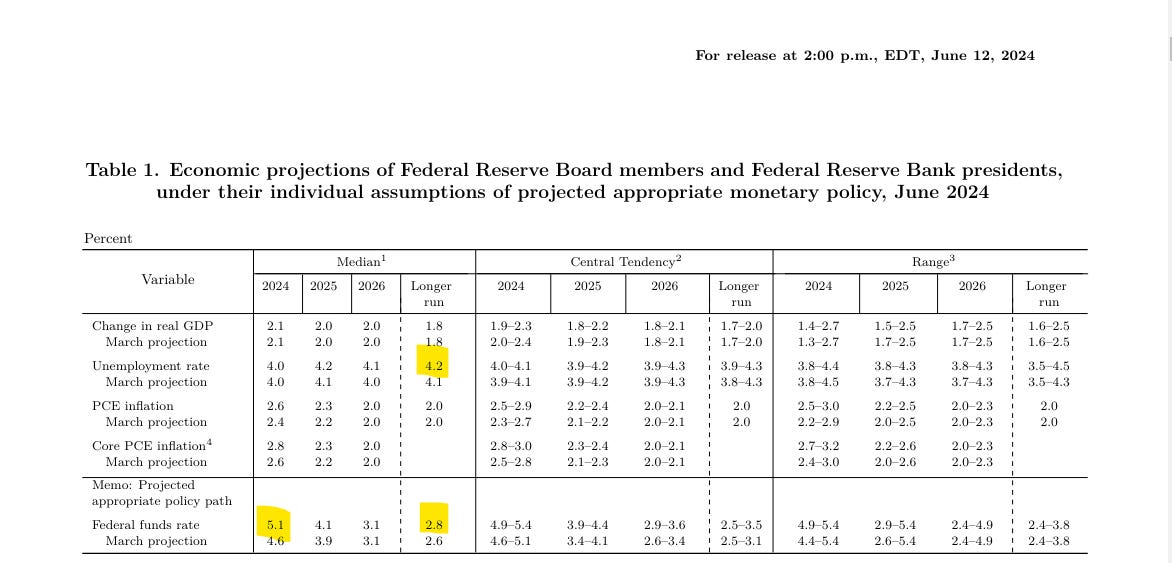

The Fed held the US interest rate unchanged at 5.25%-5.5% and revised the median Fed Funds projection by the end of 2024 to 1 cut (green line below) instead of 3 cuts projected in March. 4 rate cuts are projected in 2025 (median plot).

In the Fed’s June SEP (Summary of Economic Projections), noticeable changes are the bump up in their end-2024 Core PCE inflation by 0.2% to 2.8% and the long-run CPI to 2.8% (+0.2% vs. March) - see table below.

The market is still expecting 2 rate cuts, taking the cue from the softer inflation numbers and the signal by Powell they are inclined to cut rates this year. Powell said that the SEP is less important than the “totality of data” and how that affects the unemployment and inflation outlook, staying flexible to cut rates if data warrant it.

Whether the US consumers care more about unemployment or inflation, two economists at the Federal Reserve Board find that people would only tolerate a 0.6% increase in unemployment to reduce inflation by 1% (so overall people care more about unemployment seemingly - Fed’s cue?) The latest initial jobless claims rose to 272,000 (4-week moving average), the highest since September 2023.

While it is risk-on in the US, the EU’s financial markets were rattled by the prospect of a far-right government (not a lot of fiscal responsibility) and left-wing opposition in France. The French market dropped 7.1% this week after President Macron called a snap Parliamentary election last Sunday, dragging down the Euro 600 index, which ended down 3.3% for the week (see Econ/Invest #2), while investors fled to EU bonds for safety.

Stepping back, global macro is benign with expected 2024 global real GDP growth to be 3.1% (Barclays), helped by better estimates on the EU and Chinese growth.

A 2 to 3% inflation scenario historically has been the most favourable for S&P 500 stock market returns (JPM). YTD, however, the S&P 500 is already up close to 14%, with only one-quarter of the stocks beating the S&P index return.

At the same time, cash and bond yields are welcome choices in asset allocation.

This coming week, we will monitor the G7 Summit, US May retail sales on Tuesday and May housing starts on Thursday, the Euro Area May inflation on Tuesday and June Composite PMI on Friday, the May CPI in the UK on Wednesday and the Bank of England rate decision on Thursday, May inflation in Japan on Friday, and China’s May industrial production, retail sales, and fixed asset investment (YTD) in China on Monday.

Economy and Investments (Links):

Fed Officials Dial Back Rate Forecasts, Signal Just One ‘24 Cut (Bloomberg or via Archive)

Why French Elections are Rattling Markets (Axios Macro)

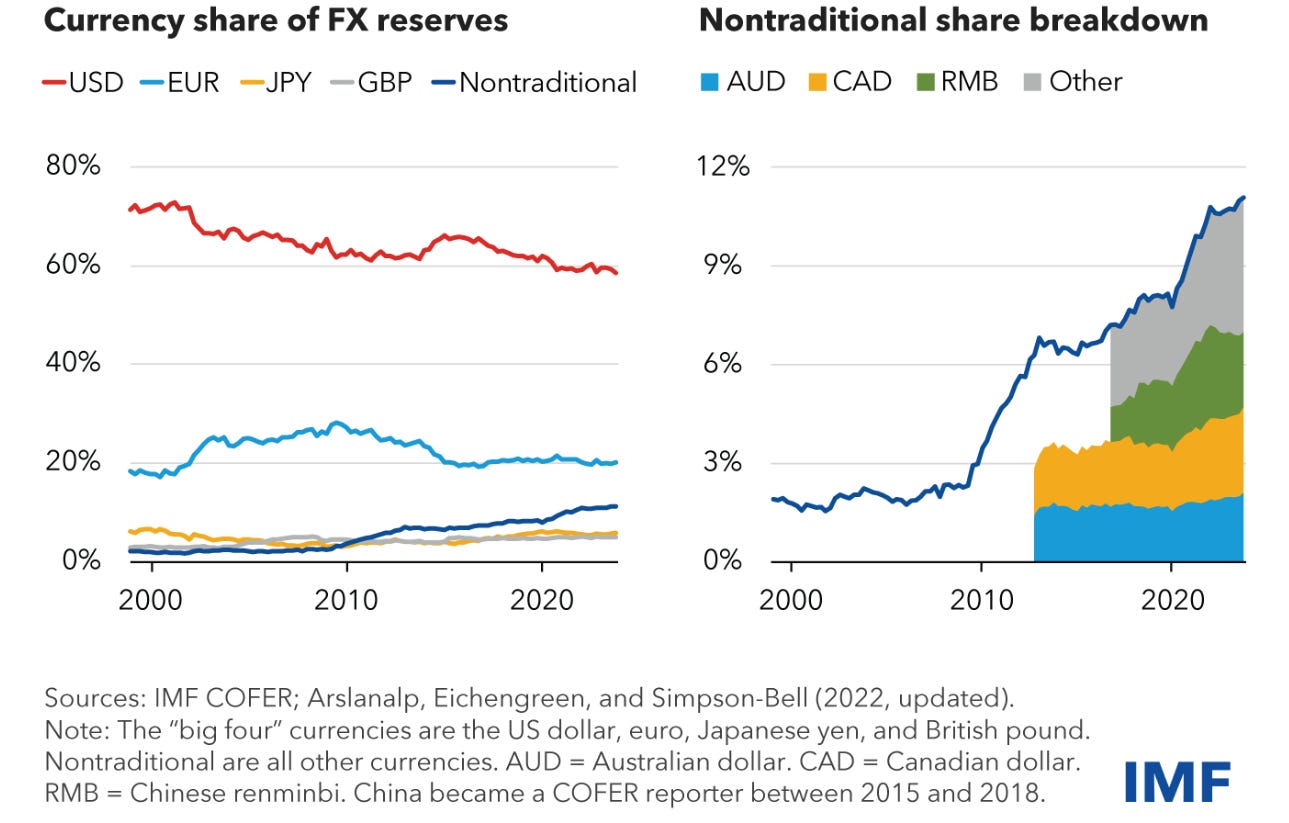

While the US Dollar is still the dominant reserve currency, its global share of FX reserves has been on the decline since 2020 (from about 71% to just under 60%). But its decline is not accompanied by the traditional currencies share going up but by the share of the non-traditional currencies rising: Chinese renminbi (especially), Australian dollar, Canadian dollar, South Korean won, Singaporean dollar, and the Nordic currencies.

Finance/Wealth (Link):

Useful and Overlooked Skills (Morgan Housel, Collab Fund)

This one particularly resonates with me, especially in pursuit of investment returns:

Respecting luck as much as you respect risk…

The ability to recognize that your wins might not signal that you did anything right in the same way your losses might not signal you did anything wrong is vital to learning something valuable from real-world feedback.

Wellness/Idea (Link)

Second Mouse.AI (Scott Galloway, No Mercy/ No Mallace)

After reading the piece, you will fully appreciate Apple's business model and the AI (Apple Intelligence) brilliance (and the market quickly figured out after the initial downbeat response to Apple’s AI announcement).

“Apple Intelligence” is more than a great brand move; it encapsulates the company’s strategy. Take something invented elsewhere; make it more consumer friendly, easier to use, and more reliable; mix in world-class industrial design; and print billions. Artificial intelligence is for tech bros and data scientists. Apple Intelligence is AI for the rest of us. Shrewd.

The tech press has spent the past 18 months telling us Apple is behind on AI. While in the next breath reporting on the AI gaffes produced by its rivals. And that’s the point. Apple is always behind. Apple is a distinctly inventive company — its $30 billion R&D budget generates 2,000+ patents per year. But it’s mainly improving vs. inventing: ways to more precisely cut white cardboard boxes to deliver its new devices; new glues to bond layers of glass and plastic together in its phones. For the big stuff, like the mouse, digital music, and multitouch screens, it lets someone else traverse the Sierra Nevadas first.

In addition, I plan to live my life over again, courtesy of Apple Memories. And that’s the real promise of technology: not to explore new worlds in a dildo or reduce customer service costs; but to save people time so they can spend more moments with loved ones … and feel closer to them. Tech’s promise isn’t artificial intelligence but native intimacy.

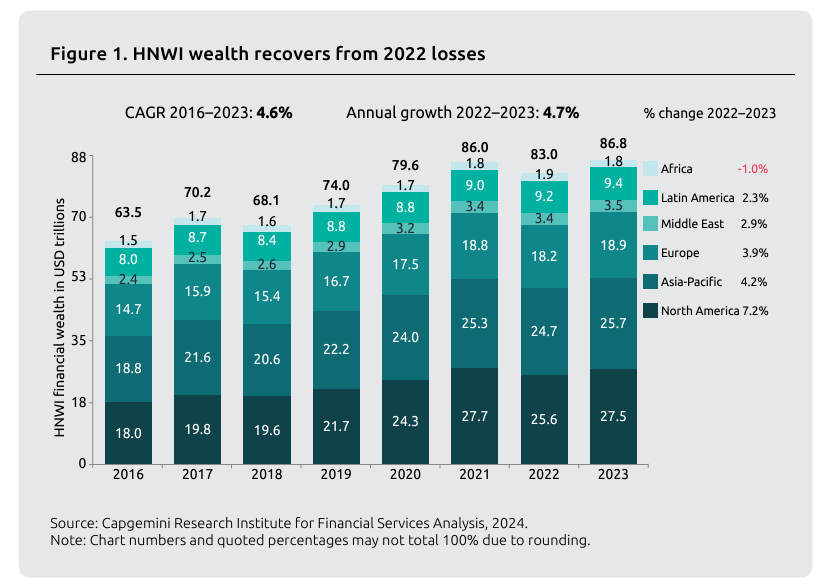

One Chart You Should Not Miss: Ultra-Wealthy (Capgemini Wealth Report 2024)

Overall, the wealth of High Networth Individuals (HNWI) rebounded 4.7% in 2023, back on trend, with North American growth leading the charge.

HNWIs have been reducing cash (from 34% of total assets in Jan 2023 to 25% in Jan 2024) reallocating to growth assets (real estate, alternative assets) and fixed income although they reduced overall equities allocation.

The ultra-high-networth (with $30 million+) holds 34% of total HNWI’s wealth but is just over 1% of the HNWI population, indicating this is the most lucrative segment for wealth management firms.

One Term to Know: Market Timing

Timing the market is a strategy that involves buying and selling stocks or shifting from one asset class to another based on expected price changes (Investopedia).

This investment strategy is often thought of as the opposite of the buy-and-hold strategy where positions are held for the long term without churning. The saying goes: timing in the market is better than timing the market.

While active traders and managers may profit from market timing strategy, as they could potentially avoid riding down the downdraft and shifting their positions to something calmer, this is generally not advisable or achievable for individual investors.

There are three main problems:

Investors need to constantly monitor the market for price patterns, which is draining and time-consuming.

Trading in and out of the market increases transaction costs as well as tax bills as all of the trades will be counted as short-term gains/losses.

Investors need to be correct 74% of the time to beat the benchmark portfolio of similar risk annually to equate the performance of a passive index fund (William Sharpe, 1975, Likely Gains in Market Timing).

A more recent study by Vanguard Investment Advisory Research Centre for the period June 1996 to March 2024 found more compelling evidence that market timing does not work:

A portfolio of $100,000 holding 60% US stocks (broad market) and 40% US bonds (aggregate bonds - government and credit) if left alone would have grown to $865,000.

Missing the 5 best days, your total return would have been $659,000; missing the 10 best days, $540,000, and missing the 25 best days, $343,000 (about 40% of $865,000).

The takeaway is: the objective of investing is to meet your goals; by playing with market volatility, you will likely incur additional risk and not be able to realize the expected returns from the market to meet your goals. The better way to invest and meet your objective is to stay the course but rebalance your portfolio according to your target allocations periodically.

[🌻] Things I Learn About AI:

+ How Do Companies Start Using Gen AI? McKinsey in this brief explained companies gearing up for Gen AI need to determine the right type of strategy for adopting the technology - are you a taker, shaper, or maker?

+ Have you used Bing Chat now called Copilot (Your Everyday AI Companion) recently on Microsoft Edge? If you haven’t, please do. I find they can not only crawl the web in real-time but also quote the most relevant sources compared to other LLMs.

Sign into Microsoft Edge and use the Copilot/Chat on the right-hand sidebar, and select the Precise mode. You can also use other browsers, but I recommend signing in to your Microsoft account for longer conversations.

You can ask questions, summarize content, generate poems/stories/content/code, translate language, generate images from text (like the one below), etc.

👍The best thing: you can select your source whether from the web, your particular tab, etc. They will provide resource links or highlight answers sourced from your tab/document.

It is now powered by GPT-4o, OpenAI's latest LLM model.

Here’s a good reference to Copilot and the art of the prompt.

{Prompt: A serene waterfall in Spring with birds flying on top of the water and blooming flowers near the waterfall.]

Please do not hesitate to get in touch if you have any questions!

Please also check out my Conversations with female fund managers, wealth advisors, and more!

Also, if you miss my latest post about investing, please read it here:

If you like this Weekly, please share it with your friends or subscribe to my newsletter🤝.

Great piece! I loved that chart at the end too comparing the differences in compounded returns if you take out the 5 best/worst days of the year.

Great read! Very informative!